![]()

PART 1

Advanced Service Management

in the Service Industries

![]()

1

Profit Sharing that Motivates

Inter-Firm Cooperation within

a Convenience Store Chain

Yasuhiro Monden

University of Tsukuba

Noriko Hoshi

Hakuoh University

1 Purpose of the Study

In an inter-firm network that consists of a franchiser and so many franchisees, profit sharing is something that requires much consideration if cooperation between the two parties is to be encouraged. The author has long been exploring the concept of the “incentive price” (i.e. price for profit allocation) and its application to the members of inter-firm network for motivating their cooperation, through a series of papers of Monden (2009a; 2009b; 2010; 2012) and Monden and Nagao (1987–1988). As one of similar courses of research, Mouritsen and Thrane (2006) also advocated that the profit allocation function as a “self-regulation mechanism” by transfer prices, taxes and fees would coordinate the relationships among member firms of network. This theme is also the basic focus of the study. In this chapter, this focus is maintained as we examine various types of profit sharing structures that would motivate participation and cooperation on the part of the franchiser of a convenience-store chain and its franchisees. We would like to verify the correlations among the items listed below, in considering profit sharing.

- (1) Differences in terms, when investing in or leasing store property

- (2) Differences in royalty rates, from company to company

- (3) Sharing the risk of disposal loss

- (4) Differences in franchise fees, from company to company

- (5) Sharing the risk of profit-earning among stores

- (6) Sharing the cost for interior finishing work

- (7) Sharing the cost of utilities

However, in this analysis, we do not consider factors such as the large amounts of initial investment made by the franchiser, operational costs, direct financing by the franchiser, or loan guarantees upon opening the store. In this chapter, we would like to construct a general proposition through analysis, by focusing on the case of Seven-Eleven Japan Co., Ltd. (hereafter abbreviated as SEJ), the most well known of all convenience store chains, and by examining complementary data from other chains.

2 Different types of Franchisees Based on the Amount of Initial Investment

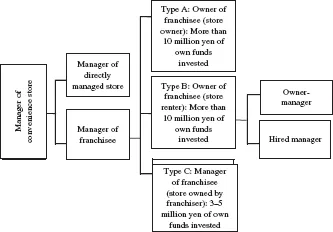

First, we would like to classify franchisees into categories, based on the amount of initial investment made upon opening the store (Fig. 1).

The word “owner”, used in the sense of “owner of franchisee’s store” on the right-hand-side of Fig. 1, does not denote that the person is the owner of the store property as listed in the register book; it means that the person is the store manager and owns more than 50% of the amount of investment made in the store. In other words, the store manager has invested his or her own funds, and those funds represent the majority of fund sourcing, shown as the owners’ equity in the balance sheet of the store. Therefore, a Type B franchisee — who rents store property and pays rent — is associated with this type of owner.

Fig. 1. Classification of convenience store managers.

3 Differences in Royalty Rates Dependent on the Amount of Initial Investment

A convenience store manager assigned a store prepared by the franchiser need only bear the cost of interior finishing work as the initial cost; this means that, for the manager, the risk of not recovering his or her initial investment is very low. However, “low risk” comes “low returns” (i.e., low revenues). On the other hand, in cases where the owner-manager bears the initial investment, which incurs a “high risk”, there should be “high returns” (i.e., high revenues).

According to the degree of risk by the amount of initial investment, an “owner of a franchisee store” — as we refer to him or her here — is charged a low royalty rate, whereas a “manager of a franchisee store” is charged a high royalty rate. Therefore, the “income” (i.e., gross profits on sales minus royalty) received by the store manager would be relatively high in the former case, and relatively low in the latter.

Type A (Franchisee candidate owns land and building)

The royalty charged by SEJ (called as “Seven-Eleven charge”) is 43% of the gross profit on sales. However, after a period of five years or following the renewal of a 15-year contract, the rate may decrease, according to the terms in each case.1

Type C (Franchisee candidate with land and building provided by franchiser)

With this type, the franchiser prepares land and arranges for the building of the store; the franchisee need not even pay rent for the property.

In the case of SEJ, since the franchiser pays rent for the land and building, the royalty charged would naturally be higher than with Type A. The rate would increase on a sliding scale according to the gross profit on sales: 56% for gross profit on sales up to 2.5 million yen, 66% for over 2.5 million yen and up to 4 million yen, 71% for over 4 million yen and up to 5.5 million yen, and 76% for over 5.5 million yen (see Sakakibara, 2010, p. 14). However, after a period of 5 years or following the renewal of a 15-year contract, among other cases, the rate charged may decrease according to the terms of each case.2 Thus, Type C is a business with low risk and low return.

Type B (Franchisee candidate rents store space on his or her own, under his or her own name)

This is a contract type that each of Circle K Sunkus, Ministop, and Daily Yamazaki has adopted, but others have not. Thus, this type is a rather special case.

In most cases, the franchisee itself becomes a tenant in apartment buildings, commercial buildings, and shopping malls. Renting a space costs approximately 10–15 million yen, in the form of costs such as the initial deposit, the guarantee payment, interior finishing work, and various fees. Even when renting a store space, property tenancy usually requires considerable initial investment; this includes not only the rent, but also key money and a considerable amount of guarantee payment (deposit) to the renter, as well as commissions to the real estate agent.

Since the royalty rate of Type B is the same as that charged for Type A above, the income of the store is high. At the same time, however, owing to the contract period with the franchiser (i.e., 7–10 years) or the lease contract with the store property owner, the franchisee cannot easily withdraw from the business, even when faced with sluggish sales. These conditions suggest that this type of business is also “high risk, high return”, just like Type A.

There are also cases in which a franchiser would prepare the store property or rent a space and pay the rent. Again, however, the royalty rate is the same as that charged for Type A, which means that the business is both “high risk” and “high return”.

4 Relationship between Royalty Rates

and Break-Even Point

Before becoming a franchisee of a certain chain, those who are considering becoming a franchisee of a convenience store chain need to compare the terms of each chain in order to make an advisable buying decision. In this sense, the principle of market competition would play a role among the chains before a prospective franchisee chooses a certain chain, and the principle of market price would influence royalty, sharing, and other kinds of rates.

At this point, it is quite difficult to choose which chain would be the best investment among the many convenience store chains. Takeuchi (2001, p. 227) describes the elements inherent in the decision-making process as follows: “In the case of major chains with a large number of stores, we can expect to see a store with high daily sales (amount of sales per day), but on the flipside, the royalty is high and the benefit in terms of revenue would be low. On the other hand, in the case of chains going in a direction different from the major chains, such as Daily Yamazaki, Circle K Sunkus, Ministop, and am/pm, daily sales might be low but the royalty rate would also be low, thus resulting in high profit margin.”

In this respect, the following is our perspective vis-à-vis the relationship between royalty rates and the break-even point. Since chains with higher average daily sales or higher average annual sales charge higher royalty rates, the “gross profit after loyalty” of the convenience store (= [gross profit on sales – royalty] = [sales volume – cost of goods sold – royalty] = [sales volume – total variable cost]) would be relatively low. Assuming that the fixed costs are identical across all stores, then:

According to this formula, chains with higher annual sales per store would have a relatively lower contribution margin ratio. As a result, the “breakeven point”, calculated as the fixed cost/contribution margin ratio, should be relatively high. Therefore, a store would need to achieve considerable sales volumes to run into the black. On the other hand, since chains with small annual sales would have low royalty rates, the “contribution margin ratio” of the above would be relatively high, and the break-even point would be relatively low. Therefore, the store would be able to run into the black even with relatively low sales volumes.

5 Method of Calculating Royalty and Bearing

the Cost of Disposal Loss, and Sharing the Risk

of Disposal Loss

5.1 Is a system in which the store owner bears

the full disposal loss socially just?

As long as the store is responsible for ordering stock, the store owner is of course responsible for bearing “disposal losses”. However, we believe it socially unfair for the store owner to bear the full risk of disposal loss, given that, in reality, the occurrence of disposal loss is significantly dependent on the strategies of the franchiser. Franchisers say “avoid opportunity loss” (in other words, lost sales opportunities as a result of being out of stock on certain items) and alert their franchisees to follow through with an active ordering strategy. If franchisees place large orders according to this strategy set by the franchiser, the risk of generating a “disposal loss” would naturally increase. Therefore, we consider it problematic to hold franchisees entirely responsible for disposal losses and have them fully bear the risk thereof. Additionally, if the sales volume of a franchisee increases by producing a disposal loss, then the commission received by the franchiser would increase. Clearly, a system in which franchisees must bear the risk of disposal loss while franchisees receive profits from large orders is not balanced.

Ryuichi Isaka, President of SEJ, was quoted as saying that “If franchisees are worried about disposal loss and hold off placing orders, we would not be able to provide enough items (to the customers)” (The Nikkei, June 24, 2009). This statement suggests that the franchiser places more emphasis on avoiding “out-of-stock loss” than on avoidin...