Praise for LEARNING PRACTICAL FINTECH FROM SUCCESSFUL COMPANIES

"Throughout my career I've seen the world of finance transformed by technology, from the earliest days of online lending to the current innovations happening with blockchain and cryptocurrency. I believe we're at a critical point in history where a new Internet of Value is starting to emerge, and I'm excited to see so many talented entrepreneurs tackling problems in global finance today." —CHRIS LARSEN, Cofounder and Executive Chairman of Ripple

"Blockchain technology is changing the way the world does business. This book offers an inside look at how institutions from all corners of financial services and other areas of commerce are collaborating with software firms like R3 to re- engineer the infrastructure that enables money, goods, and information to flow around the globe." —DAVID RUTTER, Founder, Chief Executive Officer of R3

"When we think about FinTech, we often think about New York, Silicon Valley, and London, but this book tackles the awakening dragon that is Asian FinTech. Do yourself a huge favor and read this book. Asia is where the real FinTech evolution is happening." —BRETT KING, Author of Augmented and BANK 4.0, Host of the Breaking Banks Radio Show, Founder of Moven

Trusted by 375,005 students

Access to over 1 million titles for a fair monthly price.

CHAPTER 1 Internet Revolution and Evolution of FinTech

Paradigm Shift from FinTech 1.0

In 1999, some friends and I published a book called Challenges of E-Finance (Toyo Keizai Inc.). In the introduction, I wrote the following:

As Schumpeter’s words clearly indicate, the new markets, new organizational forms of industries and other products that the Internet gives birth to will probably result in a process of creative destruction that occurs on a global scale, and at a speed that humanity has never seen before. This process will occur first in the finance industry, because that industry is well suited for the Internet.

The various companies in our financial group hope to create a stir that shifts Japan’s distorted financial system to one that makes it possible to provide greater economic efficiency and convenience to investors and consumers of various financial services, by making use of the Internet’s massive destructive power and reforming that distorted financial system. As history has shown, the process of creative destruction does not necessarily have a negative impact on the national economy, but probably has a positive impact when looked at from the long term, and comprehensively. We firmly believe this, and will take on the challenge of transforming the existing financial industry.

Over the years, I have repeatedly and assertively espoused an Internet revolution of this nature, and have intently pressed forward with efforts to achieve its realization. I will discuss the results of these efforts later, but there is probably wide agreement that this process of creative destruction has progressed with the speed and force that I envisioned when I first wrote the quoted passage.

Advent of FinTech 1.0

Since its founding in 1999, the SBI Group has built the world’s first ecosystem for the Internet financial services industry, which includes services such as banking, securities, and insurance. I call this ecosystem FinTech 1.0. In Japan, the term FinTech started to be used frequently in 2015.

However, US focus had turned to FinTech about two or three years earlier, and it has gradually taken the spotlight. What many people mean by the term FinTech is not simply introducing online versions of traditional financial services. Instead, the term applies to the provision of new solutions for the full range of financial services. US-based PayPal Holdings Inc. (among others) took the lead in this movement. Founded in 1998, PayPal provides a payment service that makes use of email accounts and other Internet tools, and, as of October 2017, the number of PayPal subscribers had reached 218 million. If users register their credit card information with PayPal in advance, they can pay for their online shopping at a low cost, and without providing credit card data to online stores, by simply entering their PayPal ID and password and processing their purchases through this platform.

PayPal has brought a welcome breath of fresh air to traditional payment systems. Following PayPal, Apple announced Apple Pay in 2014: a payment system that makes use of the iPhone. Alipay, the payment service that China-based Alibaba Group launched in 2004, is the largest online payment service in the world and boasts at least 500 million users.

Spurred on by PayPal’s success, non-financial startup companies – not only payment systems, but also loans, asset management, fund-raising, and remittances across various financial fields globally – have emerged. These individual technologies developed by both startup and established companies are now being applied in the field of finance, and various component technologies owned by different startup companies are being combined and used, primarily by financial institutions that provide full lines of financial products.

FinTech 1.5 : The Result of New Technology

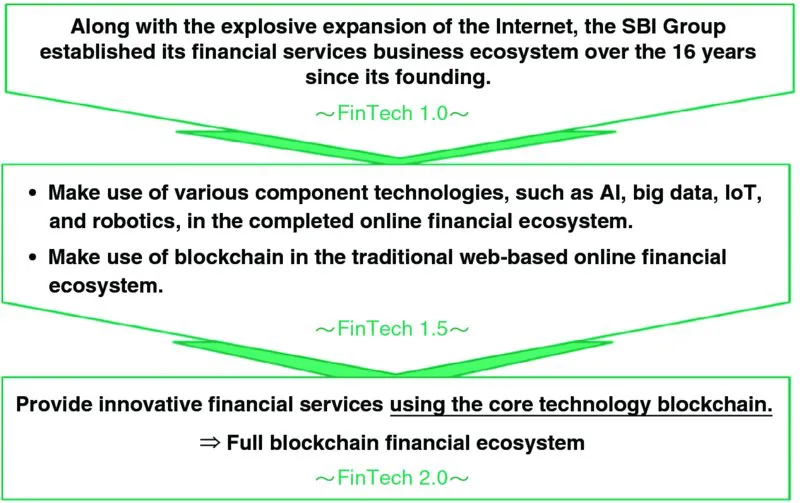

These technologies have fostered development and deployment of efficient and effective financial products in various financial fields. Component technologies include artificial intelligence (AI), big data applications, the evolution of the Internet of Things (IoT, which connects the physical world to the Internet), and robotics. The Japanese financial services industry began using these technologies – individually and in combination – about 2010. The introduction of these technologies rapidly evolved precisely when a Kondratieff wave (economic cycle that lasts 50 – 60 years caused by technological innovation) emerged, and major financial institutions began broad- scale deployment in 2012 – 2013. I refer to this trend, which has attracted attention since 2012 – 2013, as FinTech 1.5 because it is basically a more evolved form of FinTech 1.0 (Figure 1.1).

Figure 1.1 Evolution of FinTech

Source: SBI Holdings.

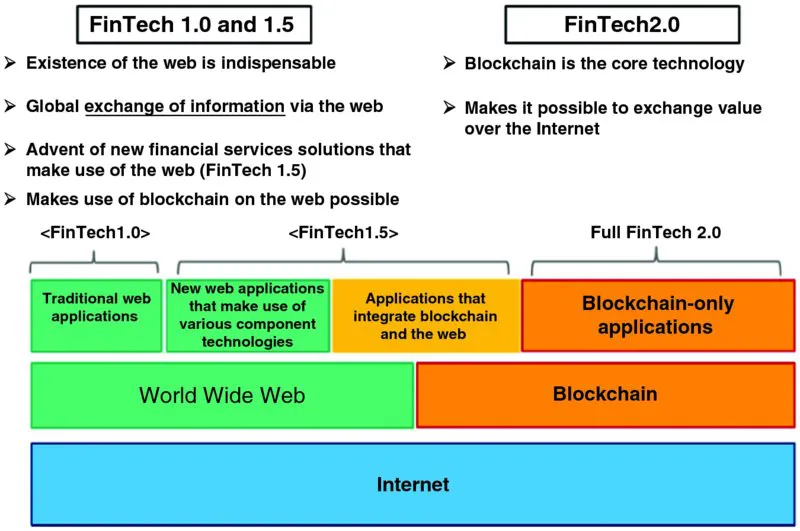

The world that I call FinTech 2.0 resides in a different dimension than that of the worlds of FinTech 1.0 or FinTech 1.5.

The existence of the Internet is indispensable to both FinTech 1.0 and FinTech 1.5, and in the world of FinTech 1.0, the World Wide Web, made it possible for individuals to freely exchange various types of data on a larger scale than ever before in human history.

In recent years, a vast array of web-based applications (apps) have been developed, and it can be argued that the combination of their commercial availability and greater use of mobile phones has enabled the worlds of FinTech 1.0 and FinTech 1.5 to develop and flourish. However, with respect to financial services, it can be argued – particularly in Japan – that we now live in the world of FinTech 1.0, a composite of online financial services that developed between 1995 and 2000, and the more-evolved system developed primarily by startup companies. For Japanese financial institutions, I would observe that their basic business has not evolved since the previous IT era.

Blockchain-based FinTech 2.0

The core technology of FinTech 2.0 is blockchain technology, and unlike FinTech 1.0 and 1.5, FinTech 2.0 does not necessarily rely entirely on the web. The advent of the Internet-based web has made it possible to exchange information throughout the world, but blockchain technology makes a global value exchange over the Internet possible. Both can exist, but they are of different natures and must be treated accordingly (Figure 1.2).

Figure 1.2 The World of FinTech 2.0

Source: SBI Holdings.

I differentiate among FinTech 1.0, 1.5, and 2.0 because if they are lumped together under the heading FinTech, there is the danger that the innovation potential and its prospects for transforming society may be underestimated. If so, it could hinder the development of blockchain technology in Japan. Since Satoshi Nakamoto published his paper on the cryptocurrency Bitcoin in 2009, blockchain technology has drawn the spotlight as the basic technology underlying Bitcoin.

Although this is only natural considering the growth of blockchain, the focus of the concept has been by and large limited to currency-related functions, as a medium of exchange and store of value. Since about 2012 – 2013, however, there have been major improvements to not only cryptocurrency frameworks but also business mechanisms (not simply those related to finance), and there has been greater awareness and expectation for the broad application of blockchain, including in the field of public administration.

During this time, one blockchain application after another began to be developed. These apps not only make use of blockchain, but are also used in combination with existing web apps. This means that blockchain technology is not only an entirely new toolkit, but also one that complements existing technologies and may be able to replace them.

Therefore, I would like to touch on the elemental and functional components of blockchain. Different people define blockchain in different ways. There are divergent definitions because blockchains have various important functions. For example, many describe blockchain as a distributed transaction ledger. This is probably a good general definition. Structurally, a blockchain is the foundation of peer-to-peer networks constructed on the Internet and can be called a fully distributed cloud system.

It can also probably be referred to as a platform that makes it possible to securely process various types of transactions involving digital assets.

Furthermore, blockchains can function as databases. Network participants (nodes) store and manage transaction history records in a distributed manner using a type of storage site referred to as a block.

Finally, blockchain technology can be considered the basic architecture supporting cryptocurrencies. Because blockchain technology was first used as the superstructure for the cryptocurrency Bitcoin, many people now have this image of blockchain technology. Bitcoin is a secured cryptocurrency because of an innovative mechanism, referred to as proof of work, which is based on a distributed consensus algorithm for gaining approval through competition between nodes.

It is evident that blockchain can be defined from various perspectives. Since its introduction, the technology has further evolved, and includes the creation of many apps.

One such application, and an extremely important one, is a concept called the smart contract: a mechanism that transforms private contracts between parties into a program on a blockchain, and then automatically executes associated contract terms. The arrival of these types of contracts can arguably be deemed a revolutionary upgrade cycle, comparable, in terms of impact, to the development of HTML (hypertext markup language), which made it possible to freely communicate information and create links to the web. The advent of smart contracts eliminates the need for m...

Table of contents

Cover

Title Page

Copyright

Contents

Preface

Contributors

Planning/Editing Staff of the SBI Group

Chapter 1: Internet Revolution and Evolution of FinTech

Chapter 2: Evolution of the SBI Group

Chapter 3: Background of the FinTech Revolution

Chapter 4: Breakthrough FinTech Companies

Chapter 5: Issues for Financial Institutions and the Legal System

Afterword

About the Author and Editor

Index

WILEY END USER LICENSE AGREEMENT

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.4M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

Both plans are available with monthly, semester, or annual billing cycles.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go. Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Learning Practical FinTech from Successful Companies by Yoshitaka Kitao in PDF and/or ePUB format, as well as other popular books in Business & Business General. We have over one million books available in our catalogue for you to explore.