Recent megatrends such as increasing complexity, volatility, internationalization and increased demand for transparency and compliance have changed the expectations towards the controlling function. During his professional experience, the author observed the increased expectations towards the controlling function. If controlling is to maintain its influence in a company, it needs to adapt to the changes in management expectations. To outline "how to increase the value added by the controlling function in multinational production companies", four research questions were addressed and answered. The questions which were answered were "what does controlling involve and which factors influence the set-up of the controlling function in a company", "how are the expectations towards the controlling function changing over time and what is its value contribution", "how can the controlling function add value to standard reporting and budgeting activities" and "how can the controlling function add value to reorganization activities".

eBook - ePub

How to Increase the Value-added of Controlling

A Guide to an Efficient and Sustainable Management Support

- 215 pages

- English

- ePUB (mobile friendly)

- Available on iOS & Android

eBook - ePub

How to Increase the Value-added of Controlling

A Guide to an Efficient and Sustainable Management Support

About this book

Information

1 Introduction

Very little is needed to make a happy life;

it is all within yourself, in your way of thinking.

Marcus Aurelius (121–180 AD)

Recent megatrends such as increasing complexity, volatility, internationalization and increased demand for transparency and compliance have changed the expectation towards the controlling function. Recent surveys have indicated that the need for a controller with a data analyst role is decreasing due to modern ERP solutions (Brands and Holtzblatt, 2015; Button 2015). Complementarily, the request towards the controlling function to provide specific decision support as a business partner of the management are increasing (Gräf 2014; Schäffer and Weber 2014a).

The idea and urgency for this topic became obvious to the author during various milestones of professional experience in multinational production companies, which have a typical number of maintained controlling specializations and a strategic orientation in the controlling function. During this professional experience, the increased expectations toward the controlling function became obvious, especially from the following perspectives:

While working in the corporate controlling department of a major steel company in Germany, the author observed that the management reporting was mainly finance driven and allowed the company no reasonable basis for an operational root cause analysis. Without knowledge about the root causes, there was no basis to set up specific countermeasures to fix the problem. So, instead of fixing the problem, the controlling department spent a lot of energy to analyse and maintain a complicated system of financial KPI including Free Cash Flow bridges between budgets and to forecast as well Economic Value-Added scenarios. It became obvious that such analysis took a lot of time to prepare and to explain to the executive board but creating no significant insight into the business. In consequence, the executive board decided to ignore the financial analysis. These observations inspired to further research on how to optimize the “value-added of management reporting” presented inchapter four.

As a general manager of automotive companies in Germany, China and Eastern Europe, the author was deeply involved in corporate planning processes and observed that those companies spent almost half a year in preparing the budget. In the first phase, the planning was prepared bottom-up in the expectation that the corporate headquarter would induce budget rounds for cost-cutting. After that, it often took half a dozen negotiation rounds and budget presentations until the final budget was approved. But, despite spending so much time and energy on the budget, it had only a little connection either with corporate strategy or with the relevant operational KPI. Furthermore, the budget was too inflexible to be changed in case a macroeconomic shock leaving the company “to be driven by sight”. This observation was triggering the author’s research to improve corporate planning and to develop a model on “operative planning by objectives”, described in chapter five.

During that time the author was also involved in strategic planning processes and responsible for public relations. It thereby surprised that those two disciplines were not connected with each other. While companies see the need to include some charity in their public relation, they seldom see a way to connect their social contribution with their strategic goals. Strategic planning does consider external trends but is seldom aware of the aspect that big companies have the possibility to influence and change the society and the business environment in which they operate. During the four years of working in Eastern Europe, the author took an active role in several corporate social responsibility (CSR) initiatives. The supported initiatives included the (re)introduction of vocational education adding and modernizing bachelor and master curriculums at leading universities in Eastern Europe. Based on the experience and insights made participating in these initiatives, the author researched and connected the strategic planning and CSR aspects in a model referred later as the “value diamond of CSR” in chapter five.

Being a corporate restructuring manager in an automotive group, the author noticed that the reaction of corporates to crisis is seldom structured in a systematic way. The research on the enhancement of organization with a “portfolio-based restructuring model” proposed in chapter six is a consequence of these observations.

The publication reflects the observations of the author described above and aims at contributing new insights on how to improve the controlling function in modern multinational production companies. The following research questions will facilitate this aim:

The first research question “What does controlling involve and how can it add value to the company?” will span the field of research by clarifying what controlling means and to determine how the added value can be defined. The answer to this question will clarify a new perspective on the modern understanding of the controlling function and its development. From the results of multiple surveys that have been analysed, it becomes clear that the controlling function, in general, has been increasingly progressing, from a data preparation to a business and to a change management oriented function, highly interconnected with the management of a business organization. The answer to this first research question will be given in chapter two and three.

The second research question: “Which factors influence the set-up of the controlling function in a company and how are the expectations towards the controlling function changing over time?” will depict how the requirements towards the controlling function are changing. An analysis will present how the expectation gap can entrap the controlling function due to misalignment with the management needs. To close this gap, change models will be discussed and a new change model will be developed. The answer to the second research question will be given inchapter three.

The third research question, “How can the controlling function add value to standard reporting and budgeting activities?” will analyse and illustrate how the controlling function could increase the added-value of its standard activities such as management reporting and operative planning. The publication will outline improvements of standard management reporting activities by focusing on decision usefulness. By taking this approach, the decision-making process becomes more cost-effective. The improvements suggested are based on a survey conducted by the author across companies in 2014; the results are benchmarked with a comparable cross-European survey. A real-life implementation in a multinational production company shall validate the best practices described by using action research methods. In the content of the publication, the optimization of the standard budgeting processes will be outlined using a strategy-orientated planning model. The answer to the third research question will be given in chapter four and five.

The fourth research question “How can the controlling function add value to reorganization activities?” will focus on how to use the saved capacity by more efficient and effective standard processes for better management support. Fewer costs for standardized processes can release the capacity for management support aspect of controlling that will have a positive effect on EBIT. Emphasis is placed on research that demonstrates how to improve the alignment between the business strategy and the strategic planning process. In the case study project, the aim is to show the use of the methodology of strategic planning in managing successful CSR projects, thereby improving the financial performance of a multinational production company. The value increased of the controlling function as a provider of management support will be demonstrated by applying its methodology to business-oriented reorganization activities. Furthermore, a portfolio-based model to improve the success of restructuring initiatives will be developed. In closing, a conclusion to the research will summarize the main contributions of this publication as well as provide an outlook for further research. The answer to the fourth research question will be given in chapter six and seven.

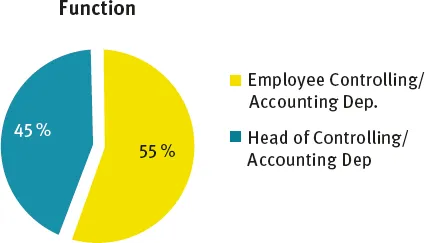

Surveys: To back up and enrich the theoretical research and the authors’ own observations during business, the author performed two surveys, one made in the year of 2014 and one made in the year of 2016. The first survey “2014 survey” was conducted during December 2014 with 20 finance experts from a global manufacturing company at its seven plants in Eastern Europe as well as in the global headquarters. 45 % of the experts interviewed were in management level positions (see Figure 1.1).

Source: Authorʼs 2014 processing/survey.

To better interpret and analyse the 2014 survey, the results were benchmarked with a reference survey (“reference”) conducted by Deloitte Consulting between December 2012 and January 2013. The reference included the same set of questions which consisted out of 30 questions. The reference included 143 participants across different branches, company size...

Table of contents

- Cover

- Title Page

- Copyright

- Dedication

- Foreword

- Contents

- List of Figures

- List of Tables

- List of Abbreviations

- 1 Introduction

- 2 Value creation in controlling – definition and terminology

- 3 Changing expectations in multinational production companies

- 4 Management reporting – contents and processes

- 5 Operative planning by objectives

- 6 Strategic planning of multi-stakeholder initiatives

- 7 Enhancement of organization with portfolio-based restructuring

- 8 Conclusions, contributions and outlook

- Bibliography

- Index

- About the Author

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Study more efficiently using our study tools.

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

- Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

- Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go.

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access How to Increase the Value-added of Controlling by Valerian Laval in PDF and/or ePUB format, as well as other popular books in Business & Accounting. We have over 1.5 million books available in our catalogue for you to explore.