Written by two of the most distinguished finance scholars in the industry, this introductory textbook on derivatives and risk management is highly accessible in terms of the concepts as well as the mathematics.

With its economics perspective, this rewritten and streamlined second edition textbook, is closely connected to real markets, and:

Beginning at a level that is comfortable to lower division college students, the book gradually develops the content so that its lessons can be profitably used by business majors, arts, science, and engineering graduates as well as MBAs who would work in the finance industry.

Contents:

Introduction:

Derivatives and Risk Management

Interest Rates

Stocks

Forwards and Futures

Options

Arbitrage and Trading

Financial Engineering and Swaps

Forwards and Futures:

Forwards and Futures Markets

Futures Trading

Futures Regulations

The Cost-of-Carry Model

The Extended Cost-of-Carry Model

Futures Hedging

Options:

Options Markets and Trading

Option Trading Strategies

Option Relations

Single-Period Binomial Model

Multiperiod Binomial Model

The Black–Scholes–Merton Model

Using the Black–Scholes–Merton Model

Interest Rate Derivatives:

Yields and Forward Rates

Interest Rate Swaps

Single-Period Binomial HJM Model

Multiperiod Binomial HJM Model

The HJM Libor Model

Risk Management Models

Readership: Undergraduate and graduate students of economics, business, arts, science and engineering, and MBAs who would work in the finance industry.Derivatives;Financial Markets;Risk Management;Arbitrage;Financial Engineering;Forwards;Futures;Call Options;Put Options;European Options;American Options;Swaps;Currency Swaps;Interest Rate Swaps;Commodity Swaps;Equity Swaps;Credit Default Swaps;Commodity Derivatives;Equity Derivatives;Index Derivatives;Interest Rate Derivatives;Commodities;Margins and Daily Settlements;Binomial Model;Black-Scholes Model;Black-Scholes-Merton Model;Delta Hedging;Gamma Hedging;Heath-Jarrow-Morton Model;Libor Model,;Forward Rate Agreements;Interest Rate Futures;Interest Rate Options;Market Manipulation;Regulation;Derivatives Exchanges00

EXTENSION 1.1 The Influence of Regulations, Taxes, and Transaction Costs on Financial Innovation

Diverse Views on Derivatives

Applications and Uses of Derivatives

A Quest for Better Models

1.4Defining, Measuring, and Managing Risk

1.5The Regulator’s Classification of Risk

1.6Portfolio Risk Management

1.7Corporate Financial Risk Management

Risks That Businesses Face

Nonhedged Risks

Risk Management in a Blue Chip Company

1.8Risk Management Perspectives in This Book

1.9Summary

1.10Cases

1.11Questions and Problems

1.1 Introduction

The bursting of the housing price bubble, the credit crisis of 2007, the resulting losses of hundreds of billions of dollars on credit derivatives, and the failure of prominent financial institutions have forever changed the way the world views derivatives. Today derivatives are of interest not only to Wall Street but also to Main Street. Derivatives are cursed as one of the causes of the Great Recession of 2007–2009, a period of decreased economic output and high unemployment.

But what are derivatives? A derivative security or a derivative is a financial contract that derives its value from an underlying asset’s price, such as a stock or a commodity, or even from an underlying financial index like an interest rate. A derivative can both reduce risk, by providing insurance (which, in financial parlance, is referred to as hedging), and magnify risk, by speculating on future events. Derivatives provide unique and different ways of investing and managing wealth that ordinary securities do not.

Derivatives have a long and checkered past. In the 1960s, only a handful of individuals studied derivatives. No academic books covered the topic, and no college or university courses were available. Derivatives markets were small, located mostly in the US and Western Europe. Derivative users included only a limited number of traders in futures markets and on Wall Street. The options market existed as trading between professional traders (called the over-the-counter [OTC] market) with little activity. In addition, cheating charges often gave the options market disrepute. Derivatives discussion did not add sparkle to cocktail conversations, nor did it generate the allegations and condemnations that it does today. Brash young derivatives traders who drive exotic cars and move millions of dollars with the touch of a computer key didn’t exist. Although Einstein had developed the theory of relativity and astronauts had landed on the moon, no one knew how to price an option. That’s because in the 1960s, nobody cared, and derivatives were unimportant.

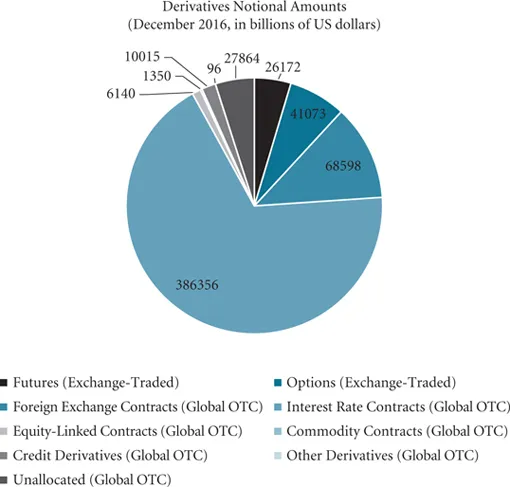

What a difference the following decades have made! Beginning in the early 1970s, derivatives have undergone explosive growth in the types of contracts traded and in their importance to the financial and real economy. According to the Bank for International Settlements (known as the BIS), the markets are now global and measured in trillions of dollars. Indeed, as depicted in Figure 1.1, in December 2016 the total outstanding US dollar notional value for exchange-traded derivatives was (26,172 + 41,072 =) 67,245 billion and for OTC derivatives a staggering 500,419 billion. Hundreds of academics study derivatives, and thousands of articles have been written on the topic of pricing derivatives. Colleges and universities now offer numerous derivatives courses using textbooks written on the subject. Derivatives experts are in great demand. In fact, Wall Street firms hire PhDs in mathematics, engineering, and the natural sciences to understand derivatives—these folks are admirably called “rocket scientists” (“quants” is another name). If you understand derivatives, then you know cool stuff; you are hot and possibly dangerous. Today understanding derivatives is an integral part of the knowledge needed in the risk management of financial institutions.

FIGURE 1.1:Global Derivatives Market

Source:https://www.bis.org/statistics/extderiv.htm, Table D1: Exchange-traded futures and options, by location of exchange; and https://www.bis.org/statistics/derstats.htm, Table D5: Global OTC derivatives market.

Markets have changed to accommodate derivatives trading in three related ways: the introduction of new contracts and new exchanges, the consolidation and linking of exchanges, and the introduction of computer technology. Sometimes these changes happened with astounding quickness. For example, when twelve European nations replaced their currencies with the euro in 2002, financial markets for euro-denominated interest rate derivatives sprang up almost overnight, and in some cases, they quickly overtook the dollar-denominated market for similar interest rate derivatives.

This chapter tells the fascinating story of this expansion in derivatives trading and the controversy surrounding its growth. An understanding of the meaning of financial risk is essential in fully understanding this story. Hence a discussion of financial risk comes next, from the regulator’s, the portfolio manager’s, and the corporate financial manager’s points of view. We explain each of these unique perspectives, using them throughout the book to increase our understanding of the uses and abuses of derivatives. A summary completes the chapter.

1.2 Financial Innovation

Derivatives are at the core of financial innovation, for better or for worse. They are the innovations to which columnist David Wessel’s Wall Street Journal article titled “A Source of Our Bubble Trouble,” dated January 17, 2008, alludes:

Modern finance is, truly, as powerful and innovative as modern science. More people own homes—many of them still making their mortgage payments—because mortgages were turned into securities sold around the globe. More workers enjoy stable jobs because finance shields their employers from the ups and downs of commodity prices. More genius inventors see dreams realized because of venture capital. More consumers get better, cheaper insurance or fatter retirement checks because of Wall Street wizardry.

Expressed at a time when most of the world was in the Great Recession, this view is challenged by those who blame derivatives for the crisis. Indeed, this article goes on to say that “tens of billions of dollars of losses in new-fangled investments [in derivatives and other complex securities] at the largest US financial institutions—and the belated realization that some of those Ph.D. wielding,...

Table of contents

Cover

Halftitle page

Title page

Copyright page

Dedication page

About the Authors

Brief Contents

Contents

Preface to Second Edition

Preface to First Edition

PART I: Introduction

PART II: Forwards and Futures

PART III: Options

PART IV: Interest Rate Derivatives

APPENDIX A Mathematics and Statistics

Glossary

References

Notation

Additional Sources and Websites

Books on Derivatives and Risk Management

Name-Index

Subject-Index

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Study more efficiently using our study tools.

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go. Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access An Introduction to Derivative Securities, Financial Markets, and Risk Management by Robert Jarrow, Arkadev Chatterjea in PDF and/or ePUB format, as well as other popular books in Business & Financial Engineering. We have over 1.5 million books available in our catalogue for you to explore.