The business guide to Big Data in insurance, with practical application insight

Big Data and Analytics for Insurers is the industry-specific guide to creating operational effectiveness, managing risk, improving financials, and retaining customers. Written from a non-IT perspective, this book focusses less on the architecture and technical details, instead providing practical guidance on translating analytics into target delivery. The discussion examines implementation, interpretation, and application to show you what Big Data can do for your business, with insights and examples targeted specifically to the insurance industry. From fraud analytics in claims management, to customer analytics, to risk analytics in Solvency 2, comprehensive coverage presented in accessible language makes this guide an invaluable resource for any insurance professional.

The insurance industry is heavily dependent on data, and the advent of Big Data and analytics represents a major advance with tremendous potential – yet clear, practical advice on the business side of analytics is lacking. This book fills the void with concrete information on using Big Data in the context of day-to-day insurance operations and strategy.

Understand what Big Data is and what it can do

Delve into Big Data's specific impact on the insurance industry

Learn how advanced analytics can revolutionise the industry

Bring Big Data out of IT and into strategy, management, marketing, and more

Big Data and analytics is changing business – but how? The majority of Big Data guides discuss data collection, database administration, advanced analytics, and the power of Big Data – but what do you actually do with it? Big Data and Analytics for Insurers answers your questions in real, everyday business terms, tailored specifically to the insurance industry's unique needs, challenges, and targets.

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

‘The real business of insurance is the mitigation of countless misfortunes.’

—Joseph George Robins (1856–1927)

The purpose of this book is not to create a textbook on either insurance or technology, so those who are looking for great depth of information on either are likely to be disappointed. Others who need to know the ins and outs of legal case law such as Rylands v Fletcher, or the detailed working of a Hadoop network are also likely to be disappointed, and will need to look elsewhere. Indeed, there are many books which already do good service to that cause. Perhaps helpfully, a list of recommended other reading is shown in Appendix A. This book is somewhat different as it seeks to exist in one of the exciting interfaces between insurance and technology which we have come to know as the topic of Big Data and Analytics.

Readers are most likely to come from one of two camps. For those whose origins are as insurance practitioners, they are likely to either have taken technology for granted, perhaps turned a blind eye or simply become disaffected because of the jargon used. After all, isn't technology something which happens ‘over there’ and is done by ‘other people’?

The technologist might see matters in a different way. Their way is about the challenges of data management, governance, cleansing, tooling, and developing appropriate organizational and individual capabilities. The language of ‘apps’ and ‘widgets’ is as foreign to the insurance practitioner as are terms like ‘indemnity’ and ‘non-disclosure’ to the technologist.

The practice of insurance, and the implementation of technology should not – and cannot – become mutually exclusive. Technology has become the great enabler of change of the insurance industry, and will continue to be so especially in the area of Big Data and Analytics which is one of the hottest topics in the financial services sector.

So there is the crunch: 21st-century technology and how it impacts on a 300-year-old insurance industry. To understand the future it is necessary to think for a short while about the past, to allow current thinking to be placed in context.

1.1 On the Point of Transformation

The starting point of this journey is over 350 years ago, in 1666, when Sir Christopher Wren allowed in his plans for rebuilding London for an ‘Insurance Office’ to safeguard the interests of the leading men of the city whose lives had been ruined by the destruction of homes, businesses and livelihoods. Some might even argue that a form of insurance existed much earlier, in China, Babylon or Rome. Before the end of the 17th century several insurance societies were already operating to provide cover in respect of damage to property and marine, and the insurance of ‘life’ emerged in the early 18th century. It might be argued that mutuals and co-operatives existed much earlier, but that debate can be put aside for the moment.

The principles of insurance are founded on case law with the foundations of insurable interest, utmost good faith and indemnity being enshrined in the early 18th century, and remain substantially unchanged. Even some of the largest global insurance companies themselves have their feet in the past albeit with some name changes. Royal Sun Alliance can trace their history to 1710 and Axa to about 1720. Those walking the streets of London will be familiar with names and places on which are founded the heritage of the insurance industry as it is known today.

It is against that background of tradition that the insurance industry now finds itself in a period of transition, perhaps transformation, maybe even radicalization. Traditional approaches for sale and distribution of insurance products are being cast aside in favor of direct and less expensive channels. The industry is on the cusp of automated claims processes with minimal or perhaps no human intervention. Fraudsters have always existed in the insurance space, but are now more prevalent and behaving with a degree of professionalism seldom seen before. Insurers are increasingly able to develop products suited to an audience of one, not of many. Quite simply, the old rules of engagement are being reinvented.

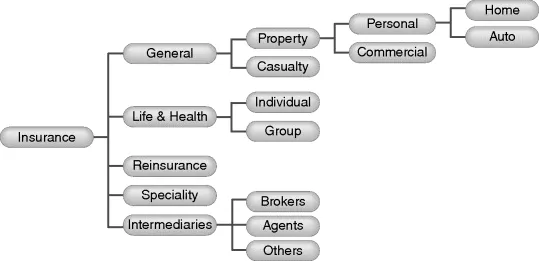

Coupled with this is the challenge of different levels of analytical maturity by market sector, by company, by location, even by department. Figure 1.1 starts to give some indication of the way the insurance industry is structured.

But this is not just a book about an industry, or an insurance company, or department. It is as much a book about how individuals within the profession itself need to become transformed.

Figure 1.1 The insurance industry

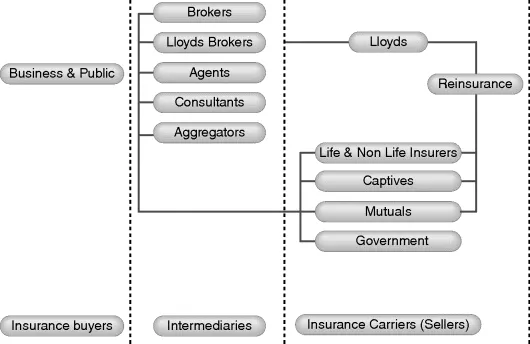

Traditional skills will increasingly be replaced by new technologically driven solutions. New job descriptions will emerge. Old campaigners who cannot learn the new tools of the industry may find it difficult to cope. Professional institutes will increasingly need to reflect this new working environment in their training and examinations. The insurance industry as a whole also comprises multiple relationships (Figure 1.2), some of which are complex in nature.

Figure 1.2 Relationships between parties

Even within single insurance organizations there are many functions and departments. Some operate as relative silos with little or no interference from their internal peers. Others such as Head Office functions like HR sit across the entirety of the business (Figure 1.3). All of these functions have the propensity for change, and at the heart of all these changes rests the topic of Big Data and Analytics.

Figure 1.3 Insurance functions

1.1.1 Big Data Defined by Its Characteristics

Big Data may be ‘big news’ but it is not entirely ‘new news’. The rapid growth of information has been recognized for over 50 years although according to Gil Press who wrote about the history of Big Data in Forbes1 the expression was first used in a white paper published in 2008.

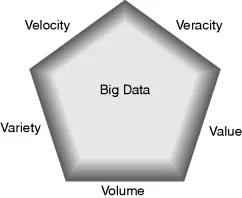

With multiple definitions available, Big Data is best described by five key characteristics (Figure 1.4) which are:

Figure 1.4 Big Data defined by its characteristics

Volume – the sheer amount of structured and unstructured data that is available. There are differing opinions as to how much data is being created on a daily basis, usually measured in petabytes or gigabytes, one suggestion being that 2.5 billion gigabytes of information is created daily.2 (A ‘byte’ is the smallest component of computer memory which represents a single letter or number. A petabyte is 1015 bytes. A ‘gigabyte’ is one-thousand million bytes or 1020 bytes.) But what does this mean? In 2010 the outgoing CEO of Google, Eric Schmidt, said that the same amount of information – 5 gigabytes – is created in 48 hours as had existed from ‘the birth of the world to 2003.’ For many it is easier to think in terms of numbers of filing cabinets and whether they might reach the moon or beyond but such comparisons are superfluous. Others suggest that it is the equivalent of the entire contents of the British Library being created every day.

It is also tempting to try and put this into an insurance context. In 2012 the UK insurance industry created almost 90 million policies, which conservatively equates to somewhere around 900 million pages of policy documentation. The 14m books (at say 300 pages apiece) in the British Library equate to about 4.2 billion pages or equivalent to around five years of annual UK policy documentation. In other words, it would take insurers five years to fill the equivalent of the British Library with policy documents (assuming they wanted to). But let's not play games – it is sufficient to acknowledge that the amount of data and information now available to us is at an unprecedented level.

Perhaps because of the enormity of scale, we seek to define Big Data not just by its size but by its characteristics.

Velocity – the speed at which the data comes to us, especially in terms of live streamed data. We also describe this as ‘data in motion’ as opposed to stable, structured data which might sit in a data warehouse (which is not, as some might think, a physical building, but rather a repository of information that is designed for query and analysis rather than for transaction processing).

‘Streamed data’ presents a good example of data in motion in that it comes to us through the internet by way of movies and TV. The speed is not one which is measured in linear terms but rather in bytes per second. It is governed not only by the ability of the source of the data to transmit the information but the ability of the receiver to ‘absorb’ it. Increasingly the technical challenge is not so much that of creating appropriate bandwidth to support high speed transmittal but rather the ability of the system to manage the security of the information.

In an insurance context, perhaps the most obvious example is the whole issue of telematics information, which flows from mobile devices not only at the speed of technology but also at the speed of the vehicle (and driver) involved.

Variety – Big data comes to the user from many sources and therefore in many forms – a combination of structured, semi-structured and unstructured. Semi-structured data presents problems as it is seldom consistent. Unstructured data (for example plain text or voice) has no structure whatsoever.

In recent years an increasing amount of data is unstructured, perhaps as much as 80%. It is suggested that the winners of the future will be those organizations which can obtain insight and therefore extract value from the unstructured information.

In an insurance context this might comprise data which is based on weather, location, sensors, and also structured data from within the insurer itself – all ‘mashed’ together to provide new and compelling insights. One of the clearer examples of this is in the case of catastrophe modeling where insurers have the potential capability to combine policy data, policyholder input (from social media), weather, voice analysis from contact centers, and perhaps ot...

Table of contents

Cover

Series Page

Title Page

Copyright

Preface

Acknowledgements

About the Author

Chapter 1: Introduction – The New ‘Real Business’

Chapter 2: Analytics and the Office of Finance

Chapter 3: Managing Financial Risk Across the Insurance Enterprise

Chapter 4: Underwriting

Chapter 5: Claims and the ‘Moment of Truth’

Chapter 6: Analytics and Marketing

Chapter 7: Property Insurance

Chapter 8: Liability Insurance and Analytics

Chapter 9: Life and Pensions

Chapter 10: The Importance of Location

Chapter 11: Analytics and Insurance People

Chapter 12: Implementation

Chapter 13: Visions of the Future?

Chapter 14: Conclusions and Reflections

Appendix A: Recommended Reading

Appendix B: Data Summary of Expectancy of Reaching 100

Appendix C: Implementation Flowcharts

Appendix D: Suggested Insurance Websites

Appendix E: Professional Insurance Organizations

Index

End User License Agreement

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

Both plans are available with monthly, semester, or annual billing cycles.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go. Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Analytics for Insurance by Tony Boobier in PDF and/or ePUB format, as well as other popular books in Economics & Banks & Banking. We have over 1.5 million books available in our catalogue for you to explore.