eBook - ePub

Management Accounting in Support of Strategy

How Management Accounting Can Aid the Strategic Management Process

- 186 pages

- English

- ePUB (mobile friendly)

- Available on iOS & Android

eBook - ePub

Management Accounting in Support of Strategy

How Management Accounting Can Aid the Strategic Management Process

About this book

Management Accounting in Support of Strategy explores how management accounting can support the strategic management process of analysis, formulation, implementation, evaluation, monitoring, and control. If the management accountant is to add value to the business they need to understand how the business works. The toolbox available to the management accountant does not just contain the accounting techniques, but also includes the strategy models and frameworks described in this book. Armed with this array of tools the management accountant is well placed to add significant value to the business. The reader will gain an understanding of the strategic management framework, strategic models and tools, and how management accounting can support the strategic management process. It will be beneficial for undergraduate and postgraduate course students studying strategy or management accounting. The book will also enable practicing accountants to understand how they can make a significant contribution to the success of their organization by demonstrating how management accounting can be used in support of strategy.

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Study more efficiently using our study tools.

Information

CHAPTER 1

Management Accounting and the Strategic Management Framework

What Is Management Accounting?

Traditionally management accounting has been distinguished from financial accounting by its focus on providing information for management activities. Definitions of management accounting in the 1970s encompassed activities such as providing support for managerial decision making, allocating resources, monitoring, and evaluating performance. Techniques such as budgeting and variance analysis to aid planning and control were commonplace, as were techniques such as investment appraisal and cost volume profit analysis. These techniques are still utilized today yet many of the traditional management accounting techniques and management information provided have been criticized over the years as being inappropriate for modern business. The information provided was typically internally generated and financial in nature, with a focus on accurately recording the cost of products, and monitoring performance via productivity and efficiency ratios. The principal criticism being that management accounting was focused on short-term operational decision making. There was a presumption that the accountant was merely the person with the numbers and the finance role was often devoiced from the development of strategy within the organization. Kaplan (1984) notably commented that management accounting should not be seen as a set of prescribed procedures and systems that could be applied universally, but that it should be tailored to serve the needs of the strategic objectives of the firm. Indeed, it is now understood that the management accounting system is contingent upon the organization’s strategy, that is, there is not a one-size-fits-all accounting system.

During the 1980s and 1990s it was accepted that management accounting needed to develop to meet the changing requirements of business. As the business environment became more competitive, and the emphasis moved from long-range planning to strategic management, the call was not only for management accounting practices to respond to the changing needs of business, but also for accountants to become more involved in the strategic management process. This has been recognized in more recent definitions of management accounting. The Institute of Management Accountants (2008, p. 1) definition includes the phrases “partnering in management decision making” and “to assist management in the formulation and implementation of an organization’s strategy.” This indicates that the accountant is no longer seen as just the person with the numbers but is an active member of the management team involved in the strategic management process.

The Development of Strategic Management Accounting

During the 1980s and 1990s the concept of strategic management accounting emerged partly in response to the criticism that traditional management accounting was not serving the needs of strategic management. Various authors promoted aspects of information to aid strategy development. Simmonds (1981) focused his attention on the need for external information and in particular that which related to competitors and markets. Bromwich (1988) emphasized gathering and analyzing information pertaining to competitors and the benefits to customers over the long term; Govindarajan and Shank (1992) developed the concept of strategic cost management; Roslender and Hart (2003) focused on merging management accounting and marketing concepts within a strategic framework. Despite numerous offerings, a clear and agreed definition of strategic management accounting is yet to emerge from the published literature, but there is agreement that it involves providing information that supports strategic decision making. There has been a shift from providing information purely related to internal, quantitative, financial, past performance, and short-term decision making, to recognizing the need to include external, qualitative, nonfinancial, long-term, and future-oriented information.

Following the introduction of strategic management accounting to the literature a growing number of studies have been published that seek to ascertain the degree to which the new accounting techniques have been adopted in practice. A further difficulty, however, is that there is no definitive agreement on what constitutes a strategic management accounting technique. For example, Guilding, Cravens, and Tayles (2000) defined 12 techniques; Cadez (2006) defined 17 techniques; Cinquini and Tenucci (2007) defined 14 techniques; and Cadez and Guilding (2008) defined 16 techniques. A brief explanation of each technique is provided in Appendix A.

Various surveys over the past few decades have reported limited adoption and utilization of the defined strategic management accounting techniques and, although research suggests that practicing managers and accountants can see potential benefits in the use of the newer techniques, there is a tendency to prefer the tried and tested conventional management accounting techniques (McLellan 2014). More recent studies undertaken in specific industry sectors have indicated that some of the techniques ascribed to strategic management accounting are being adopted, for example, Oboh and Ajibolade (2017) in the Nigerian banking sector. However, it is still fair to say, as studies by Langfield-Smith (2008), Nixon and Burns (2012), and Pitcher (2015) have identified, that the term strategic management accounting has not as yet entered the lexicon of the accounting practitioner. These, and other studies do, however, find evidence that management accounting, whether conventional or strategic, is being used to aid strategic decisions and support the strategic management process.

Strategic Management

In the 1950s and 1960s management writers were discussing long-range planning. In many cases organizations were taking their annual budgets and extending them for a period of 5 to 10 years, thus creating a long-range plan. In the 1970s, and particularly in the 1980s, the focus shifted toward strategic planning as markets became more competitive. Toward the end of the 1980s and into the 1990s the focus changed again, this time toward strategic management, as organizations needed to become more responsive to changes in what was becoming a more dynamic and complex business environment. The original intension of strategic management accounting was that the information provided should aid strategic decision making and the strategic management process.

Here arises another difficulty—how to define the strategic management process. It is often described as a series of phases such as formulation, implementation, and evaluation of the strategy. A more encompassing and generally accepted definition is offered by Nixon and Burns (2012, p. 229) as containing the following key activities: “(1) development of a grand strategy, purpose or sense of direction, (2) formulation of strategic goals and plans to achieve them, (3) implementation of plans, and (4) monitoring, evaluation and corrective action.” This portrays the process as a routinized and formal process, and although many firms still adopt a formal planning process it is also recognized that strategic decisions are often complex, nonlinear, and fragmented, and that the strategic management process is fluid and iterative in nature.

The Strategic Management Framework

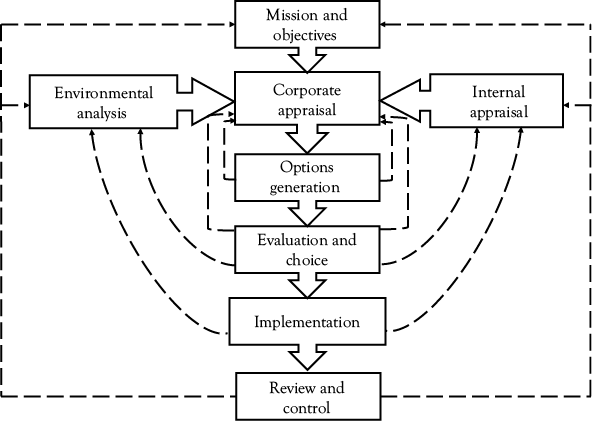

Academic and practitioner texts discuss various methods, processes, and frameworks for the development of strategic plans. This section provides an outline of a strategic management framework (Figure 1.1). It is based on the concept of a rational approach to strategic planning and forms a structure for the subsequent chapters. The explanation here is therefore deliberately brief as each element is discussed in detail later.

Figure 1.1 The strategic management framework

The framework incorporates key phases of analysis encompassing the external and internal analysis resulting in the corporate appraisal or SWOT (strengths, weaknesses, opportunities, and threats), the generation and evaluation of strategic options and strategic choice, followed by implementation, and finally the review, evaluation, and control of the current strategy. The dotted lines illustrate the iterative nature of the process.

Mission and Objectives

The mission is the rationale behind the business. It sets out the long-term aims and purpose of the organization as well as indicating the strategy, values, policies, and behavior standards. Organizations often develop a vision alongside the mission. This is usually broader, and shorter, than the mission statement and is often intended as a point of inspiration for employees to drive the business forward. It is common for organizations to promote their vision, mission, and the values that underpin these statements on their websites. This is extended for internal consumption to include the strategy and tactics, which creates a VMOST statement: vision, mission, objectives, strategy, and tactics. The objectives are more specific and set out what the organization aims to achieve. Ideally, they should be specific, measurable, agreed, realistic, and time bound (SMART).

Environmental Analysis

The environmental analysis is the subject of Chapter 2 and provides a means for identifying external factors that could affect an organization’s ability to achieve its objectives. A strategic tool known as PESTEL (political, economic, sociocultural, technological, environmental, and legal) provides a framework that can be utilized to analyze changes in the general business environment. The focus of the analysis is on how the changes will impact on the industry and hence the organization. Models such as Porter’s Five Forces (Porter 1979) can aid the analysis at an industry level to identify the forces that will impact on the profitability and attractiveness of the industry, now and in the future. Competitor analysis is also a key area in this stage of analysis. Strategically the analysis helps to identify the opportunities and threats to the organization that are evident, or could emerge, from the business environment.

Internal Appraisal

The internal appraisal analyzes the organization’s resource capability to achieve its objectives, given that environmental factors will impact on this ability. Various models can be utilized to aid the analysis, which are discussed in Chapter 3. These fit within a simple framework known as the 9 Ms: manpower, money, markets, machinery, materials, makeup, methods, management, and management information. These headings need to be viewed as pointing to broad areas requiring a detailed analysis. The analysis helps to identify strengths and weaknesses.

Corporate Appraisal

This pulls together the issues identified during the environmental analysis and internal appraisal and is the subject of Chapter 4. The environmental analysis is the source of opportunities and threats, while the internal appraisal is the source of strengths and weaknesses. However, during the environmental analysis it is not known whether a change creates an opportunity, or a threat, until this has been reviewed in light of the resource capability. It is not until the ability of the organization to deal with the change has been assessed that it emerges as an opportunity or a threat, hence the corporate appraisal provides the framework in which this can be identified. It is also worth noting that changes in the environment can provide an opportunity for some organizations while creating a threat for others, depending on the organization’s ability to deal with the change. This has a strong connection to competitor analysis as strengths and weaknesses can be judged to be relative to competitors and a source of competitive advantage. Once identified, strategies can then be formulated that build on the strengths, address the weaknesses, grasp the opportunities, and minimize or avoid the threats, and that are consistent with the mission and objectives.

As part of the corporate appraisal a GAP analysis can be undertaken that ascertains the gap between an organization’s stated objectives and the level of performance that will be achieved based on the current strategy, given the changes in the environment and its current resource position. If a gap is identified it requires the formulation and evaluation of strategic options to close the gap.

Options Generation

Strategic options can be considered under the he...

Table of contents

- Cover

- halftitle

- title

- copyrights

- dedication

- abstract

- contents

- Preface

- Ack

- 01_Chapter 1

- 02_Chapter 2

- 03_Chapter 3

- 04_Chapter 4

- 05_Chapter 5

- 06_Chapter 6

- 07_Chapter 7

- 08_Chapter 8

- 09_Chapter 9

- 10_Chapter 10

- 11_Chapter 11

- 12_Appendix A

- 13_Appendix B

- 14_References

- 15_Bios

- 16_Index

- 17_Adpage

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go.

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Management Accounting in Support of Strategy by Graham S. Pitcher in PDF and/or ePUB format, as well as other popular books in Business & Managerial Accounting. We have over 1.5 million books available in our catalogue for you to explore.