The concepts under analysis were developed through intense dialogue with business managers. While maintaining academic rigour, Integrated Performance Management presents ideas that students will find relevant outside of the classroom. Postgraduate and MBA students in a range of areas including strategy, accounting, finance, operations management, marketing, leadership and human resource management will find this book useful.

eBook - ePub

Integrated Performance Management

A Guide to Strategy Implementation

- 352 pages

- English

- ePUB (mobile friendly)

- Available on iOS & Android

eBook - ePub

Integrated Performance Management

A Guide to Strategy Implementation

About this book

Linking various disciplines and management functions, Integrated Performance Management provides the reader with a concrete framework to manage organizations successfully. The authors do not isolate a single strategy to manage performance. Instead, the book focuses on a range of strategies providing the reader with an introduction to each one.

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Study more efficiently using our study tools.

Information

Publisher

SAGE Publications LtdYear

2004Print ISBN

9781412901550

9781412901543

Edition

1eBook ISBN

9781446240014

1 | Integrated Performance Management: New Hype or New Paradigm? |

A new world with new challenges …

The business world is changing at an ever-increasing pace. The globalization of markets, the revolution in information and communication technologies, the increasing importance (and volatility) of financial markets, and the war for talent are only a few of the change drivers in our current business climate. In this ever-changing world, today’s managers are confronted with a number of daunting challenges in their quest for creating value. Business is becoming more and more complex. Newly trained and empowered employees have implemented many innovative practices, including continuous improvement, empowerment, Activity-Based Costing, re-engineering and quality management. Companies are looking for new forms of relationships with customers, suppliers, employees and other stakeholders. Intangible assets have become the major source of competitive advantage. As a reaction, companies have been changing their operating assumptions to include the development of closer value chain relationships, customization of products and services, reliance on knowledge workers, and an intense focus on innovation. At the same time, companies have been downsizing, de-layering and outsourcing strategically non-relevant activities. And all these new trends are occurring against a background of intensified competition.

Managers are thus confronted with greater uncertainty and unpredictability, leading to greater risk in decision-making. In such a rapidly changing and complex environment, past performance becomes less valuable for guiding future strategic options. Furthermore, the consequences of making ‘wrong’ decisions can be disastrous. Effective risk management is becoming increasingly key to successful business. In the current Information Age, the rising activism of all kinds of stakeholder puts further pressure on managers, and new codes for corporate governance create additional responsibilities for the directors and managers. The management of any organization (whether private or public, for-profit or non-profit) is held accountable for more than just financial bottom-line results.

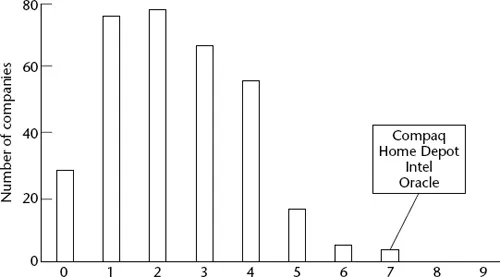

All these changes in the business context impose new challenges on the management of today’s organizations. Academic and consulting professionals are responding with an ever-expanding range of new tools, usually encapsulated in nice three-letter acronyms (BPR, TQM, EVA®, and many others). In many cases, the results have been disappointing – particularly when the initiatives have been attempted without linking them to corporate strategy (Stivers and Joyce, 2000). Research at the Strategos Institute, Gary Hamel’s international consulting company, has shown that only a small number of companies were able to provide sustained high returns to their shareholders in the last decade (Figure 1.1).

The research indicates that not even 20 US companies were able to provide high shareholder returns for five consecutive years. Only four companies were able to show these returns for seven consecutive years.1 Why do so many organizations have difficulty delivering sustained performance?

Figure 1.1 The challenge of sustaining high shareholder returns (1990–99)

Source: Strategos Institute (2001)

What is lacking?

There are, of course, many reasons why organizations are not able to meet their performance expectations. One of the most obvious reasons is the inability of companies to efficiently and effectively define and create customer (and hence, shareholder) value. The idea that companies succeed by selling value is not new. But companies find it extremely difficult to define a unique strategic position in an ever-changing competitive arena.

However, having a clear vision and a well-defined strategy are not enough. Business observers are more and more convinced that the ability to execute strategy is more important than the quality of the strategy itself. In their most recent book, The Strategy-Focused Organization: How Balanced Scorecard Companies Thrive in the New Business Environment, Robert Kaplan and David Norton (2001) see the ability to execute the strategy as an even bigger management challenge than determining the right vision and strategy in the first place. Kaplan and Norton point to the importance of adequate performance management systems as a critical success factor for implementing strategy: ‘Strategies are changing, but the tools for measuring strategies have not kept pace’ (2001: 2).

Consultants and academicians are aware of this and have started a quest for the appropriate performance measures. For a long time, companies have used financial accounting-based performance measures to track how well the organization is doing. Financial control systems emerged when international conglomerates were created at the end of the previous century. The managers of these conglomerates focused on controlling costs and installing efficient production processes. These financial control systems were adequate for such industrial economies. The picture changed when new elements, such as quality and service, started to determine the competitive advantage of firms and when the Total Quality movement conquered the world. However, the management control systems did not change and financial control systems stayed in place (although some of them captured some aspects of quality as well).

Criticism of conventional performance measurement systems grew in the mid-1980s. Critics charged that financial performance measures lack the requisite variety to give decision-makers the range of information they need to manage processes. Performance measurement systems based primarily on financial performance measures lack the focus and robustness needed for internal management and control (Atkinson et al., 1997). Andy Neely and Rob Austin (2002) have called this first measurement crisis measurement myopia, which essentially stems from the fact that the wrong things were being measured.

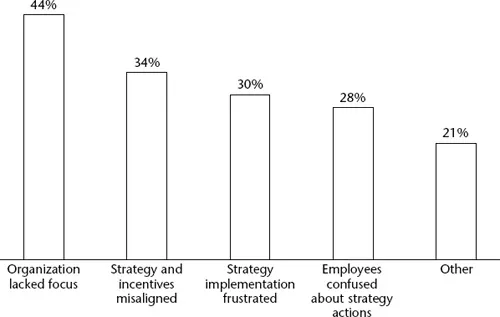

Hence, the call for more strategic types of management control. One of the first definitions of strategic control goes as follows: ‘Strategic control focuses on the dual questions of whether: (1) the strategy is being implemented as planned; and (2) the results produced by the strategy are those intended’ (Schendel and Hofer, 1979). According to this definition of strategic control (and other, similar definitions), there should be a clear link between an organization’s strategy and its performance measures. Good performance measures should predict the long-term financial success of the business. More and more companies are acknowledging that performance measurement systems need focus by linking them to the strategy of the organization. Often, managers are confused by changing priorities. This year, a company may focus on Business Process Re-engineering (BPR), next year on capabilities enhancement, and the year after that on Total Quality Management (TQM). Without a clear strategy, managers will remain confused and sceptical about new strategic initiatives. An international survey by The Conference Board of 113 chief financial officers (CFOs) and corporate strategists revealed that the lack of organizational focus is the major reason for having a formal strategic performance measurement system. Furthermore, the respondents believe that strategic performance measurement systems could be very helpful for implementing strategy more effectively (Gates, 1999), as is shown in Figure 1.2.

Many academicians and performance management consultants see a solution in new performance measurement systems, as demonstrated in the following statement:

The global market and its rapid pace of change have increased the demand on measurement systems in modern corporations. The ‘command and control’ function (previously served by performance measurement systems) has been transformed into a need to ‘predict and prepare’ the organization to meet the next challenge and to create the next opportunity. Changes to the business context are also changing the nature of measurement. Process management emphasizing value and service to the customer is replacing traditional vertical and functional structures. Decision-making is increasingly being moved lower in the organization; self-directed teams rather than individual managers now make decisions. Virtual corporate structures are creating the need to manage and measure performance across the value chain. Each of these shifts has implications for the performance management system and its ability to effectively serve the organization and its stakeholders. (Institute of Management Accountants and Arthur Andersen LLP, 1998: 1–2)

Figure 1.2 Reasons cited for introducing strategic performance measurement systems

Source: Gates (1999)

However, according to Andy Neely and Rob Austin, this quest for more appropriate performance measures (and measurement systems) has resulted in a real ‘measurement madness’:

[S]ociety is obsessed with measurement. The desire to measure and quantify has become overwhelming. … Organizations are seeking to value their intellectual assets, their brands, their innovative potential, in addition to their operating efficiency, their economic profit, and the satisfaction of their employees, customers, and shareholders. Today the old adage, ‘if you can’t measure it, you can’t manage it,’ has been taken to a new extreme and in many organizations the result is confusion. (Neely and Austin, 2002: 42–3).

Therefore, rather than developing new performance measures or measurement systems, we need a more integrated approach towards performance management. In this book, we will present such an integrated approach. But before we outline the building blocks of our new framework, we will first explain how we define the concept of Integrated Performance Management.

Integrated Performance Management: what’s in a name?

Integrated Performance Management or IPM (a new three-letter acronym indeed) is not a new term. It is being used with increasing frequency in the performance management literature but, as is the case with many widespread management concepts, there is confusion about what it exactly stands for. This can partly be ascribed to the fact that performance management processes manifest themselves in many different ways and that contributions to performance management come from many different angles: strategy, finance, management accounting and control, operations management, and human resource management (HRM).

Still, the concept has great potential for helping to solve some of the issues we have been discussing. But then we need to define what we mean by ‘performance’ and ‘performance management’, and we should explain what makes performance management really ‘integrated’.

A definition of performance

‘Performance’ is a term used in a variety of disciplines. For example, athletes out-perform the field when they jump the highest or run the fastest. In other sports disciplines – in team sports or gymnastics, for example – performance evaluation becomes somewhat more complicated. In these sports disciplines, athletes or teams are usually evaluated along composite ‘performance’ measures, such as technical difficulty, originality or a creativity criterion. The personal experience and intuition of the jury plays an important role in their rating. In the field of biology, Darwin introduced his ideas of variation, specialization and collaboration as tactics for survival in a complex and uncertain environment. Those species that manage to adapt to their environment ultimately survive. The ability to adapt, and the speed and method of adaptation, can be seen as forms of out-performance.

In this book, we focus on organizational performance. Organizational performance is at the heart of strategic management and accounting disciplines (Venkatraman and Ramanujam, 1986). Although widely used in theoretical and empirical research, the notion of organizational performance remains largely unexplained and recourse is taken to commonly used operationalizations of performance. There is relatively little agreement about which definitions are ‘best’ and which criteria should be used to judge the definitions (Barney, 1997). Moreover, many definitions capture the notion of performance only partially. The reason why organizational performance is so difficult to define is to be found in the multidimensionality of the performance concept. For example, performance can be defined in financial terms (e.g., market value, profitability, value-at-risk), but it is often used in other environments, such as operations (e.g., efficiency, effectiveness, number of outputs, throughput-time, product or service quality), marketing (e.g., customer satisfaction, number of customers retained over a certain period), and others.

A conceptual definition of organizational performance was forwarded by Jay Barney, a strategy professor at Ohio State University. The starting point for Barney’s (1997) conceptualization is that an organization is an association of productive assets which come together to obtain economic advantages. For an organization to continue to exist, the owners of these productive assets must be satisfied with their use. The owners will only be inclined to provide these assets if they are satisfied with the returns they are receiving. So, organizational performance is defined in terms of the value that an organization creates using its productive assets in comparison with the value that the owners of these assets expect to obtain. If the value that is created is at least as large as the expected value, then it is likely that the owners of these assets will make them available to the organization. On the other hand, if the value created is less than expected, the owners might look for other alternatives and withdraw their support.

A definition of performance management

Apart from the multidimensional nature of the performance concept, the performance management literature also suffers from concentrating too much on finding the appropriate performance measures. That is, there is too much focus on performance measurement. In general, performance measurement can be viewed as the process of quantifying the efficiency and effectiveness of purposeful action and decision-making (Waggoner et al., 1999). Performance measurement should provide the data that will be collected, analysed, reported and, ultim...

Table of contents

- Cover Page

- Title

- Copyright

- Contents

- Preface

- Editors’ Preface

- Acknowledgements

- Contributors

- 1 Integrated Performance Management: New Hype or New Paradigm?

- PART I – AN OVERVIEW OF TRADITIONAL PERFORMANCE MANAGEMENT FRAMEWORKS

- PART II – THE INTEGRATED PERFORMANCE MANAGEMENT FRAMEWORK: CONSTITUENT ELEMENTS

- PART III – ADDING A NEW DIMENSION TO INTEGRATED PERFORMANCE MANAGEMENT: INTRODUCING THE CONCEPT OF MATURITY ALIGNMENT

- References

- Index

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

- Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

- Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go.

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Integrated Performance Management by Kurt Verweire, Lutgart van den Berghe, Kurt Verweire,Lutgart van den Berghe in PDF and/or ePUB format, as well as other popular books in Business & Management. We have over 1.5 million books available in our catalogue for you to explore.