![]()

CHAPTER 1

Risk Management for Trade Credit Financing Instruments

Introduction

The risk mitigation of trade credits reflects the implementation of the credit risk management system by ensuring the convergence between the underlying risk exposure and the capital planning of the financiers. Given equal trade credits, exposure to credit risk depends on the legal characteristics of the transaction and the services offered, while risk mitigation depends on the credit risk embedded in the assets. Therefore, alternatives to the implementation of an internal rating system distinguish between exposures based on purchased and/or assigned trade receivables (see An Internal Rating System for Exposures Based on Purchased/Assigned Trade Receivables section) and exposures backed by trade receivables (see An Internal Rating System for Exposures Backed by Trade Receivables section). Once the conceptual framework for the implementation of the internal rating system is defined (see An Internal Rating System for Trade Credit Financing Instruments section), the specific characteristics of the lending activity require adaptations in the application of the standard credit risk measurement parameters at both the individual level (see Credit Risk Parameters: Theoretical Features and Empirical Evidence section) and portfolio level (see Concentration Risk: Alternative Approaches and Empirical Evidence section). Concluding remarks are presented in Conclusions section.

Trade Credit Financing and Credit Risk Exposure

The potential loss that a financier can incur in lending to a defaulted debtor is determined by the exposure to credit risk. Therefore, credit risk models must provide consistent estimations (Crouhy, Galai, and Mark 2000). Exposure to credit risk depends on the types of products (Araten and Jacobs 2001), and predictability is strictly affected by the relevance of the undrawn amount of the commitment (Asarnow and Marker 1995).

In trade credit financing, the origination of the exposure to credit risk must be carefully evaluated in light of the combination of the services offered to counterparties (Table 1.1). In transactions with recourse to the seller/assignor, trade credit financing determines an exposure to credit risk due to the on-balance sheet exposure deriving from the amount of the advance provided to the seller/assignor or the total price paid for purchasing the receivables. In the absence of disbursement by the financier, any exposure to credit risk is outlined. Regarding transactions without recourse, the exposure to credit risk originates from the outstanding amount of trade credits assigned/purchased, regardless of any cash exposure stemming from the provision of an advance or payment of the purchasing price. The financier has made a commitment to guarantee the seller/assignor for the default of trade debtors. Therefore, even though only part of the commitment has already been provided, the residual part of the receivables assigned/purchased will be due according to the agreed terms and conditions. Therefore, in light of multiple sources affecting credit risk, cash exposure is relevant only to measure credit exposure due to dilution risk.

Table 1.1 Trade credit financing services and the exposure to credit risk

| With on-balance sheet exposure | Without on-balance sheet exposure |

With recourse | Credit risk determined by the advance/purchasing price | No credit risk |

Without recourse | Credit risk determined by the commitment to guarantee for trade debtors default | Credit risk determined by the commitment to guarantee for trade debtors default |

Source: Author’s elaborations.

The classification of exposures to credit risk in combination with services offered presented in Table 1.1 must be considered from a dynamic perspective. Because trade credit financing has a revolving nature, transactions that do not currently involve exposures to credit risk can become risky because of approbation in credit limits deliberated by the financier.

An Internal Rating System for Trade Credit Financing Instruments

Modern credit risk management is based on the development of credit risk models encompassing all policies, procedures, and practices used by a financial intermediary in estimating a credit portfolio’s probability density function (Basel Committee on Banking Supervision 1999). Estimation of the probability density function of potential losses requires the implementation of an internal rating system that comprises all the methods, processes, controls, and data collection and information technology systems that support the assessment of credit risk through the assignment of internal risk ratings and the quantification of default and losses estimates (Basel Committee on Banking Supervision 2004).

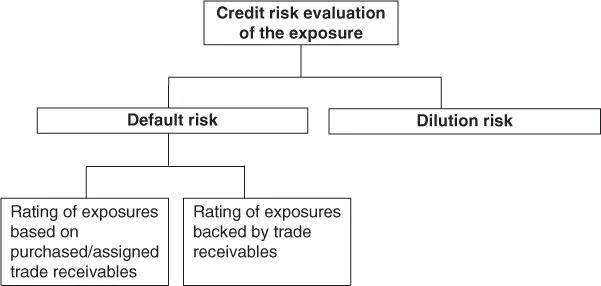

Even though a flourishing academic and professional literature on internal rating systems has emerged, their implementation for trade credit financing exposure still has issues to be resolved due to the specific characteristics of the lending activity. In particular, because risk management is intended to ensure the integrated control of risks to allocate capital efficiently (Saita 1999) and the ratings to be assumed as risk proxies must produce a reliable evaluation (Nocco and Stulz 2006) of the potential losses for each exposure, internal rating systems are found that refer to both the borrower and the facility (Foglia, Iannotti, and Marullo Reedtz 2001). Since trade credit financing exposures are involved, the alignment between risk measures and underlying risks requires the development of a facility-oriented internal rating system. Because of the self-liquidating nature of the exposure, the rating assignment must evaluate the risk of the relationship between the supplier and the customer consistently with the risk taken on by the financier (Figure 1.1).

Figure 1.1 Credit risk evaluation of trade credit financing exposures

Source: Author’s elaboration.

In light of the multiple sources that can determine credit losses in trade credit financing, the internal rating system must obtain a credit rating for the exposure based on the synthesis of

- •Default risk

- •Dilution risk

The implementation of the default risk rating for trade credit financing is based on management activity. The management of receivables provides the lender information unavailable in transactions where receivables back the loans provided to the seller/...