![]()

Chapter 1

Environmental Finance Introductory Remarks

October 1999

We are delighted to introduce the first of a monthly series of articles by Richard Sandor exploring the growing use of capital markets products to solve environmental problems. Few people are better placed to comment on this important trend. Best known as “the Father of Financial Futures” for his pioneering work on interest rate futures contracts, Dr. Sandor is currently chairman and chief executive of Environmental Financial Products, a Chicago-based company which designs novel risk management tools for the environmental, financial, and commodity markets. He is also a senior advisor to PricewaterhouseCoopers on greenhouse gas emissions trading; an expert advisor to the United Nations Conference on Trade and Development on tradeable permits for greenhouse gases; a director of Zurich-based investment and risk management company Sustainable Performance Group; a principal of SAM Sustainability Group and a member of the board of Dow Jones Sustainability Group Indexes GmbH. During several years’ work with the Chicago Board of Trade, he was instrumental in developing the exchange’s annual auction of sulfur dioxide allowances and its options and futures contracts for catastrophe insurance.

![]()

Chapter 2

The Convergence of Environmental and Capital Markets

October 1999

Two facets of the convergence of environmental and capital markets became visible in September 1999 as final preparations were being made for the Conference of Parties (COP) 5 climate change meetings in Bonn.

The early news from the markets is good. The cost of reducing greenhouse gases is less than early forecasts and corporations that are sustainable yield superior value to shareholders.

In London, British Petroleum reported on the success of its pilot program in greenhouse gas emissions trading and announced its plan to expand to group-wide emissions trading in January 2000.

In Zurich and Chicago, Dow Jones and the Sustainable Asset Management (SAM) Sustainability Group announced the launch of a family of comprehensive stock indexes — the Dow Jones Sustainability Group Index (DJSGI) — that track the share prices of the leading companies that have a proven record of being financially, socially, and environmentally sustainable. The selected companies represented in the new indexes demonstrate a real commitment to reducing pollution and safeguarding human and natural resources.

In 1998 British Petroleum — a component of DJSGI — announced that it would voluntarily reduce its greenhouse gas emissions to 10% below 1990 levels by the year 2010. It began a pilot emissions trading program to accomplish this objective in the most cost effective way. Twelve business units initially participated. The cost of reducing a ton of carbon emissions in early trades was approximately $63–$70 ($17–$20/ton CO2). Although the initial prices should be viewed cautiously, they are significantly below some early forecasts of $200/ton. Furthermore, the expansion to group wide emissions trading and the inclusion of credit-based trading (e.g., net emission reductions associated with external investments in energy efficiency and carbon sequestration) should witness a further reduction in costs associated with meeting the corporate targets. It is important to emphasize that British Petroleum extended its commitment when it acquired two US companies, Amoco and Arco.

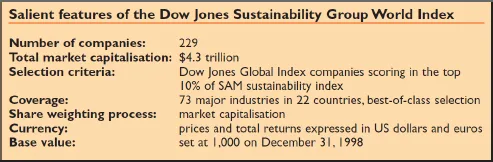

The comprehensive sustainable stock index family includes an index with global coverage, the DJSGI World, as well as regional indexes focused on companies in Europe, North America, Asia-Pacific, and a country index — DJSGI USA.

The table shows salient features of the global DJSGI index.

The DJSGI index is fully integrated with the Dow Jones Global Index in the sense that it uses the same calculation, publication, and review methodologies. Sustainability ratings for individual companies are based on general sustainability criteria, industry sustainability, and corporate sustainability criteria. In addition to public information a proprietary corporate sustainability questionnaire is used.

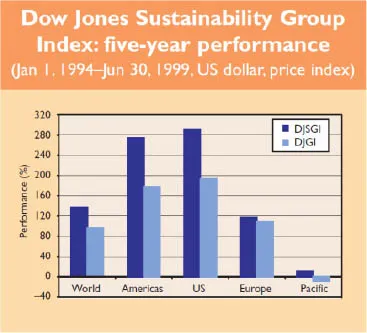

The results of back casting the price appreciation performance of the indexes are very instructive. As shown in the chart, in all instances the sustainable indexes outperformed the standard Dow Jones index. Furthermore, these superior returns were realized with minimal increases in volatility (risk) relative to comparable indexes. Evidence from the markets shows that sustainability and maximization of shareholder value are entirely compatible.

Both these examples of the convergence of the environmental and financial markets provide interesting price signals. The cost of reducing greenhouse gas emissions appears to be lower than many predicted and corporations that cut pollution and manage for sustainability will increase value to their shareholders.

Special thanks to Dr. Alois Flatz, Dr. Michael Walsh, and Rafael Marques for their valuable input.

![]()

Chapter 3

Voluntary Carbon Deals Break Records

November 1999

Since the 1997 Kyoto Protocol to the Rio Climate Convention, Washington legislators have spoken about global warming and its policy cousin emissions trading — like old soldiers vaguely remembering a defeated enemy in a long-passed military conflict.

However, this month in the capital markets and in a few cities in North America, the dialogue has become vivid and more animated, with the completion of two of the largest greenhouse gas emission trades in history.

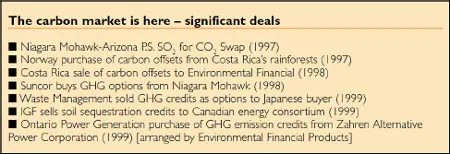

Currently, there is no central market for greenhouse gas emissions, and historical trades have not disclosed all of the transaction details.1 It appears that since the 1992 Rio Earth Summit, there have been almost 20 trades involving over 10 million tons of carbon dioxide (CO2)-equivalent emission reductions. It should be noted that many of these transactions involved options for future purchase of reductions rather than a full-fledged spot or future sale.

The transaction volume in November 1999 reached a total of more than 5 million tons of CO2 equivalent reductions, equal to the emissions of 1 million cars for 1 year. This volume of trading is small relative to the capital markets and is based on voluntary commitments. Nonetheless, these two transactions are sending a strong signal that the private sector is building the required infrastructure for full-blown markets. An examination of one of the transactions can help demystify the mechanics of an environmental derivatives trade as well as the motivations of the participants.

On 26 October 1999, the Wall Street Journal reported that Ontario Power Generation had purchased emissions reductions of 2.5 million tons of CO2-equivalent from Zahren Alternative Power Corporation (ZAPCO), a developer of landfill methane collection systems. The reductions were, or will be, generated in the years 1998, 1999, and 2000.

The trade is significant for several reasons:

•It is the largest spot greenhouse gas emissions trade in history.

•The participants are a Canadian buyer and a US seller, thereby making it international.

•The reductions have and will be registered by the US Department of Energy under the Energy Policy Act of 1992 and will also be recorded by the Canadian government under its Pilot Emission Reduction Trading Program.

•The emission reductions will be monitored twice — by ZAPCO and by the buyer of the methane gas — and independently attested to by PricewaterhouseCoopers.

•The reductions achieved were carefully selected to ensure that they are surplus to any regulatory requirements in the United States and that the transfer is legally incontestable.

Ontario Power Generation has set a voluntary, corporate target of stabilizing its greenhouse gas emissions at 1990 levels of 26 million tons of CO2-equivalent from the year 2000 forward. The company’s goal is to expand into new electricity markets while operating in a safe, open, and environmentally responsible manner. It is also committed to meeting environmental goals at the lowest cost to its customers.

Ontario Power’s greenhouse gas emissions reduction pledge will be achieved through a portfolio of activities. Internal energy efficiency measures will produce a significant amount of the reductions. Alternatively, some portion of the reductions can be achieved by purchasing offsets (reductions achieved by others), where this is financially desirable and serves the purpose of stimulating this new market.

After a considerable search, ZAPCO was identified as a natural counterparty. The company’s principal business is to drill wells in solid waste landfills, extract methane, and sell the methane for energy use, primarily to generate electricity. Methane is a natural byproduct of landfill waste. As a greenhouse gas, it is also chemically 21 times more potent than CO2 in contributing to global warming. If not collected from the landfill and destroyed (burned), it will seep into the atmosphere. In this particular example, without ZAPCO’s intervention, 2.5 million tons of CO2-equivalent would have seeped into the atmosphere. This would have had the same impact on global warming as 500,000 cars operating for a year.

ZAPCO’s incentive for trading is easy to understand. The sale of the emissions reductions provides a new revenue stream for its production of sustainable energy. As a result, its “return on investment” increases. ZAPCO can expand its operations, thereby cleaning additional landfills.

This trade also provides additional resources to monitor, verify, and independently attest to emissions reductions. Through these processes, we will take another critical step in the development of environmental derivatives. Defining and accurately measuring emissions reductions are prerequisites for creating a “homogenous” commodity and an effective trading system. Product standardization is essential for all of us to fully realize the gains from market-based solutions to environmental problems.

I would like to thank Dr. Michael Walsh, Alice LeBlanc, and Rafael Marques for their assistance in the preparation of this article.