![]()

1

Introduction

“When you are hungry, you go to the kitchen.”

This book is about market practice in the modelling of financial derivatives. The intent is to discuss the essential features that a model needs to capture to appropriately treat various financial products. But we must start somewhere. To avoid boring the initiated, basic familiarity with stochastic calculus and a good grounding in mathematics is assumed. But for clarity, it will nevertheless be useful to go through a few key ideas that are fundamental to the pricing of derivatives.

This chapter breezes through the basics of derivatives pricing and various key considerations, as well as introduces various market quantities, so that the reader can relate the discussion to market observables, rather than see it from only an abstract sense.

1.1 The Theory

Derivatives pricing is theoretically anchored in the concept of replication. Basically, the premise is that if you have two portfolios whose payoffs are equivalent at a future date, then their values must be equivalent today. If we ignore the possible need to liquidate these portfolios prior to that future date, the possibility of the counterparty of one of the portfolios defaulting, and the potential cost differentials of funding these two portfolios, this statement is uncontroversial.

It follows that to price a derivative, it is sufficient if you could come up with a replicating portfolio. Notice that in this case, we are not concerned about what happens to the underlying itself, or indeed if it is overpriced.

Further, if this replicating portfolio can be constructed today (independent of model assumptions), then you can price the derivative with confidence, since it is just a combination of existing traded market products. That is the realm of static replication, which we shall cover in Chapter 3.

More frequently, it is necessary for the replicating portfolio to be dynamic, i.e. you may have to rebalance it over time, and the rebalancing is dependent on certain model assumptions. In this way, pricing of derivatives becomes dependent on the model chosen for the underlying.

Let us now investigate what this means in practical terms.

1.1.1 Ito’s Lemma

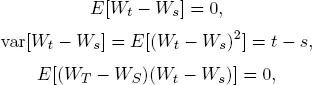

Let us start with a Wiener process Wt. Amongst its properties, it is continuous and has independent random increments that are normally distributed, i.e. for s < t <S < T:

and

There are arguments that a continuous process cannot properly represent market quantities since they tend to jump. For example, negative shocks (e.g. a major disaster or credit event) can cause stock prices to drop sharply instantaneously. And interest rates at the short end tend to be changed by 25 basis points (from central bank action) or nothing at all. But for longer expiries and for hedging considerations for derivatives where we are worried about how the 10-year euro swap rate moves or changes in the forward value of the S&P 500 over the next three years, jumps are not very meaningful, since they disproportionately affect the short term but their effect is smoothed out over time. To this end, it is beyond the scope of this book to investigate jump processes, and because of their practical utility, we shall focus on processes constructed out of Wiener processes instead.

So, let us now consider the following stochastic differential equation (SDE) for the process of an asset

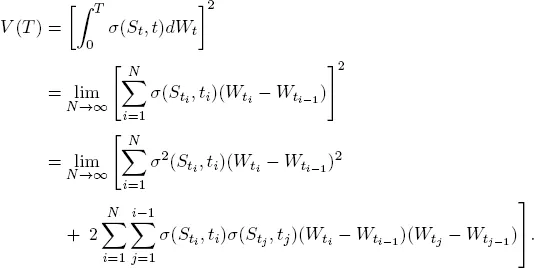

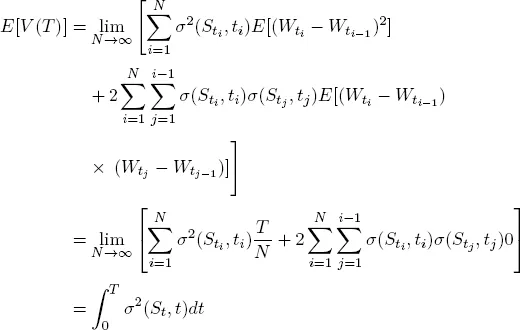

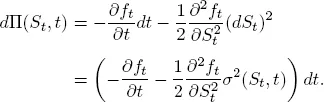

Consider a function f(St, t) of St and t. Ito’s Lemma gives

As in standard calculus, (

dt)

2 =

dtdWt = 0. But in contrast,

= dt.To see this, consider (for

):

Then the expectation is given by

since

Further, it can be shown1 that

Thus, the stronger condition

holds in a mean square convergence sense.

1See Neftci in [Nef96].

1.1.2 The Black–Scholes Partial Differential Equation (PDE)

Given our discussion earlier, if we can come up with a self-financing and predictable trading strategy that attains a particular payoff, then that trading strategy gives the price of that payoff. We would like to replicate a derivative with value given by f (St, t) above where

Our trading strategy involves holding Δ(St, t) units of the underlying St at time t, and financing by borrowing or lending at the risk-free rate rt.2

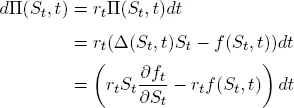

A portfolio of the derivative and our replicating strategy is worth

For it to be self-financing, we require

Now, if we choose

notice that

Since our portfolio only involves dt terms and not dWt terms, it is risk-free and hence must grow at the risk-free rate rt. This gives

2This is predictable and hence a valid strategy in a sense that ...