- 62 pages

- English

- ePUB (mobile friendly)

- Available on iOS & Android

eBook - ePub

Corporate Valuation Using the Free Cash Flow Method Applied to Coca-Cola

About this book

The value of a corporation is the discounted present value of future cash flows provided by the company to the shareholders. The valuation process requires that the corporate financial decision maker determine the future free cash flow to equity, the short-term growth rate, the long-term growth rate, and the required rate of return based on market beta. This book provides a template for demonstrating corporate valuation using a real company—Coca-Cola. The data used in this book comes from the financial statements of Coca-Cola available on EDGAR. Other data are from SBBI, Yahoo! Finance, the U.S. Bureau of Economic Analysis, Stocks, Bonds, Bills, and Infla-tion, Market Results for 1926–2010, 2011 Yearbook, Classic Edition, Morningstar, and US Department of the Treasury.

Information

Topic

Negocios y empresaSubtopic

FinanzasCHAPTER 1

Introduction: An Overview of Corporate Financial Management

Corporate financial management can be defined as the efficient acquisition and allocation of funds. The efficient acquisition of funds requires the firm to acquire funds at the lowest possible cost, and the efficient allocation of funds requires investing funds at the highest possible expected rate of return. If the firm acquires funds at the lowest possible cost and invests funds at the highest possible return, net cash flow to the firm will be maximized. The objective of corporate financial management is to maximize the value of the firm. The value of the firm is the market capitalization of the firm, which is the number of common equity shares times the price per share. The value of the firm is determined by the risk and return characteristics of the firm. The relationship between risk and return is positive and linear. Firms that want to earn higher rates of return must be willing to assume greater levels of risk, and firms that want to have lower levels of risk must be willing to accept a lower rate of return. The risk and return characteristics of the firm are determined by the decisions made by the managers.

Corporate financial management decisions fall into three categories. Managers make decisions about

1. investing;

2. financing;

3. paying dividends.

Investing decisions determine the specific assets purchased by the firm, and the assets purchased by the firm determine the asset structure of the firm or the left-hand side of the balance sheet, assets. The financing decisions determine the extent to which the firm uses fixed cost financing. Fixed cost financing is the use of bonds that have a cost to the firm that does not change over the life of the bond, that is, the interest payment is fixed for the life of the bond. The financing decisions determine the right-hand side of the balance, liabilities and owners’ equity. The dividend decision is separate because, on the one hand, the dividend decision is an allocation of funds but is not an investment decision because no assets are purchased. On the other hand, the dividend decision affects the right-hand side of the balance sheet, specifically, retained earnings, but is not a financing decision. In addition, the dividend decision affects firm valuation through a number of mechanisms.

Once the firm’s financial managers have made a set of decisions, we have a firm that can be represented by the financial statements—the balance sheet and the income statement. The financial statement information can be used to estimate the level and the riskiness of expected future cash flows for the firm. The cash flows are represented by a probability distribution of all possible cash flows and the probability of each of the possible cash flows. The degree of operating leverage is determined by the amount of fixed cost assets used by the firm, and the degree of financial leverage is determined by the amount of fixed cost financing used by the firm. The combine leverage effect is represented in the required rate of return for the firm.

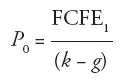

The value of the firm is the discounted present value of all of the future cash flows discounted at the required rate of return. Cash flow today is worth more than cash flow in the future because the firm can invest cash flow and earn a rate of return on cash currently in one’s possession, which means that next year’s cash level will be higher than today’s cash level. Alternatively, cash in the future is worth less than cash today. The more risky the cash flow is further into the future, the less the cash flow is worth today. Each cash flow in the future, free cash flow to equity (FCFE)t, which will grow from FCFE0, which is the current dividend, at an estimated rate, g, must be discounted by the required rate of return, (1 + k), to reflect the amount of risk and the time in the future. The sum of the growing and discounted future cash flows from time zero to time infinity is as follows:

(1.1) P0 = ΣFCFE0 (1 + g)t/(1 + k)t

We can simplify this expression after making a number of simplifying assumptions to the following expression:

(1.2)

That is, the value of a share of stock is equal to the expected dividend at time t = 1 divided by the required rate of return minus the expected future growth rate.

The information and process to value a company require finding financial data, stock price and dividend data, and bond data. FCFE is derived from the balance sheet, the income statement, and the statement of cash flows. Short-term growth is estimated using sustainable growth, and long-term growth is estimated using gross domestic product (GDP) growth. The required rate of return is calculated using the security market line with market beta, Treasury bond rates, and the long-term rate of return on the stock market.

Table 1.1 shows the relationship among value, expected cash flow, and the discount rate for a firm that does not grow. As the expected net cash flows increase, for a given discount rate, the value of the firm increases. Alternatively, as the required rate of return decreases for a given expected net cash flow, the value of the firm increases.

Table 1.1 The relationship among value, expected net cash flow, required rate of return, and required rate of expected net cash flow return

| (percent) | 100 | 200 | 300 |

| 20 | 500 | 1,000 | 1,500 |

| 10 | 1,000 | 2,000 | 3,000 |

| 5 | 2,000 | 4,000 | 6,000 |

Table of contents

- Cover

- Half Title

- Title Page

- Copyright Page

- Abstract

- Contents

- Preface

- Acknowledgments

- Chapter 1: Introduction: An Overview of Corporate Financial Management

- Chapter 2: Determining the Short-Term Growth Rate Using the Extended DuPont System of Financial Analysis

- Chapter 3: Determining the Long-Term Growth Rate

- Chapter 4: Calculating the Beta Coefficient and Required Rate of Return for Coca-Cola

- Chapter 5: Free Cash Flow to Equity

- Chapter 6: Valuing Coca-Cola

- Appendix

- References

- Index

- Ad Page

- Back cover

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Study more efficiently using our study tools.

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go.

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Corporate Valuation Using the Free Cash Flow Method Applied to Coca-Cola by Carl McGowan in PDF and/or ePUB format, as well as other popular books in Negocios y empresa & Finanzas. We have over 1.5 million books available in our catalogue for you to explore.