![]()

1

Payments system innovations in the United States since 1945 and their implications for monetary policy

Lawrence H. White

The revolutions that haven’t yet happened

Monetary policy works through its control over the monetary base, the volume of the central bank’s monetary liabilities. (Central bankers typically prefer to think and talk about monetary policy working through changes in a targeted interest rate, but the central bank’s balance sheet holds the key to understanding what the central bank can do to influence interest rates and other variables.) The central bank’s monetary liabilities consist of paper currency (in the US, Federal Reserve notes) and commercial bank deposit balances held at the central bank (used for interbank settlements).1 Payment system innovations have potential consequences for the conduct of monetary policy if they provide such close substitutes that they significantly reduce the scale or increase the interest-elasticity of demand for central-bank-issued currency or central-bank-issued settlement deposits.

Recent innovations that may provide close substitutes for paper currency include such electronic money devices as card-based, mobile-phone-based, and personal-computer-based means for consumers to hold and transfer spendable balances. Innovations that may provide close substitutes for central-bank settlement balances include deposit-transfer systems that settle outside the central bank’s books, such as PayPal, e-gold and deposit transfers cleared and settled by private systems (private automated clearinghouses and ATM networks).

In a 1996 interview banker Walter Wriston declared that digital currency carried on smart cards was ‘the revolution that’s waiting in the woods’ and a ‘technology … on the verge of exploding’ (Bass 1996). The predicted explosion has yet to happen.

Monetary economists (Cronin and Dowd 2001; Friedman 1999) and central bankers (BIS 1996; King 1999) have envisioned serious consequences for – perhaps the complete disappearance of – monetary policy should privately issued electronic money completely displace central bank liabilities. The literature on e-money in this respect resembles the earlier literature on the ‘legal restrictions theory’ of money demand,2 which envisioned the complete displacement of central bank liabilities by higher-yielding bonds in the absence of legal restrictions. Cronin and Dowd (2001, 227) foresee that

One BIS (1996, 2) report posits that e-money innovations ‘have the potential to challenge the predominant role of cash for making small-value payments’ by dint of their greater convenience, but worries that therefore ‘they also raise a number of policy issues for central banks because of the possible implications for central bank seigniorage revenues and monetary policy and because of central banks’ general interest in payment systems’. To date, the displacement of paper currency by e-money has been a non-event for US monetary policy makers.

At the 1999 Jackson Hole conference on ‘New Challenges for Monetary Policy’, sponsored by the Federal Reserve Bank of Kansas City, the Bank of England’s Deputy Governor Mervyn King (1999, 49) declared that, with enough computing power,

The Federal Reserve System’s role in clearing and settlement has, if anything, grown since 1999. At the 2003 Jackson Hole conference, where the topic was ‘Monetary Policy and Uncertainty: Adapting to a Changing Economy’, the changes and uncertainty posed by e-money and private settlement were never mentioned as a concern.3

Credit and debit cards

Between 1945 and 2000, the proliferations of credit cards and later debit cards were the most visible developments in US retail payments. Credit card systems grew to handle nearly one-fourth of US retail payments. The effects that these developments had on monetary policy, through their effects on the demand for central bank money, may give us some hint as to what we might expect from payment innovations now in prospect.

Sellers have extended credit to their customers for centuries. The growth of multi-outlet retail chains (most notably of gasoline stations and department stores) in the early twentieth century led to the formalisation of standing credit authorisations and their representation by company ‘charge cards’ that could be used for charging purchases at any of the company’s outlets. Such single-company cards were supplemented by ‘travel and entertainment’ cards beginning in 1950. The first of these was the Diners Club card, initially accepted by 14 restaurants in New York City. American Express, then a leading issuer of traveler’s cheques, launched a more widely accepted T&E card in 1958. Unlike some retail chains, Diners Club and American Express expected the consumer to pay his charge balance in full at the end of each month.

Meanwhile various banks, the first of which may have been Franklin National Bank in New York in 1951, began issuing their own ‘universal’ credit cards combining widespread acceptance with the opportunity to defer repayment beyond the end of the month. Because US laws at the time restricted each bank to operating in a single state or city, each bank card was similarly limited at first, accepted only by the local retailers that the bank had signed up. Bank of America, then the largest bank in California with branches throughout the state, launched its Bank Americard in 1958. It took the card nationwide through licensing agreements with banks in other states beginning in 1966. An alliance of other California banks, seeking to build a network large enough to challenge the BankAmericard, formed a reciprocal bankcard-acceptance arrangement called the Interbank Card Association in 1966, and quickly began signing up banks in other states. The association adopted the ‘Master Charge’ brand in 1969. Bank of America responded to the challenge by transferring ownership of its card brand to a similar association of issuing banks in 1970. The association licensed the card internationally, renaming it Visa in 1976. Master Charge became MasterCard in 1979.4

A third universal card, the Discover Card, was introduced by the nationwide Sears retail chain through a financial services subsidiary in 1985. American Express introduced its own universal credit card, the Optima Card, in 1987.

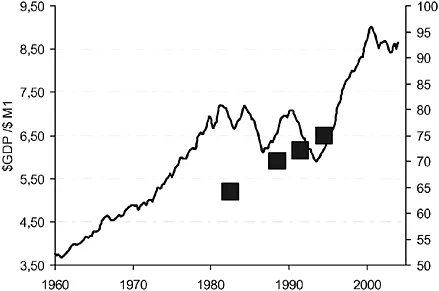

Credit card penetration became high in the 1970s and has continued to rise at an even pace, as measured by the share of US households having at least one credit card. According to the Federal Reserve System’s Surveys of Consumer Finances (Yoo 1998, 21), the share stood at 64 per cent in 1983, 70 per cent in 1989, 72 per cent in 1992, and 75 per cent in 1995.

Some economists in the 1970s extrapolated from the growth of credit card use to the notion that credit cards would soon almost completely supplant cash and cheque payments, making the monetary aggregates irrelevant. Brunner and Meltzer (1990, 358 n. 1) later commented:

Cross-sectionally, as one would expect, credit card ownership is associated with smaller holdings of demand deposits (Duca and Whitesell 1995). But in time series the velocity of US$ M1, as Bruner and Meltzer indicated, declined after 1980

despite the continued growth in the use of credit cards (see Figure 1.1). The leading explanations for the post-1980 break in the path of...