- 296 pages

- English

- ePUB (mobile friendly)

- Available on iOS & Android

eBook - ePub

Housing and Finance in Developing Countries

About this book

This book explores the linkages between formal and informal housing finance drawing upon the lessons of NGO and micro-finance practices. Both public and private formal finance institutions have experienced great difficulty in lending below a middle-income client group, and are often reluctant to lend for the purpose of housing at all. This failure of formal finance to filter down to low-income households, and in particular to women, has led various NGOs and community groups to create and adopt innovative finance programmes, such as informal savings banks and credit rotating schemes. The authors critically assess the impact of theses schemes, and evaluate links between gender, housing and finance.

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Study more efficiently using our study tools.

Information

Part I

Position Papers

1

From Self-Help to Self-Finance

The Changing Focus of Urban Research and Policy

University of Wales, Swansea

Introduction

A strong relationship between levels of urbanization and wealth has been demonstrated both theoretically and empirically in numerous studies (Malpezzi 1990, World Bank 1993b). Yet, in practice, it has proven to be very difficult to harness the enormous wealth generated through urbanization for the benefit of low-income households. Traditionally, faced with other development priorities, governments and international agencies have been reluctant to encourage investment in housing, which has often been seen as an item of consumption (UNCHS 1991b, 1996). Moreover, many of the first wave of housing finance institutions were poorly managed and contributed to macroeconomic disruption (Buckley 1996, Buckley and Mayo 1989). Even by the late 1980s, Renaud was able to observe that ‘few aspects of economic development remain as unexplored and poorly analysed as the potential to induce financial development and ways to improve the financing of housing’ (1987b:30).

These practical and conceptual difficulties notwithstanding, during the 1990s housing finance moved to the top of the urban agenda (World Bank 1993a). Under pressure to reform urban management, governments have made important legislative and institutional reforms to enable private institutions and non-governmental organizations (NGOs) to have a greater role in the provision of housing finance.1 The lead of the World Bank has been especially important in making the shift from housing projects towards the delivery of housing finance (World Bank 1993a). From 1983 to 1988, Bank lending for housing finance exceeded the total for sites-and-services from 1972 to 1988 and by 1989 almost one-half of all Bank urban lending was for housing finance programmes (Buckley this volume). This reorientation went beyond the need to deliver more and better housing, to make urban policy compatible with macro-economic management, particularly in the context of structural adjustment programmes in which control of foreign exchange risks and fiscal probity have been paramount (Buckley 1996, Jones and Ward 1994, Malpezzi 1994).

While this policy shift has generated a significant literature on the supply-side of housing finance, our understanding of the uses to which households have put finance and the implications for house construction is less advanced and requires attention to a more disparate literature. The aim of this chapter is to draw together the emergence of leading-edge themes of housing finance in developing countries and to place these within the broad context of the housing problem and the evolution of housing finance policy and research. To some extent, our aim is also to play devil’s advocate to some of our own contributors and the literature in general. Following the policy debates on housing finance prior to Habitat II in Istanbul (1996) and on micro-finance in the lead up to the Microcredit Summit in Washington (1997) we noted the high degree of optimism and the tendency to cite ‘positive’ experiences. General claims have been made for the ability of private-sector institutions to go down-market and lend to lower middle-income and, with less regularity, low-income households. Partly building upon the experience of programmes for micro-enterprise and consumption finance, arguments have been made for the ability of NGOs to deliver housing finance. The extension of micro-and housing finance was also being linked to the empowerment of low-income households and communities, and especially of women. While not wishing to dispute the validity of specific cases, our argument is for caution and to concur with the stoic advice of Adams and von Pischke that ‘debt is not an effective tool for helping most poor people enhance their economic condition’ (1992: 1468). We believe that the potential of housing finance as a means to improve living conditions can be better understood if governments, NGOs and international agencies analyse the weaknesses as well as the successes of recent experience.

Housing and Finance

The Scale of the Problem

In developed countries, housing conventionally costs three to four times the combined annual incomes of the owners so that virtually all housing is bought or built with finance. With a typical deposit of between 5 and 20 per cent of the total price, finance is needed to cover about 80 per cent of costs and is usually repayable over twenty years. For most borrowers this debt burden is manageable because, although the finance is repaid at positive interest rates, income growth is likely to be relatively constant and predictable, and the family cycle dictates that most households will have reduced outgoings over time. Although not affecting all households equally, positive interest rates in the short term are partly offset by returns on savings and, in the event that incomes do not increase or that savings are unable to smooth the shortfall, data show that house values tend to outperform inflation. Should normal financing arrangements be insufficient to cover remaining balances of principal, households can realize insurance policies (which can also cover loss of earnings or excessive interest rate increases) or expect an equity windfall from inheritance. In a worse case scenario, lenders are accustomed to offering a range of refinancing packages such as lengthening the loan period or allowing interest rate holidays as a matter of course and often at little additional cost (Diamond and Lea 1992, Hamnett 1994).

By contrast, households in developing countries face a series of problems in attempting to access finance with which to resolve their housing needs Despite enormous absolute housing deficits and the need to improve the existing stock, housing finance often represents less than 10 per cent of all financial transactions. To make matters worse, many housing finance institutions possess losses amounting to many times the value of their capital reserves, have been prone to invest in highly speculative ventures with consequent boom-bust swings in their portfolio and have a track record of delivering funds only when government subsidies are available and only then to the better-off 10–20 per cent of households (Boleat 1987, UNCHS 1991b). Not surprisingly, most estimates of housing investment as a proportion of GDP in developing countries provide figures substantially below those of developed countries (Buckley 1996, Malpezzi 1990, Renaud 1987b, World Bank 1993b).

This situation means that most households have to ‘chase loans’ with upwards of 80 per cent of housing finance transactions taking place in the informal economy (Renaud, 1987b:184, Okpala 1994). The size and the nature of the gap between supply and demand is indicated by Merrett and Russell

The UNDP suggests that in the world of conventional finance, the minimum loan size may be large, whilst the poor require small loans. The formal loan period may be for many years, whilst the low-income household seeks a short maturity, and the availability of follow-on funds. Banks require regular repayments of principal, but workers with insecure earnings need flexible loan schedules. The formal system may offer money only for completed dwellings, when what is needed is money for the initial stages of self-help or improvement of the self-help house once it is constructed. Finance may be offered with conditions written in a language of considerable sophistication, when those in housing poverty require a legal agreement which is easily understood, and under which payments are possible in local premises open throughout the working day for cash payments.

(1994:60)

To this salutary list one might add that formal finance institutions are rarely willing to assist with the purchase of land, especially where the tenure is insecure, to provide assistance with improvements to the rental housing stock or to support non-conventional household arrangements such as sharing or multiple-family compounds. These limitations have implicit gendered consequences as rental and shared housing are of particular importance to low-income women who often lack the means to become home-owners (Chant 1997, Datta 1995, Miraftab 1994). Of course, some of these problems are derived from broader inequalities and do not derive directly from the shortcomings of finance institutions. As a number of authors point out, weaknesses in the delivery of housing, the lack of affordable land and an inefficient urban administration are as much causes of the poor financial condition of the urban sector (Rakodi 1995, Renaud 1987b, Struyk and Turner 1986).

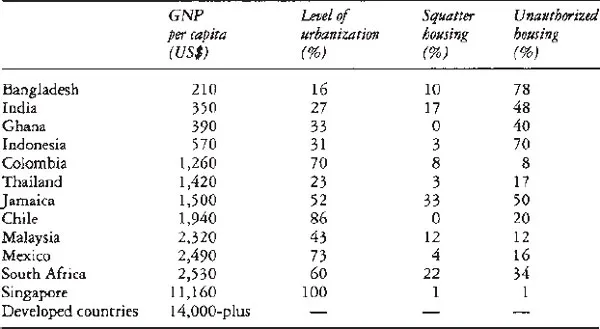

The scale and direction of some of these problems have been captured by the Housing Indicators Program (World Bank 1993b).2 Table 1.1 provides details of the basic housing conditions for countries featured in this volume and for some of those most frequently mentioned in the literature. The details show high levels of urbanization for countries in Latin America and the Caribbean as well as significant levels in South Africa and Malaysia. Squatter housing (illegal land occupation) is clearly a major problem in Jamaica and South Africa, although recent figures for both Colombia (Bogotá) and major Mexican cities provide figures many times higher than those of Table 1.1. Unauthorized housing is a universal problem, accounting for about 30 to 60 per cent of housing. Although differences in the ability of low-income households to acquire finance alone are unlikely to explain cross-country differences in housing conditions, the data indicate that while average income in some countries might be greater the availability and type of finance are of critical importance. For example, in India where few low-income households have access to formal finance the proportion of households living in permanent structures is significantly less than Mexico which devotes more resources to housing and has a range of delivery institutions (for a comparison of Korea and the Philippines see Struyk and Turner 1986).

Table 1.1 Housing conditions in developing countries

Note: The Indicators Program uses key cities (usually capitals) to represent ‘countries’. The cities are Dhaka, New Delhi, Accra, Jakarta, Bogotá, Bangkok, Kingston, Santiago, Kuala Lumpur, Monterrey, Johannesburg and Singapore. Income is converted to Purchasing Power Parity.

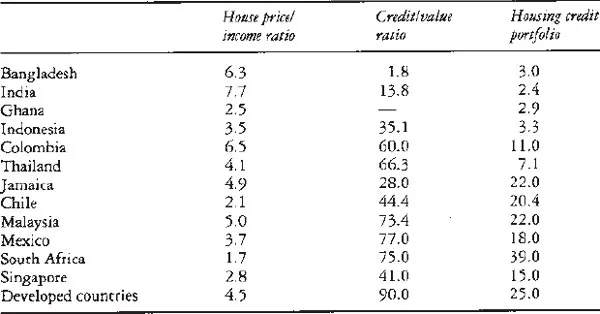

A more detailed look at housing finance conditions is provided by Table 1.2. The house price/income ratio is credited as a proxy for the level of dysfunction in the housing market: a high ratio indicates restrictions to supply and a low ratio indicates insecurity of tenure or poor-quality accommodation.3 The data reveal lower ratios for Africa and Latin America (but not Colombia) than for South Asia, the Middle East and North Africa (World Bank 1993b:11– 12). The ratio also indicates whether better housing finance delivery will improve housing conditions: if the relative cost of housing to income is high, more resources will make little impact upon housing conditions unless institutions are willing to lend many times over conventional income-value ratios. As the column for credit/value ratio indicates, for most countries this is unlikely to be the case.

Table 1.2 Housing finance in developing countries

Table 1.2 also shows that financial institutions seem unable to supply adequate resources for housing purposes. The housing credit portfolio is the ratio of total mortgage loans to all outstanding loans in the commercial and government sectors. It is thus a measure of the relative size of the housing finance sector. A low figure indicates either an underdeveloped sector (perhaps because of opportunities elsewhere) or constraints imposed on the sector by government.4 Although this indicator only includes finance in the formal sector, it demonstrates that housing finance represents only a low proportion of financial transactions in nearly all developing countries and especially those with the lowest levels of GNP.5

Of course, it is extremely difficult to establish housing finance institutions under any circumstances, but in developing countries the problems can be particularly acute. First, the very nature of housing finance means that institutions are required to borrow short and lend long, thereby extending the conventional period of time before sustainable operations can be reached. Second, in economies with a shortage of capital the competition for funds is high and institutions may have to pay premiums in order to acquire capital, putting further pressure on their portfolio. Until the 1980s, most governments attempted to resolve these problems through the creation of designated public housing and finance institutions.

The Rise and Fall of Public-Sector Housing Finance Institutions

While many of these institutions assisted in the construction of large numbers of housing units, almost all have encountered severe financial problems and many have been wound up, privatized or obliged to take on private partners (Munjee 1994, Pugh 1994). One reason for this poor performance relates to the methods used to fund these institutions. Their reliance on the seemingly endless supply of funds from (sometimes non-redeemable) payroll levies, central government transfers or the enforced sale of government-backed stock to other public departments removed the pressure to be efficient (Boleat 1987, Buckley 1996, Rahman 1994, USAID 1997).6 In a number of countries, funds were the result of foreign loans which were to be repaid out of general government expenditure without the housing finance institution being accountable to the donor for their use or providing adequate details of repayment and subsidy rates (Rahman 1994, Valença 1992). In general, interest rates were often adjusted only periodically and were not subject to central bank control, monetary correction or the indexation of balances, aiding the steady path toward bankruptcy (Munjee 1994, UNCHS 1991b). The constant resource top-ups also removed any desire to innovate by developing new financial instruments, look for new client groups and offer bespoke finance packages. Nevertheless, some institutions expanded their remit to become housing and land developers without providing much evidence for having performed particularly well at their principal role.

A second characteristic of the public finance institutions has been a poor organizational record. Valença (1992:39) summarizes the conditions of Brazil’s housing finance system by the 1980s as one of ‘crisis, chaos and apathy’. Notoriously inadequate fund collection and loan enforcement rates exemplified these conditions. In Chile 60 per cent of loan recipients through the Basic Housing Programme were in arrears despite discounted interest rates, and about 99 per cent of loans given by the House Building Finance Corporation in Pakistan were in default although record-keeping was so poor that the precise figure is not known (Buckley and Mayo 1989, Malik 1994, Rojas and Greene 1995). Alarmingly, default rates were high even from households which had received large (if rarely transparent) levels of subsidy and despite some attempts to index repayments to wages (which were kept artificially low) rather than consumer prices, which were increasing at a faster rate (Buckley 1996).

These conditions were accentuated by political manipulation that passed institutions from one ministry to another at short intervals (Okpala 1994: 1577– 8, Valença 1992). Institutions also became a part of the ‘patronage bureaucracy’ serving sectoral interests to give favourable treatment to labour groups or to coopt opponents (Bond 1990, Klak and Smith, Siembieda and López this volume). In Ecuador, for example, employees of the Housing Bank were entitled to an annual mortgage subsidy three times the level of GDP per capita in addition to other generous benefits (Klak 1993:667). Having brought some of these groups into housing finance more as ‘vote banks’ than as clients there was a natural tendency to waive loan repayments and provide unconditional amnesties to defaulters at election time. In Sri Lanka, the Million Houses Programme was hijacked by political interests and eventually operated with only one-half of loan recipients making repayments on time or of the correct amount (Sirivardana 1986).

In the short term, this situation appeared sustainable so long as economic growth, low inflation, and stable exchange rates and commodity prices supported the large capital injections to cover subsidies and administrative inefficiency.7 However, as the economic crisis of the 1980s deepened, the fall in the real value of payroll deductions with rising unemployment, the diversion of revenue sources to fund higher priority areas of the government budget and the withdrawal of savings from negative interest rate bearing accounts left many institutions short of capital (Klak 1993, Rakodi 1995, Valença 1992). Between 1979 and 1989, assets per capita in financial institutions were held at very low levels and even fell, especially from 1985 to 1989 (UNCHS 1991b:12–14).8 The response was to ration lending and to depart from any pretence at social progression, by going up-market in the hope of finding borrowers with sufficient income to maintain payments (Buckley and Mayo 1989, Okpala 1994:1581, Valença 1992).

The declining effectiveness of housing finance institutions, coupled with economic and fiscal crises, have made governments more aware of the need to promote savings, reduce subsidies and mobilize domestic resources, and to motivate the involvement of private financial institutions (Buckley 1996, Kim 1997). Many of the most restrictive practices operating in housing finance markets, such as institutional entry requirements and liquidity limits, have been lowered, loan/value ratios made more flexible and a wider definition given to the terms of collateral.9 The optimistic view was that private institutions would be able to deliver larger quantities of finance more efficiently and with a greater chance for sustainability (Munjee 1994).

Certainly, there is evidence that deregulation and other reforms have promoted greater innovation, notably the development of dual-interest mortgages (DIMs) which allow payments to be indexed so that lenders are not ‘taxed’ through inflation, secondary mortgage markets, pension-linked housing finance and insurance-backed schemes (Buckley 1996, Kim 1997, Rakodi 1995). One of the best examples is the development in Chile of certificates which are issued with a mortgage, pay interest to the bearer and are traded on the stock exchange. The effe...

Table of contents

- Cover Page

- Half Title page

- Series page

- Title Page

- Copyright Page

- Dedication

- Contents

- List of figures

- List of tables

- Notes on contributors

- Preface

- Acknowledgements

- Part I Position papers

- Part II Formal and informal housing finance

- Part III Gender, NGOs and micro-finance

- Bibliography

- Index

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

- Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

- Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go.

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Housing and Finance in Developing Countries by Kavita Datta,Gareth Jones in PDF and/or ePUB format, as well as other popular books in Physical Sciences & Geography. We have over 1.5 million books available in our catalogue for you to explore.