George Selgin is one of the world's foremost monetary historians. In this book, based on the 2016 Hayek Memorial Lecture, he shows how a system of private banks without a central bank can bring about financial stability through self-regulation. If one bank stretches credit too far, it will be reined in by the others before the system as a whole gets out of control. The banks have a strong incentive to ensure an orderly resolution if a particular bank is facing insolvency or illiquidity.Selgin draws on evidence from the era of 'free banking' in Scotland and Canada. These arrangements enjoyed greater financial stability, with fewer banking crises, than the English system with its central bank and the US model with its faulty government regulation. The creation of the Federal Reserve appears to have increased the frequency of financial crises.The book also includes commentaries by Kevin Dowd and Mathieu Bédard. Dowd asks whether free-banking systems should be underpinned by a gold standard, which he regards as a tried-and-tested institution at the heart of their success. Bédard challenges the assumption that the banking sector is inherently unstable and therefore requires state intervention. He argues that increases in government control have made the banking system more prone to crisis.

- 88 pages

- English

- ePUB (mobile friendly)

- Available on iOS & Android

eBook - ePub

Financial Stability Without Central Banks

About this book

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Study more efficiently using our study tools.

Information

Edition

1When I was a young boy, my twin brother and I would play a game with my father called ‘the five-line game’. I don’t know if this was a game anyone else played, but we did. This game worked as follows. We would scribble five lines on a piece of paper, any kinds of lines or curves and what have you, and we would tell my father that he had to make from these lines, incorporating all of them, a picture of something like an elephant or a dog. The idea was that the picture had to look like the thing we wanted it to look like. All the lines had to be used, and they could not look odd. My father was excellent at this game.

What has that got to do with this talk? Well, the five-line game came to mind when I finally got around to taking a good look at the title that had been assigned to my talk, and I found myself thinking, ‘How the heck am I going to turn those words into a good lecture?’ I struggled with it. Finally I thought, ‘I can talk about this; I think I can make it work. But I’ll have to cheat a little bit’.

So, I am going to tell you about financial stability without central banks, sure enough; but I am going to cheat by telling you, not about ‘price stability … without central banks’, but about financial stability without price stability! I can’t help cheating this way because I do not believe that price stability, as it is normally understood – as a stable price level or absolutely stable rate of inflation – is in fact a desirable thing.

I am going to explain to you how we can have stability – financial stability or macroeconomic stability, if you like – without central banks and also without a stable price level, though still with a price level that behaves in a certain systematic fashion.

Financial stability without central banks

As for financial stability without a central bank, well, it is actually rather easy to explain that this is possible because history shows that it is possible. Geographically closest to where we are today, history has given us a good example in the Scottish banking system, which flourished from roughly the latter part of the eighteenth century until the middle of the nineteenth century, when the UK government started to interfere and ruin it, eventually turning it into the disaster that it has become in recent times.

The Scottish system, unlike the English system, did not rely upon a privileged bank of issue, or what would later come to be known as a central bank. This was due to a sort of benign neglect on the part of Parliament. The Bank of Scotland had received the first charter for a banking and currency business in Scotland. But because it was suspected of being a Jacobite institution, Parliament allowed a rival bank, the Royal Bank of Scotland, to be established. That step opened the floodgates to what ultimately became a system of numerous banks, all of which could issue bank notes.

It was because there were many banks of issue, almost entirely free from any sort of government regulation, that Scotland ended up with a notoriously stable financial system. The stability was ultimately due to the pressure that the competing banks of issue exerted upon one another by actively presenting notes of rival banks that they received in the course of a business day to those banks for collection, either directly or indirectly through a clearing house, where clerks would figure out how much each bank owed to other banks.

This mechanism created a discipline that was not unlike the discipline one finds in a chain gang. In a chain gang, the prisoners are chained to one another, but none has to be chained to anything else. That’s because none of them can run away without being tripped up by the others, and because it’s practically impossible for them to coordinate their steps so as to all run away at once, as any of you who has ever been in a three-legged race can imagine.

What’s the analogy? It’s that, were any one Scottish bank too aggressive in its lending, it would essentially be trying to run ahead of the other banks. But unless all the banks were somehow acting in unison, the aggressive bank would find more of its notes presented to it at settlement time, without itself receiving a like value of other banks’ notes, and it would have to have, or get hold of, reserves to cover its net dues to the rest of the system, or else it would default. In short, no Scottish bank could afford to be too generous in its lending if it wished to avoid being ‘tripped up’ by losing reserves to other banks in the system.

In fact, early in the history of the Scottish system, there was a very good example of how this discipline worked. The example consisted of the notorious failure, which at least some of you have perhaps heard of, of the so-called Ayr Bank, the formal name of which was Douglas, Heron & Company.

Set up around 1770, the Ayr bank and its various branch offices immediately proceeded to lend money on extremely generous terms to various borrowers, with the express aim of becoming the biggest Scottish bank of issue – and doing so very quickly! In making loans, the Ayr exchanged its own paper notes for borrowers’ IOUs. Had the Ayr’s borrowers just held on to the notes, things might have gone splendidly. But borrowers like to spend the money they borrow. So the notes soon found their way into the hands of Scotland’s other banks; and those banks wasted no time returning them to the Ayr Bank for payment.

As theory would predict, the Ayr Bank was soon being bled by its less aggressive rivals. Eventually, if it didn’t change course, they would bleed it dry. But the Ayr tried to put off the inevitable, not by contracting its lending, or by rethinking its overall strategy for success, but by borrowing in London to cover its cash losses. Of course, the Ayr couldn’t have kept that up for very long under the best of circumstances. In the event, when its London creditor itself failed, the gig was up. Soon afterwards the Ayr folded, bringing some smaller Scottish banks down with it. The rest, having anticipated the debacle, kept safely out of harm’s way.

The eventual result of the Ayr’s failure – a failure of what had, in fact, become Scotland’s biggest bank, as measured by its total assets at the time of its failure – was that Scotland enjoyed almost a century of complete economic and financial stability. There was, thank goodness, no such thing as ‘Too Big To Fail’ at the time; and Scotland in any case had no central bank capable of carrying out such a policy. Instead, because of the lesson taught by the Ayr Bank’s failure, Scotland entered into a long period of remarkable monetary stability, during which no other bank again dared to behave as the Ayr Bank had.

Now, there is also a more subtle advantage of the ‘chain-gang discipline’ of a competitive banking system, which has to do with how it stabilises the total amount of spending in the system. As I explained before, if they are to survive, competing banks of issue cannot individually be too generous in their lending; but they cannot collectively be too generous either, because that would require that they manage somehow to perfectly coordinate their expansionary policies, so that none finds itself losing reserves, which is practically impossible. At some point, and probably very quickly, one of the banks will feel the pinch of a net reserve loss, and that will make it hesitate, forcing the other banks to abandon the scheme as well.

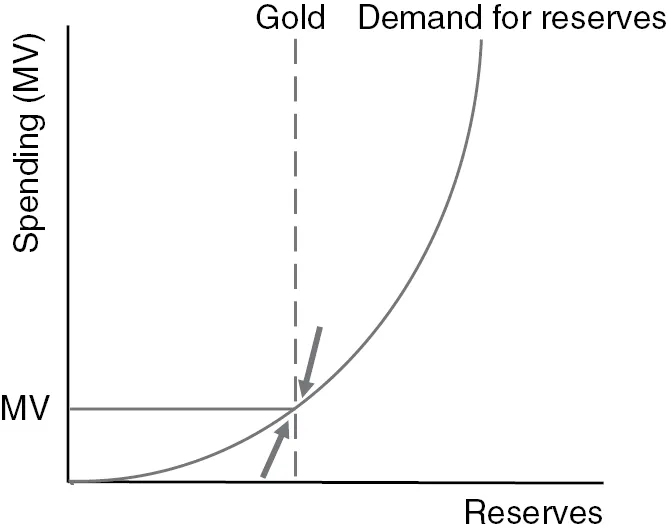

The overall discipline that this chain-gang behaviour imparts on the system is summed up in Figure 1.

- Spending equilibrium: free banking

The vertical line in the figure represents the supply of reserves in the Scottish banking system, where reserves consist mainly of gold and silver coin held by the Scottish banks. Those coins must be acquired through the course of trade with other nations. The vertical schedule reflects the fact that their quantity doesn’t change with the level of spending within Scotland itself, which is what the figure’s vertical axis measures.The banks’ overall demand for reserves is, on the other hand, a function of the value of notes (and perhaps some cheques) being exchanged for goods or services every day, which is to say, on the total amount of spending going on in the Scottish economy. If no one spends anything, the banks don’t need any reserves for settlement, because there’s nothing to settle! So, the demand schedule starts at the figure’s lower left-hand corner.As spending increases (where the level of spending is equal to the product of the quantity of money in the Scottish economy and its velocity, and velocity is just how many times each unit of money gets spent in a period of time), the demand for reserves also increases, though generally less than proportionally. Consequently, the demand schedule curves up from the origin. It follows that there’s a particular point where the quantity of reserves available is equal to the quantity demanded, and that the system will be in equilibrium at that level of spending.Now, this equilibrium does not mean that the banks cannot and are not inclined to adjust how big they are and how many IOUs (notes and deposits) they have outstanding. The velocity of money measures how anxious people are to spend money; that is, velocity moves inversely with people’s willingness to refrain from spending money, or what economists call their demand for money balances. If velocity declines, people are trying to hold more notes and deposits, and are therefore spending less. In that case the banks – that is, those banks whose notes or deposits are in greater demand – can issue more banknotes and create more deposit credits because the requirement for supply and demand equilibrium allows them to do so. If a particular bank’s notes, for example, are being spent less actively, that bank can issue more notes without needing more reserves to cover the presentation of those notes for gold. And, of course, this works in reverse. If the people are spending more aggressively, the banks will find that they had better reduce their outstanding IOUs by lending less.So, in a free banking system like Scotland’s, you h...

The vertical line in the figure represents the supply of reserves in the Scottish banking system, where reserves consist mainly of gold and silver coin held by the Scottish banks. Those coins must be acquired through the course of trade with other nations. The vertical schedule reflects the fact that their quantity doesn’t change with the level of spending within Scotland itself, which is what the figure’s vertical axis measures.The banks’ overall demand for reserves is, on the other hand, a function of the value of notes (and perhaps some cheques) being exchanged for goods or services every day, which is to say, on the total amount of spending going on in the Scottish economy. If no one spends anything, the banks don’t need any reserves for settlement, because there’s nothing to settle! So, the demand schedule starts at the figure’s lower left-hand corner.As spending increases (where the level of spending is equal to the product of the quantity of money in the Scottish economy and its velocity, and velocity is just how many times each unit of money gets spent in a period of time), the demand for reserves also increases, though generally less than proportionally. Consequently, the demand schedule curves up from the origin. It follows that there’s a particular point where the quantity of reserves available is equal to the quantity demanded, and that the system will be in equilibrium at that level of spending.Now, this equilibrium does not mean that the banks cannot and are not inclined to adjust how big they are and how many IOUs (notes and deposits) they have outstanding. The velocity of money measures how anxious people are to spend money; that is, velocity moves inversely with people’s willingness to refrain from spending money, or what economists call their demand for money balances. If velocity declines, people are trying to hold more notes and deposits, and are therefore spending less. In that case the banks – that is, those banks whose notes or deposits are in greater demand – can issue more banknotes and create more deposit credits because the requirement for supply and demand equilibrium allows them to do so. If a particular bank’s notes, for example, are being spent less actively, that bank can issue more notes without needing more reserves to cover the presentation of those notes for gold. And, of course, this works in reverse. If the people are spending more aggressively, the banks will find that they had better reduce their outstanding IOUs by lending less.So, in a free banking system like Scotland’s, you h...

Table of contents

- The authors

- Foreword

- Acknowledgement

- Summary

- 1 Price stability and financial stability without central banks: lessons from the past for the future

- 2 Questions and discussion

- 3 Selginian free banking

- 4 On chain gangs in financial stability

- About the IEA