The time for financial technology innovation is now

Marketplace Lending, Financial Analysis, and the Future of Credit clearly explains why financial credit institutions need to further innovate within the financial technology arena. Through this text, you access a framework for applying innovative strategies in credit services. Provided and supported by financial institutions and entrepreneurs, the information in this engaging book encompasses printed guidance and digital ancillaries.

Peer-to-peer lenders are steadily growing within the financial market. Integrating peer-to-peer lending into established credit institutions could strengthen the financial sector as a whole, and could lead to the incorporation of stronger risk and profitability management strategies.

Explain (or Explore) approaches and challenges in financial analysis applied to credit risk and profitability

Explore additional information provided via digital ancillaries, which will further support your understanding and application of key concepts

Navigate the information organised into three subject areas: describing a new business model, knowledge integration, and proposing a new model for the Hybrid Financial Sector

Understand how the rise of fintech fits into context within the current financial system

Follow discussion of the current status quo and role of innovation in the financial industry, and consider the financial technology innovation landscape from the perspective of an entrepreneur

Marketplace Lending, Financial Analysis, and the Future of Credit is a critical text that bridges the gap in understanding between financial technology entrepreneurs and credit institutions.

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

PART One FinTech and the Online Lending Landscape—Where Are We Now?

Online lending platforms have become a large part of the thriving FinTech sector, and startups in the space have become a mainstay in the financial press in recent years. Large amounts of venture capital are flowing into the sector. Many of the current initiatives in financial technology innovation promise great disruption to the status quo in finance. It has become popular to predict the demise of banking as we know it. In fact, the Financial Times even dedicated a series to the subject, aptly titled “Death of Banks.”1 But are recent FinTech innovations really a threat to the existing financial system? And if they are, who says that their solutions will be superior to those that exist today and consumers will be better off?

Even though banks are facing assaults on their hegemony on different fronts—payments, foreign exchange, wealth management, lending—we focus on online lending in this book. Let's first define what we mean with this broad term. Roughly speaking, online lending describes the emerging market outside of the established financial sector that is using technology to disrupt the lending market. There exist several business models in the online lending space, and different authors use different terminology to describe similar things. We realize this discussion can become confusing unless we agree on which terms we use for which approach. This is why we will describe several FinTech business models in more detail in Chapter 1, which will set out which terms describe which approaches in the rest of this book when we speak about marketplace lending.

Despite our focus on online lending, we also need an overview of the entire FinTech sector to understand the status quo and potential of the emerging hybrid financial sector. Many of the technologies are overlapping and building on each other. In their current form, most financial technology startups are still operating at small scale compared to the transaction volumes of established banks. In reality, FinTech startups in their current form are far from a threat. Nevertheless, the sector is attracting large amounts of venture capital, and this trend is set to continue, with global investment in FinTech on track to grow to up to $8 billion by 2018.2 At the same time, Gartner points out that banking and securities institutions are spending roughly $485 billion on information technology in 2014.3 On a global scale, the United States attracts the lion's share of FinTech investment, about 83 percent of global investment in 2013. Several hubs for activity of financial technology startups have emerged in recent years. Silicon Valley is the biggest FinTech cluster in the world, New York ranks second. London and Hong Kong are evolving as hotspots for startups as well.

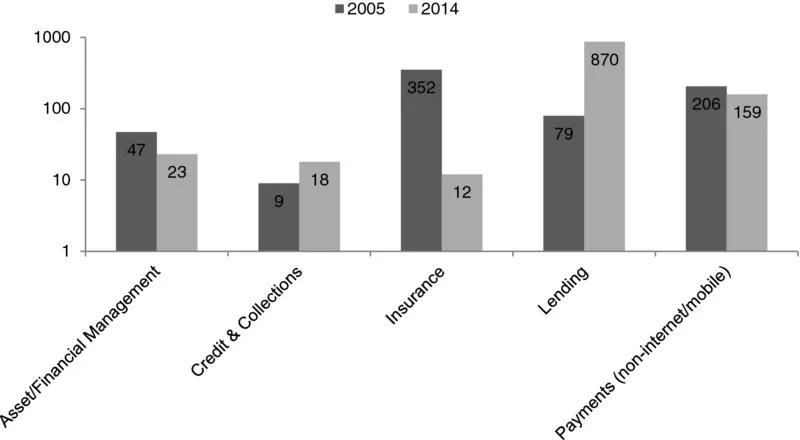

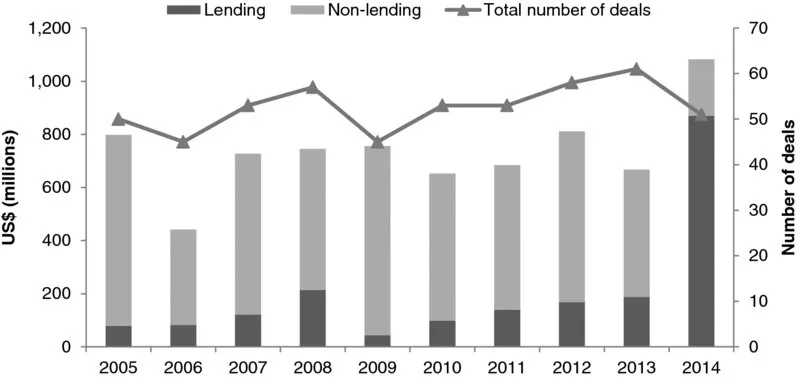

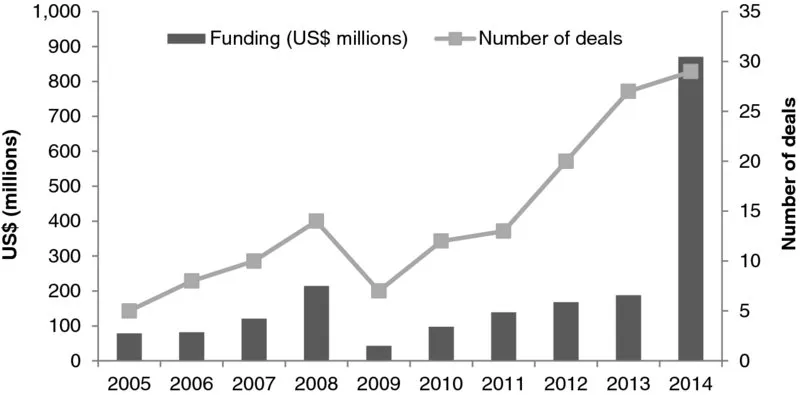

Out of the different focus areas of FinTech companies, lending has emerged as a winner in recent years. Especially in the United States, lending companies lead both in terms of the absolute amount of venture capital funding it attracts (Figure P1.1) and the share of total investment in financial companies (Figure P1.2). Figure P1.3 shows venture capital funding over time and the number of investments in lending companies between 2005 and 2014 in the United States. The data consider investments of venture capital firms in financial companies other than FinTech. Nevertheless, the growth trend of capital flows into the lending space is evident. Lending attracted US$ 870 million of venture capital in the United States in 2014, roughly 80 percent of the total investment amount for the year. In comparison, venture capital investors invested less than 10 percent of their funds in lending companies in 2005. Remember that these are equity investments in companies, not capital invested in loans originated by these companies. Another interesting observation is the relative draw of venture capital from the white-hot payments sector: even though mobile payments and digital wallets seem to occupy a prominent share of media attention, they were attracting less capital in 2014 than in 2005. The multiple of investment in payments over lending has changed from roughly 2.6 in 2005 (payments attracted 2.6 times the capital of lending) to under 0.2 in 2014.

Figure P1.1 U.S. venture capital flowing into selected financial companies (US$ millions), excluding corporate venture capital

Data source: CB Insights

Figure P1.2 U.S. venture capital deal volume (US$), number of deals in financial companies, and proportion of investment in lending companies of total investment in financial companies, excluding investment banking and funds

Data source: CB Insights

Figure P1.3 U.S. venture capital investment volume and number of deals in lending companies

Data source: CB Insights

The rise of online lending as a leader in the FinTech space is expected: current interest rates are at their lowest since the financial crisis of 2007/8. However, transaction volumes of online lending platforms still pale in comparison with those of the conventional financial sector. Nevertheless, author Charles Moldow predicts that by 2025, $1 trillion in loans will be originated on marketplace lending platforms globally.4 Many technology experts predict that, in the near future, innovations in financial technology will pave the way for a massive paradigm shift that will unseat the existing players in financial markets. This is a possibility. No monopolist has been able to keep the walls up for over a hundred years. In essence, what financial technology startups promise is making transactions cheaper, faster, and more transparent, by replacing the current lending institutions with more effective platforms. They are “trying to eat the banks' lunch,” as Jamie Dimon, chief executive of JPMorgan Chase, put it.5 But can FinTech companies follow through on their promises?

The logical next step for online lenders and established credit institutions is to find common ground and join forces—at least in some respects. First baby steps are already taking place: banks including Citigroup, Capital One, Bank of Montreal, Barclays and Deutsche Bank are currently exploring ways to finance or securitize loans originated by online lenders.6 This makes it seem as if online lending platforms simply served as sales offices for uncollateralized subprime loans for shadow banks. Of course, there are better ways to explore synergies between online lenders and banks, and all parties in the financial sector have complementary roles. When they work together, great opportunities arise to advance the financial industry toward providing better financial services and a more stable financial system. In the coming chapters, we will address some of the common themes around which innovation in online lending takes place today. We will also examine opportunities and risks. Integrating innovative, customer-centric approaches into banks comes with challenges of its own, and both innovators and banks should understand what they are getting involved in before embarking on the journey. Let's now get an overview of the FinTech sector before we focus on online lending in more detail.

NOTES

1 Kaminska, Izabella (2014a) “Death of Banks,” Financial Times, http://ftalphaville.ft.com/tag/death-of-banks/, data accessed 9 December 2014. 2 Accenture (2014) “The Rise of FinTech: New York's Opportunity for Tech Leade...

Table of contents

Cover

Series

Titlepage

Copyright

Dedication

Preface

Acknowledgments

About the Authors

About the Website

Introduction

Part One: FinTech and the Online Lending Landscape—Where Are We Now?

Part Two: The Status Quo of Analytics in the Financial Industry—The Perspective of Banks

Part Three: Toward the Future of the Hybrid Financial Sector

Bibliography

Index

EULA

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

Both plans are available with monthly, semester, or annual billing cycles.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go. Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Marketplace Lending, Financial Analysis, and the Future of Credit by Ioannis Akkizidis,Manuel Stagars in PDF and/or ePUB format, as well as other popular books in Business & Finance. We have over 1.5 million books available in our catalogue for you to explore.