![]()

Part One

Investment in the United Kingdom: The Current Outlook

1.1 THE UK ECONOMY AND INWARD INVESTMENT

Jonathan Reuvid, Legend Business

The outcome of the June 2016 Referendum on UK membership of the EU had little visible effect on the UK economy up to March 2017 when the Prime Minister invoked Section 50 of the Treaty of Rome confirming termination from March 2019. Following the intervention of the UK General Parliamentary Election called in April, negotiations on the terms of departure were delayed until 19th June when formal negotiations in Brussels opened. Understandably, uncertainties which surround the likely outcomes and which will persist until there is an outline agreement on the future relationship between the EU and the UK are now having a dampening effect on the economy.

However, the economy remains robust and there are encouraging signs of possible bilateral trade deals with some leading global economies beyond the EU when Brexit finally takes place. (Profiles of these economies and their foreign trade are included in Appendix I of this book.) The UK Department for International Trade is leading these initiatives.

MACRO-ECONOMIC INDICATORS

Forecasts for 2017/18

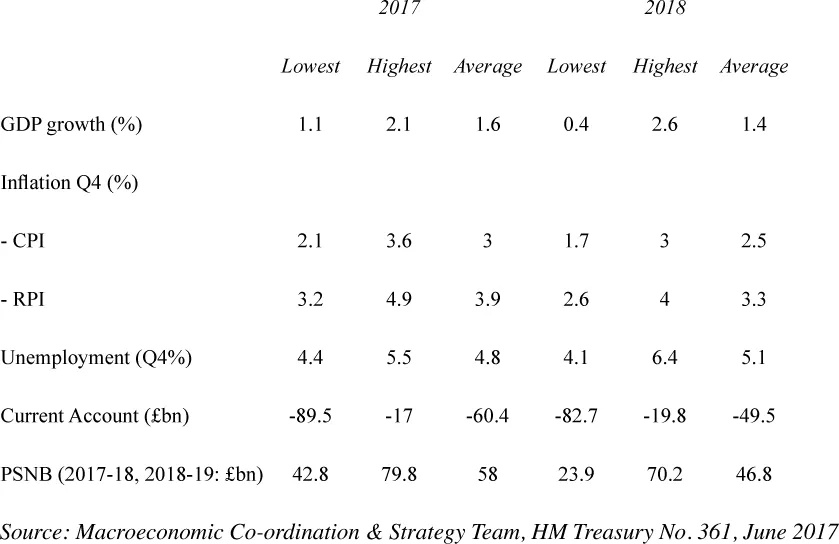

Composite forecasts for the basics of the UK economy published by HM Treasury are highlighted in Table 1.1.1.

Table 1.1.1 Macro-economic indicators June 2017

The highest and lowest forecasts are extracted and the averages calculated from the forecasts made by 20 City banks and accredited advisers and by 19 international institutes and professionals during the previous three months excluding May. The non-City institutions include the European Commission, OECD, IMF, the Economist Intelligence Unit (EIU), the Confederation of British Industry (CBI) and the British Chamber of Commerce (BCC).

Growth prospects for the UK are compared with those of other major advanced economies and the emerging and developing economies in Table 1.1.2 by reference to the most recent OECD forecasts of real GDP.

Table 1.1.2 Forecast GDP growth for 2017 and 2018 vs 2016

| 2016 | 2017 | 2018 |

| % | % | % |

Advanced economies | | | |

UK | 1.8 | 1.6 | 1.0 |

US | 1.6 | 2.1 | 2.4 |

Australia | 2.4 | 2.5 | 2.9 |

Canada | 1.4 | 2.8 | 2.3 |

France | 1.1 | 1.3 | 1.5 |

Germany | 1.8 | 2.0 | 2.0 |

Italy | 1.0 | 1.0 | 0.8 |

Japan | 1.0 | 1.4 | 1.0 |

Spain | 3.2 | 2.8 | 2.4 |

Euro Area | 1.7 | 1.8 | 1.8 |

Emerging and developing Asian economies | | | |

China | 6.7 | 6.6 | 6.4 |

India | 7.1 | 7.3 | 7.7 |

Korea | 2.8 | 2.6 | 2.8 |

Total OECD | 1.8 | 2.1 | 2.1 |

Source: OECD statistical Table 1, June 2017

The lower rate of growth projections by the OECD for the UK in 2018 compared to HM Treasury’s current forecasts reflects a more pessimistic view of the progress of Brexit negotiations. Nevertheless, it is clear that the short-term outlook for the UK economy is significantly weaker than for North America and for the larger EU countries other than Italy. All of these are overshadowed by the continuing high growth rates of Asia’s two biggest economies.

The UK Population

At mid-year 2016 the population total stood at 65.6 million having increased by 538,100 over the previous year. Of this increase net immigration accounted for 336,000, representing 62.4%.(Source: Office of National Statistics, June 2017).

As of May 2017, 32.1 million were in work, 324,000 more than a year earlier. As of July the jobless rate stands at 4.5% (www.tradingconomics.com). Applying the international measurement standard, the UK’s unemployment rate compares favourably with the EU average of 9.3% (source: Eurostat, 2017) although higher than the US (4.4%) and Germany (3.9%).

The last UK census of population was taken in 2011, when 83.9% of the population were resident in England, 8.4% in Scotland, 4.9% in Wales and 2.8% in Northern Ireland. Of those living in the UK at that time 8.4 million (13%) were born abroad.

UK INWARD INVESTMENT

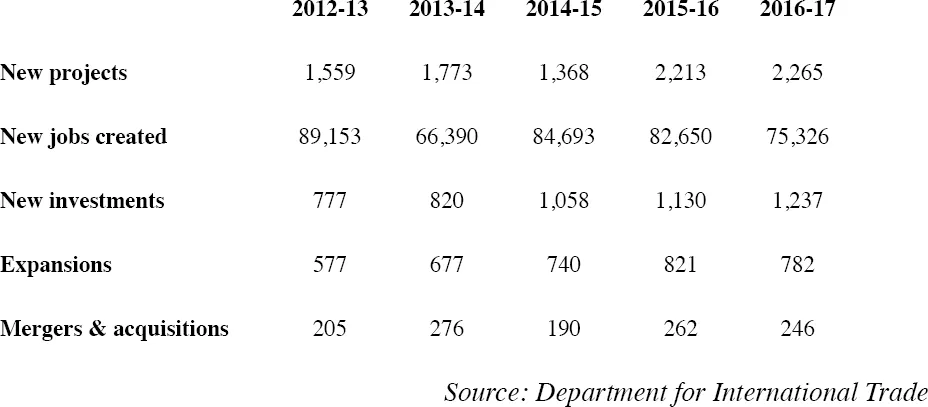

The UK enjoyed a successful year in 2016-17 with the number of projects rising by 2% compared with the previous year to 2,265, creating 75,226 new jobs and protecting a further 32,672 jobs. However, the total of jobs related to inward investment projects declined from 115,974 in 2015-16 to 107,986. Of the new projects registered 1,053 were funded by investors new to the UK and 1,212 by existing investors extending their UK engagements. Over the past five years, the number of new FDI projects in the UK has increased steadily each year as illustrated in Table 1.1.3.

Table 1.1.3 FDI performance over five years

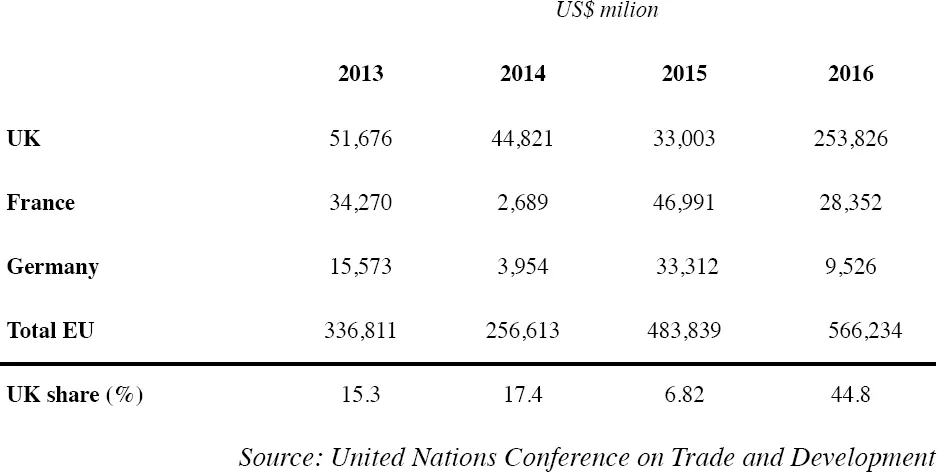

Inward investment flows to the UK over the past four years have been impressive by comparison with EU fellow members and the EU in total according to UNCTAD statistics (World Investment Report 2017).

Table 1.1.4 Value of FDI inflows

In terms of accumulated investment UK inward FDI in 2016 reached USD$1.2 trillion, representing 15.6% of the EU total and compared to US$771 billion for Germany and US$698 billion for France. UK outward FDI stocks, net of disposals, stood at US$1.4 trillion.

Sources of FDI

The top sources of UK FDI in 2016-17 in descending order are listed in Table 1.1.5 together with the new jobs created and safeguarded jobs.

Table 1.1.5 The UK’S major investment sources

Country | FDI projects | New jobs | Safeguarded jobs |

United States | 557 | 24,607 | 7,197 |

China and Hong Kong | 160 | 3,326 | 1,444 |

France | 131 | 5,831 | 2,182 |

India | 127 | 3,999 | 7,645 |

Australia and New Zealand | 127 | 2,197 | 1,803 |

Japan | 116 | 3,511 | 6,095 |

Germany | 100 | 5,802 | 426 |

Italy | 99 | 1,482 | 167 |

Canada | 72 | 1,788 | 122 |

Spain | 70 | 1,789 | 1,152 |

Ireland | 56 | 2,914 | 752 |

Netherlands | 53 | 2,292 | 546 |

Switzerland | 49 | 1,428 | 643 |

Other Europe, Middle East, Africa | 261 | 6,867 | 923 |

Other American countries | 59 | 1,080 | 206 |

Other Asian Pacific countries | 82 | 1,896 | 394 |

Source: Department for International Trade

Regional dispersion

FDI in 2016-17 was spread widely among the regions with the Greater London Area taking the lion’s share as Table 1.1.6 demonstrates:

Table 1.1.6 Regional dispersion of 2016-17 FDI

| No. of projects | New jobs created |

London | 891 | 20,753 |

South East | 217 | 5,432 |

North West | 147 | 6,501 |

West Midlands | 151 | 6,570 |

Yorkshire and the Humber | 132 | 3,872 |

East of England | 125 | 3,634 |

South West | 101 | 3,402 |

East Midlands | 74 | 1,796 |

North East | 69 | 4,609 |

England | 1,907 | 56.569 |

Scotland | 183 | 5,547 |

Wales | 85 | 2,581 |

Northern Ireland | 34 | 1,652 |

Source: Department for International Trade

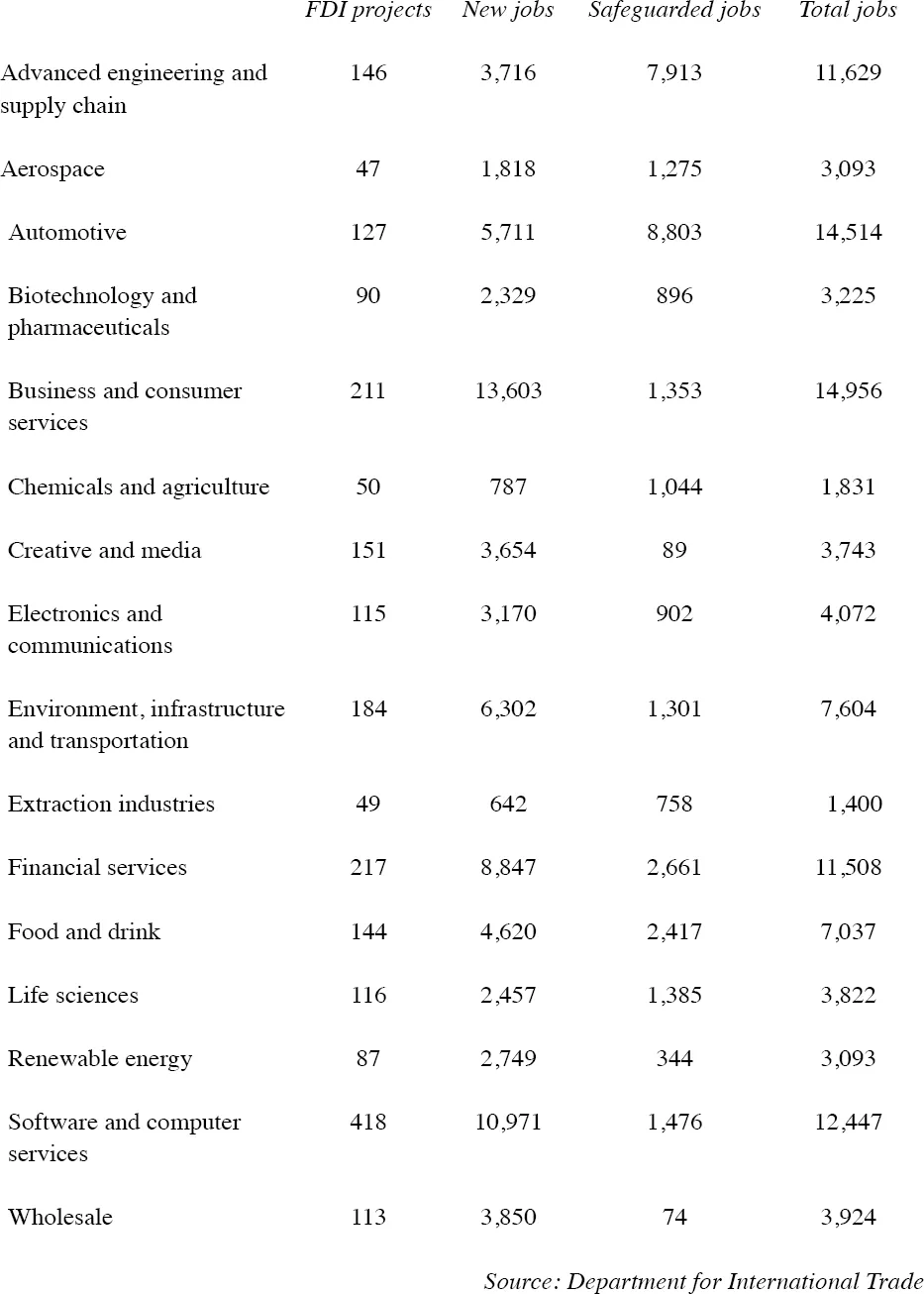

Sectoral focus of 2016-17 FDI

As the report issued by the Department for International Trade for 2016-17shows, the tech sector attracted the greatest number of new projects with the second highest number of new jobs after the business and consumer services sector. Many of these are located in the Greater London area and at the beginning of July London & Partners reported a record level of investments in UK tech companies in the first six months of 2017 accounting for £1.3 billion. The UK remains the leading destination for venture capital investments, attracting more than twice as much invested than in Berlin.

The sectoral dispersion of investment and job creation is illustrated in Table 1.1.7.

Table 1.1.7 Sector results 2016-17

Among the other sectors receiving the most new projects creating high numbers of jobs and protecting existing ...