How much money is circulating in the United Kingdom? The question sounds simple. In fact, it is notoriously difficult to answer, because what counts as money is not a straightforward matter. A variety of measures have been advanced, and they tell different stories about the changing supply of money in an economy. These differences are of more than merely academic interest, because measures of the money supply are inputs to the decisions of central banks. Wrong answers can lead to wrong actions, with potentially devastating economic effects. This book examines the measure of money and, in that light, the actions of the Bank of England in in the lead up to the 2008 financial crisis and its aftermath. It is essential reading for anyone interested in money, measures of its quantity, and the relationship between the money supply and the economic cycle.

eBook - ePub

Getting the Measure of Money

A Critical Assessment of UK Monetary Indicators

- 206 pages

- English

- ePUB (mobile friendly)

- Available on iOS & Android

eBook - ePub

About this book

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Study more efficiently using our study tools.

Information

Edition

1Subtopic

Monetary Policy2M: The importance of alternative monetary aggregates

Summary of key points

- For some time academic economists have neglected the role of money, and monetary policy has been conducted through interest rates rather than the money supply.

- The introduction of quantitative easing (QE) in 2009 has made the money supply relevant again, and made a discussion about alternative money supply measures of direct policy significance. Unfortunately, official Bank of England figures have proved misleading and subject to major alterations (such as the replacement of M4 with M4ex).

- This chapter argues in favour of measures such as MZM and Divisia money, which attempt to find a middle ground between narrow and broad, and introduces a new and publicly available measure, MA, based on an a priori approach to defining money as the generally accepted medium of exchange.

- Attention to MA would have provided an early warning that a major credit crunch was occurring in 2008, and explains the lethargic recovery.

Introduction

The conventional explanation for the cause of the Great Depression was an unprecedented contraction of the money supply (Friedman and Schwartz 1963b; Romer 1992). So when, in 2008, many of us were concerned that the recent housing boom would precede an imminent credit crunch, monetary aggregates seemed an obvious place to look for warning signs. And yet M4 (the conventional measure of broad money for the UK) was growing strongly. The growth rate increased from around 9 per cent in 2004 to 14 per cent by 2007. And then, in late 2008, it went above 17 per cent. At the time, I was working on compiling an alternative measure of the money supply, and my measure showed a dramatic contraction. Something seemed amiss.

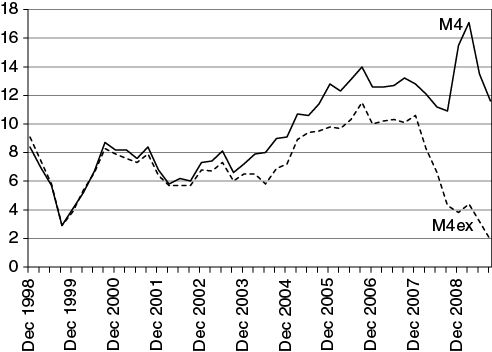

In September 2007 the Bank of England had begun a user consultation to modify M4, proposing to exclude intermediate ‘other financial corporations’ (OFCs) because it views them as containing interbank transfers.5 This was timely because QE boosted the money holdings of intermediate OFCs, but it was only in May 2009 that the Bank released quarterly estimates of M4 that excluded those intermediate OFCs (see Janssen 2009). In stark contrast to the existing M4, M4ex now showed a dramatic fall in broad money from mid 2008 (see Figure 1).6 As David B. Smith (2010: 2) said, ‘unfortunately for the Bank of England, the renewed emphasis on broad money occurred when its established M4 definition had become distorted by artificial transactions designed to push bank liabilities off balance sheet’.

Figure 1M4 and M4ex, 1998–2009 (year-on-year % change)

This timing had a major impact on policy decisions. At the height of the financial crisis, in September 2008, there was an almost divergent relationship between the traditional measure of broad money (M4) and a new measure of broad money (M4ex) that the Bank was attempting to launch. Even the Governor of the Bank of England seemed confused. In 2011 Mervyn King advocated QE2 on the grounds that the money supply was falling. But while this was true for M4 (which fell by 0.6 per cent relative to the previous year), M4ex had increased by 2.2 per cent (Ward 2011). He was looking at the wrong measure of broad money.

Other events compounded the lack of data. In September 2008 the Bank was concerned that confidentiality issues would emerge following the inclusion of the recently nationalised Northern Rock in the ONS Public Sector Finance Statistics (PSF). To prevent market watchers from arbitraging information between different data sources, a specific table (A3.2) was discontinued. It was reinstated in June 2009, because by then other banks had been brought into the public sector. But for several critical months we lost information. Similarly, in the US, William Barnett (2012: 27) has pointed out that the Federal Reserve not only stopped reporting M3 in March 2006, but also stopped releasing the component series. When the Bank of England began paying interest on reserves in May 2006, it switched from M0 to ‘Notes and Coin’ as its favoured measure of the narrow money supply. There may well be valid reasons for such changes, but the timing was unfortunate. It was like a boat heading into stormy waters while experimenting with new navigational equipment.

The global financial crisis has had a profound and enduring impact on the way monetary policy has been conducted. In March 2009, the Bank of England reduced the Bank rate to 0.5 per cent, which has been seen as a lower bound for policy, limiting the scope for further cuts. In conjunction with this decision it was announced that £75 billion worth of quantitative easing (QE) would be launched, intending to inject money directly into the economy through the purchase of various financial assets with newly created reserves.7 In addition to demonstrating a change in focus from short-term to longer-term interest rates, QE has also increased the attention paid to the role of monetary aggregates. As the then Governor, Mervyn King, explicitly revealed, ‘We are now doing [this] in order to increase the supply of broad money in the economy’.8 Despite theoretical and empirical doubts about the ability to define and measure the money supply, it is of direct and increasing policy significance.

This is in stark contrast to previous trends that have downplayed attention to the money supply. The US Federal Reserve stopped targeting M1 in 1987 and M2 in 1992. Financial deregulation that occurred during this period was seen to create greater instability in the demand for money, and thus reduce the influence of the money supply on prices and output. Indeed ‘the reliability of various money measures as useful indicators on which to base policy has become se...

Table of contents

- The author

- Preface

- Acknowledgements

- Summary

- 1Introduction

- 2M: The importance of alternative monetary aggregates

- 3V: Velocity shocks, regime uncertainty and the central bank

- 4P: The hidden inflation of the Great Moderation

- 5Y: GDP, GO and the structure of production

- 6Conclusion

- About the IEA

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

- Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

- Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go.

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Getting the Measure of Money by Anthony J. Evans in PDF and/or ePUB format. We have over 1.5 million books available in our catalogue for you to explore.