Risk management solutions for today's high-speed investing environment

Real-Time Risk is the first book to show regular, institutional, and quantitative investors how to navigate intraday threats and stay on-course. The FinTech revolution has brought massive changes to the way investing is done. Trading happens in microsecond time frames, and while risks are emerging faster and in greater volume than ever before, traditional risk management approaches are too slow to be relevant. This book describes market microstructure and modern risks, and presents a new way of thinking about risk management in today's high-speed world. Accessible, straightforward explanations shed light on little-understood topics, and expert guidance helps investors protect themselves from new threats. The discussion dissects FinTech innovation to highlight the ongoing disruption, and to establish a toolkit of approaches for analyzing flash crashes, aggressive high frequency trading, and other specific aspects of the market.

Today's investors face an environment in which computers and infrastructure merge, regulations allow dozens of exchanges to coexist, and globalized business facilitates round-the-clock deals. This book shows you how to navigate today's investing environment safely and profitably, with the latest in risk-management thinking.

Discover risk management that works within micro-second trading

Understand the nature and impact of real-time risk, and how to protect yourself

Learn why flash crashes happen, and how to mitigate damage in advance

Examine the FinTech disruption to established business models and practices

When technology collided with investing, the boom created stratospheric amounts of data that allows us to plumb untapped depths and discover solutions that were unimaginable 20 years ago. Real-Time Risk describes these solutions, and provides practical guidance for today's savvy investor.

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Do you wonder why the markets have changed so much? Where's it all heading? How will it affect you? You are not alone. Today's markets are very different from what they used to be. Technological advances morphed computers and infrastructure. Changes in regulation allowed dozens of exchanges to coexist side by side. The global nature of business has ushered in round‐the‐clock deal making. All of this has created stratospheric volumes of data. The risks that come along with automated trading in real‐time are numerous. Now, the inferences from these data allow us to go to previously untapped depths of markets and discover problems and solutions that could not even be imagined 20 years ago.

Do you remember Bloomberg terminals? If so, you are reading this book not so long after it was written. JP Morgan's January 2016 announcement “to pull the plug” on thousands and thousands of Bloomberg terminals is a leading example of the sweeping disruption facing investment managers. Billion‐dollar hedge fund Citadel followed suit on August 16, 2016, by announcing that it was taking on Symphony messaging as Bloomberg's replacement. Symphony, who? Many still struggle to wrap their head around the situation, with social media platforms like LinkedIn buzzing with discussions about pulling the plug on traditional sources of market data. Yet, here is fact: The competition is not sleeping, but working hard. And now, the competition is so strong that Bloomberg, Thomson Reuters, and others may end up in significant financial peril if they ignore fintech. Is your company also oblivious to changes in innovation?

The unfortunate truth is that many established firms are completely unprepared for the fast train of innovation currently passing them by. Old, manual procedures may have been fine in the past, but with innovation sweeping through, risk management executives have to be ready to see established operating models and platforms go out the door as newer, untried approaches take their place.

Consider the investment advisory industry. Reliance on charming brokers to seduce ever‐dwindling pools of clients into paying for their commissions and overhead expenses remains the business model for some firms. At the same time, a number of well‐established startups deliver cutting‐edge portfolio‐management advice to investors right over the Internet, with some charging as little as $9.95 per month.

Global banks like Barclay's and Credit Suisse have exited the US wealth management arena while at the same time hundreds of millions of dollars in venture funding have been channeled to fintech startups working to streamline financial advice and beyond.

The bet has been wagered that new innovative and cost‐efficient business models are here to stay. Innovation can take the form of a completely new approach to conducting business or through advances in the information used for the existing way of conducting business. As an illustration, while many finance professionals are still debating market structure and whether a new exchange will help people avoid high‐frequency traders, companies like AbleMarkets deliver a streaming map of high‐frequency trading activity directly to subscribers' desktops, leaving nothing to chance and helping to significantly improve trading performance across all markets. Similar innovations are going on in insurance, risk management, and other aspects of financial services, and firms that are not up to par on what's going on are at a significant risk of failure.

EVERYONE IS INTO FINTECH

Have you ever missed opportunities in the markets because you felt you were disrupted? We have been in a unique and fortunate position to be immersed in the heart of fintech innovation and to observe first‐hand the extent of what is becoming a true disruption to businesses that, in turn, disrupted financial markets in the late 1970s and 1980s. Think of this as Finance 3.0. The possibilities are endless, and the new players are already embedded in most facets of traditional finance. These new players are not boiler rooms—most founders have advanced degrees and the most recent scientific innovations at their fingertips.

According to the Conference Board, investment in financial technology, trendily abbreviated into fintech, grew by 201 percent in 2014 around the world. In comparison, overall venture capital investments have only grown by 63 percent. The digital revolution is well underway for banks, asset managers, and customers. The impact on the financial institutions from the many startups that are trying unproven ideas is beginning to crystallize. Venture capitalists are betting that the once‐stodgy financial industry is about to experience a considerable transformation.

The pace of change for the financial world is speeding up, and startups and venture capitalists are hardly alone in the fintech craze. Apple, Amazon, and Google, among others, have already launched financial services platforms. They have aimed at niches where they can establish a strong position. Threatened by these new entrants, traditional financial stalwarts are hearing the pitch: Adapt to the new environment or perish.

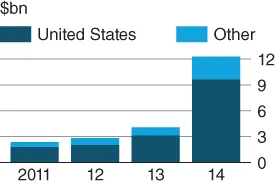

Banks are launching their own internal funds and hiring significant numbers of developers for internal builds. Why now? In his latest annual letter to shareholders, Jamie Dimon, CEO of JPMorgan Chase, wrote that “Silicon Valley is coming.” While this statement went unnoticed by the news, it reflects the torrent of venture capital flowing into fintech. Estimates by the Economist, shown in Figure 1.1, suggest that 2014 was the watershed year for fintech startups.

Figure 1.1 Global fintech investment

Source: Economist, May 19, 2015.

The Current State of Big Data Finance

What is big data finance? For many financial practitioners, big data is still just a buzzword, and finance is business as usual. However, looking at the hottest‐financed areas of business, one uncovers particular trends that move beyond buzz into billion‐dollar investments. According to Informilo.com, for instance, the fastest‐growing areas of big data in finance in 2015 were:

Payment services

Online loans

Automated investing

Data analytics

Each of these areas, in turn, translates into automation. The payment services businesses, such as TransferWise, harness technology to commoditize counterparty risk computations. Counterparty risk is a risk of payment default by a money‐sending party. Some 20 years ago, counterparty risk was managed by human traders, and all settlements took at least three business days to complete, as multiple levels of verification and extensive paper trails were required to ensure that transactions indeed took place as reported. Fast‐forward to today, and ultra‐fast technology enables transfer and confirmation of payments in just a few seconds, fueling a growing market for cashless transactions.

Similarly, the loan markets used to demand labor‐intensive operations. Just 10 years ago, the creditworthiness of a bank's business borrowers were often judged during a round of golf and drinks with the company's executives. Of course, quantitative credit‐rating models such as the one by Edward Altman of New York University have proved invariably superior for predicting defaults over most human experts, enabling faster online loan approvals. Online loan firms now harness these quantitative credit‐modeling approaches to produce fast, reliable estimates of credit risk and to determine the appropriate loan pricing.

Can anyone issue loans over the Internet or facilitate payments? According to recent industry reports, yes, the founders of many loan startups that originated during the credit squeeze of 2009—have little prior background in lending.

The key issues in lending are (1) having capital to lend, and (2) estimating credit risk of the borrowers correctly. The pricing of the loan service, interest, is then a function of the credit rating. If and when a borrower defaults, the loan should be optimally paid out from the interest. More generally, the average loan interest should exceed the average loan amount outstanding in order for the lender to make money.

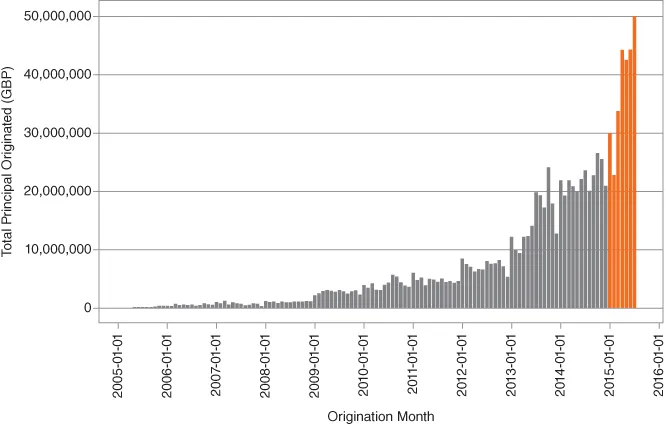

The lending business is central to banking, and banks have had a near monopoly over the lending business for a very long time. New approaches to lending have emerged that compete with banks. Banks fund loans with deposits, whereas peer‐to‐peer lending is funded by investors. The leading players in this new approach to lending are the LendingClub and Prosper in the United States and Funding Circle and Zopa in the United Kingdom. In 2015, Zopa passed the Great Britain pound (GBP) 1 billion mark. Zopa's growth is shown in Figure 1.2.

Figure 1.2 Zopa originations by month

Source: p2p‐banking.com

With peer‐to‐peer lenders prospering with their new model, not only have banks noticed, but in some cases, started to acquire the upstart companies. SunTrust Bank acquired FirstAgain in 2012, later rebranding it LightStream.

New technologies are making their presence felt in wealth management as well. The topics of the robo‐advising and a broad group of analytics are the most diverse and least exact. Robo‐advising takes over the job of traditional portfolio management. The idea behind robo‐advising is that a computer, programmed with algorithms, is capable of delivering portfolio‐optimized solutions faster, cheaper, and at least as good as its human counterparts, portfolio managers. Given a selected input of parameters to determine the customer's risk aversion and other preferences (say, the customer's life stage and philosophical aversion to selected stocks), the computer then outputs an investing plan that is optimal at that moment.

Automation of investment advice enables fast market‐risk estimation and the associated custom portfolio management. For example, investors of all stripes can now choose to forgo expensive money managers in favor of investing platforms such as Motif Investing. For as little as $9.95, investors can buy baskets of ETFs preselected on the basis of particular themes. Com...

Table of contents

Cover

Table of Contents

Title Page

Copyright

Dedication

Acknowledgments

Chapter 1: Silicon Valley Is Coming!

Chapter 2: This Ain't Your Grandma's Data

Chapter 3: Dark Pools, Exchanges, and Market Structure

Chapter 4: Who Is Front‐Running You?

Chapter 5: High‐Frequency Trading in Your Backyard

Chapter 6: Flash Crashes

Chapter 7: The Analysis of News

Chapter 8: Social Media and the Internet of Things

Chapter 9: Market Volatility in the Age of Fintech

Chapter 10: Why Venture Capitalists Are Betting on Fintech to Manage Risks

Authors' Biographies

Index

End User License Agreement

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

Both plans are available with monthly, semester, or annual billing cycles.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go. Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Real-Time Risk by Irene Aldridge,Steven Krawciw in PDF and/or ePUB format, as well as other popular books in Business & Finance. We have over 1.5 million books available in our catalogue for you to explore.