- 400 pages

- English

- ePUB (mobile friendly)

- Available on iOS & Android

eBook - ePub

About this book

At the beginning of the 1990s, Korean firms embarked on an impressive wave of direct investment abroad. This dramatic multinationalization was considered as yet another sign of Korea's remarkable economic performance, especially as a high proportion of the foreign ventures were located in advanced countries. But this unbalanced quest for globalization actually tested the 'Korean model' to its limits; after the 1997 crisis a new policy prepared the way for a surge of inward investment. Using empirical tests and case-studies, this collection shows that Korean groups have invested in developed countries to jump over trade barriers, but also to source advanced technology and marketing capabilities. Moreover, their ambitious strategies have been stimulated by oligopolistic rivalry among the chaebols.

From a policy perspective, the book provides an original discussion of national ownership by questioning the substitutability between inward and outward foreign investment and its relationship with the evolution of the national innovation system. By shedding light on the pattern of Korea's internationalization, these essays make a valuable contribution to the theory of international production and provide important insights for the current policy debates on globalization and innovation-led growth.

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Study more efficiently using our study tools.

Information

Subtopic

Business GeneralIndex

BusinessSIX

The International Development of the Korean Automobile Industry

INTRODUCTION

The South Korean automobile industry was simply not on the world manufacturing map in the 1970s. During the two following decades, however, it has grown extraordinarily rapidly. Between 1975 and 1996, its production increased by a factor of 75, from 37,000 units to over 2.8 million units. At the end of this period, South Korea was ranked 5th in the world automobile industry, with a 5.3 per cent share of global production, and automobile firms were planning massive new investments.

This successful development is unique in recent history. Over the last 50 years, no country other than South Korea has followed the Japanese path and fostered the emergence of indigenous automobile manufacturers1.

The Korean experience is also unique as far as internationalization is concerned. Economic theory has traditionally insisted on the role of firms’ competitive advantages in explaining foreign investment.2 Indeed, internationalization in the automobile industry has always been driven by firms’ ownership advantages, from the early foreign investments of GM and Ford in Europe and Japan, based on their lead in mass-production technology, to the more recent Japanese expansion abroad, based on ‘lean’ production methods. In the case of Korean manufacturers, however, the reverse causal sequence gives a better explanation of their internationalization process. Their recent foreign investment drive has been primarily motivated by the need to overcome competitive disadvantages. Indeed, the export expansion and the rise of foreign production in the 1990s have resulted from the firms need to catch up rapidly with their foreign competitors in terms of size. The Korean automobile industry has been engaged in a ‘capacity-push’ growth since the early 1980s, in which capacity expansion has always been ahead of the demand. This over-investment strategy aimed at drastically reducing catching-up time by accumulating faster learning and scale economies. Thus, the initially limited size of the domestic market, the fierce competition among Korean makers and the absolute necessity to increase volume to pay off huge investments forced them to export early on. In the mid 1990s, however, despite their remarkable growth Korean carmakers were still small compared with foreign mass-producers. At the time, Korean firms had not yet acquired a significant competitive advantage within the world oligopoly, in terms of product quality, productivity or technology. Accordingly, they had to keep on growing at a fast pace because volume expansion was the easiest way to catch up in terms of productivity and technology. But the domestic market ended its rapid climb, while the traditional export markets could not absorb the large additional volumes that Korean firms had planned to sell. However, the largest emerging markets — namely the ones with the greatest growth potential — remained almost untouched by export strategies, and firms realized that investing abroad had become the best way to speed up their expansion.

Since basic information on Korean firms’ strategies, especially abroad, has often been confusing, the first goal of this chapter is to evaluate the true scope of Korean carmakers’ foreign operations and to present their specificities in the late 1990s, before the industry restructuring. At a more theoretical level, the paper argues that competitiveness has been the goal rather than the source of Korean automobile firms’ foreign investment drive. Foreign direct investments are thus becoming an integral part of their catching-up strategy. Furthermore, Korean carmakers’ competitive position within the world oligopoly explains their location choices. Section I presents the stylized facts of the Korean automobile industry development and its main outcomes, underscoring the lack of economies of scale and of any specific competitive advantage within the industry. Section II describes how Korean firms have stepped up their exports and diversified into foreign markets. Section III provides key figures of their foreign involvement and an analysis of outward direct investment (ODI) location and implementation strategies for Korean carmakers.

CATCHING UP IN A MASS PRODUCTION INDUSTRY

The development of an automobile firm requires adequate technological skills, a market large enough to exploit economies of scale and an efficient network of component suppliers. In leading countries these different components of the ‘automobile system’ have grown in parallel, whereas the Korean strategy has been characterized by unbalanced development. As a result, Korean carmakers have been able to grow faster, but their competitiveness and technological base have remained fragile.

The capacity-push strategy of the Korean automobile industry

Like many modern East Asian industries, the Korean automobile industry was built without initial comparative advantages. Korean firms had no technology, no capital and no supporting industry. Even demand was lacking, since the Korean automobile market stayed far below 100,000 units until the early 1980s. The main features of its successful development have been the aggressive investment strategy backed by strong support from the government and the use of strategic short-cuts to reduce the catching-up period.

State’s support and strategic short-cuts

For the past three decades, the automobile industry has been regarded as a major strategic industry in Korea. During this period, the Korean government has promoted the industry through different means, including preferential credit allocations, protection of the domestic market and export incentives. It has also implemented regulating policies and restructuring measures. The main objective was to achieve economies of scale rapidly which, combined with relatively low wages, could give Korean carmakers a competitive advantage despite their lack of manufacturing experience and technology. However, industrial policy has always favored several firms in the sector in order to stimulate efficiency and limit market power. These sometimes incompatible policy goals explain the succession of rationalization measures (to allow firms to attain a critical size) and liberalization measures (to develop competition).

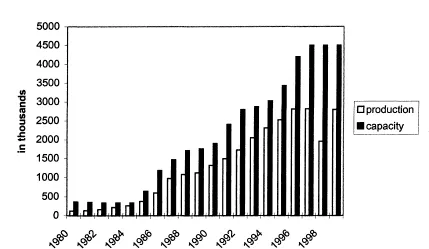

The firms’ aggressive investment strategies, combined with the flow of State-controlled bank financing, have locked the automobile industry into a ‘capacity-push’ growth since the early 1980s.3 Although production increased by a factor of 23 between 1980 and 1996, capacity expansion has always been one step ahead. Korean manufacturers have created the potential for the third or fourth largest industry in the world. Despite a worldwide automobile over-capacity estimated at 30 per cent, Daewoo inaugurated a new USD 1.2 billion plant in Kunsan in April 1997, with an annual capacity of 320 000 units. At the time, the three main carmakers were planning on a production capacity of 7 million units by the year 2000, betting on growth in such developing markets as China, Indonesia and Russia.

Figure 6.1 Production and capacity

Source: KAMA

The most impressive characteristic of Korean automobile industry development has undoubtedly been its fast-paced growth, made possible by three strategic short-cuts: intense technology transfers from advanced producers, early export orientation to tap foreign demand, and a bias towards in-house production of components.

Already back in 1974, Kia embarked on the production under license of a Mazda vehicle, Saehan (formerly Daewoo Motor) launched a similar cooperation scheme with Isuzu, while Hyundai tried to open the ‘technological package’ by contracting with different technology suppliers. To build a ‘national car’, the Pony, Hyundai used an Italian design (Ital design), core components from Japan (Mitsubishi) and English engineers (from British-Leyland). Later on, increasing strategic autonomy in the context of structural dependence on foreign technology became a major objective. In terms of strategy, Hyundai has stressed self-reliance the most. The company failed to complete joint venture negotiations with Ford in 1972 and with GM in 1981 notably because Hyundai did not want to lose managerial control and limit its access to export markets.4 It has relied heavily on technology licensing to develop its model range and manufacturing process.5 Mitsubishi Motors soon became its main technological partner, but Hyundai managed to avoid an exclusive partnership and diversified its technology sources (see Appendix 6.A1). In contrast, Daewoo Motor initially operated within the framework of General Motor’s global strategy, following a joint venture agreement. Technology transfers from GM and its affiliates allowed Daewoo Motor to enter the mass production stage without developing its own technology. But the GM-Daewoo partnership became shaky in the 1980s and ended up in 1992 with GM disengaging. However, the GM group has remained an important technology supplier for Daewoo.6 Despite their late entry and small size, Korean firms have been particularly successful in turning their initially unbalanced relationships with leading MNEs to their advantage. By blocking any direct access to the Korean market, the State has reinforced the bargaining power of local firms.

Initially the domestic market was unable to absorb large volumes of cars. Thus Korean firms’ rapid growth strategies implied the development of foreign sales. Various governmental incentives have guided them along the export route at an early stage.7 Prior to 1984, there were almost no exports — a total of less than 150,000 cars had been exported, mainly to less industrialized countries (South-East Asia, Middle East). By 1988, however, exports, aimed almost exclusively at the North American markets, had surged to a peak of 576,000 units. As it is well known, Korean exports nose-dived, declining by almost 40 per cent in the next two years.

However, the rapid growth of the Korean industry has continued unabated, despite the pessimism of many analysts.8 This is primarily due to the take off of the domestic market, whose explosive growth has more than offset the decline in exports (see Figure 6.2). Indeed, the partial withdrawal from North-America ensured an adequate supply for Korean salarymen, impatient to enter the mass consumption stage.9 Yet the domestic market has been rapidly maturing and exports are once again increasingly the driving force behind the sector.

In Korea, vertical integration has been used extensively to reach a high local content ratio early on and to accelerate the development of a complete manufacturing base. The industrial concentration process of the 1970s weakened small- and medium-sized businesses. Once they entered the mass production stage, Korean carmakers invested heavily in their own parts and components facilities. Furthermore, imported components were necessary to meet quality standards on export markets.10 This preference for in-house productions and imports reduced the available market for independent components firms, hence their growth and development.11 The carmakers’ internalization ratio has remained high by world standards, around 50 per cent in the early 1990s (Chung, 1994; Lautier, 1993). As a result, the industry’s growth and tec...

Table of contents

- Front Cover

- Half Title

- Studies in Global Competition

- Title Page

- Copyright

- Contents

- Preface

- NOTES ON CHAPTER CONTRIBUTORS

- ONE: Emerging Multinationals: The Main Issues

- TWO: A Case of Government-Led Integration into the World Economy

- THREE: Korean Direct Investment in North America and Europe: Patterns and Determinants

- FOUR: Korean Multinationals’ Strategies and International Learning

- FIVE: The Internationalization of Korean Electronics Firms: Domestic Rivalry and Tariff-Jumping

- SIX: The International Development of the Korean Automobile Industry

- SEVEN: Technological Catching-Up through Overseas Direct Investment: Samsung’s Camera Business

- EIGHT: Alice Amsden, René Belderbos, John Cantwell, Byungki Ha, Pierre Jacquet, Randall Jones,

- NINE: Globalization and Korea’s Development Trajectory: The Roles of Domestic and Foreign Multinationals

- Index

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

- Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

- Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go.

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Going Multinational by Frédérique Sachwald in PDF and/or ePUB format, as well as other popular books in Business & Business General. We have over 1.5 million books available in our catalogue for you to explore.