Leave the old paradigm behind and start safeguarding your portfolio

Short Selling with the O'Neil Disciples is a guide to optimizing investment performance by employing the unique strategies put forth by William O'Neil. The authors traded these strategies with real money, then refined them to reflect changing markets and conditions to arrive at a globally-relevant short-selling strategy that helps investors realize maximum profit. Readers will learn how short selling recognizes the life-cycle paradigm arising from an economic system that thrives on 'creative destruction,' and has been mischaracterized as an evil enterprise when it is simply a single component in smart investing and money management. This informative guide describes the crucial methods that preserve gains and offset declines in other stocks that make up a portfolio with more of an intermediate- to long-term investment horizon, and how to profit outright when markets begin to decline.

Short-selling is the act of identifying a change of trend in a stock from up to down, and seeking to profit from that change by riding the stock to the downside by selling the stock while not actually owning it, with the idea of buying the stock back later at a lower price. This book describes the methods that make short-selling work in today's markets, with expert advice for optimal practice.

Learn the six basic rues of short-selling

Find opportunities on both the long and short sides of stocks

Practice refined methods that make short-selling smarter

Examine case studies that profitably embody these practices

Investors able to climb out of the pessimistic, conspiratorial frame of mind that fixates on the negative will find that short selling can serve as a practical safeguard that will protect the rest of their portfolio. With clear guidance toward the techniques relevant in today's markets, Short Selling with the O'Neil Disciples is an essential read.

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Reduced to its mechanics, short-selling is simply the act of identifying a change of trend in a stock from up to down and then seeking to profit from that change of trend as one rides the stock to the downside. To do this, the investor or trader sells the stock in question while not actually owning it, e.g., being “short” the stock, and pockets the proceeds of the sale with the idea of buying the stock back later at a lower price as the downtrend takes hold and extends to the downside. To go short, the seller must first borrow the stock from her broker and may have to pay a very small fee to do so. If and when the stock drops in price, the seller then repurchases the shares, “covering” her short position for less than she sold them, returning the borrowed securities and pocketing the difference. This is, of course, not a risk-free proposition, as the short-seller may also end up owing the difference if the stock rises in price and the cost of buying back those shares exceeds the proceeds they pocketed at the time of the initial short-sale. Because stocks can theoretically rise to infinity, while their decline is finite given that a stock price cannot go below zero, or 100 percent of its current value, then the potential losses a short-seller faces are unlimited. Of course, this assumes that a short-seller is operating without a stop-loss that provides a clear point at which the short-sale would be covered and the trade closed out at a loss, hopefully a small one.

To some, short-selling represents the “dark side” of the market, and history has often characterized the art of selling short as an evil enterprise, embodying a conspiratorial or pessimistic frame of mind that fixates on the negative. Consider that during the Great Crash of 1929, Jesse Livermore made $100 million in 1929 dollars, an astronomical sum at that time, by short-selling stocks during this severe market downturn. When this was later disclosed to the public, Livermore was the subject of extreme public outrage, even to the point where his short-selling activities were blamed as part of the cause of the great crash. In reality, Livermore merely observed and acted upon the market facts as they became apparent. The true cause of the Crash of 1929 was the fact that everyone had piled into the market and there was nobody left to buy stocks at that point. As well, paltry 10 percent margin requirements allowed investors to buy $100 worth of stock with only $10 in their pocket, creating a massive asset bubble and the optimal conditions for a rapid and destructive popping of that bubble.

Thus stocks find their value given the circumstances, and short-sellers can act as a catalyst to help stocks reach their true value faster than they might without any short-sellers. Supply–demand mechanics have shown time and time again that even when short-sellers pile onto stocks as they did the dot.coms, such as Amazon.com (AMZN) in the early 2000s, their short-selling has no long-term effect on depressing price if the perceived value of the stock continues to be higher than where the stock is currently trading.

Nevertheless, during the earlier existence of the United States, short-selling was in fact banned because of the inherent instability of the then very young country's fragile markets, mostly thanks to speculation surrounding the outcome of the War of 1812. It was not until 1850 that the short-selling ban was repealed. More recently, in 2008, government officials banned the short-selling of certain financial stocks that had come under pressure as a result of severe, even deadly, liquidity issues related to having swarms of bad mortgages held on their books. Excesses in the mortgage industry, fostered by government subsidies and policies that forced and/or allowed banks to lower their lending standards in order make home loans to low-income consumer borrowers who had no means of paying back the loans, created a housing bubble as demand for homes was artificially spiked, sending real estate prices soaring. These low-quality mortgages were in turn repackaged into bundles known as mortgage-backed securities (MBS), and the structure of these MBSs magically enabled them to be rated Triple-A by the credit-rating agencies such as Standard & Poor's and Moody's. With Triple-A ratings, such mortgage-backed securities were eagerly purchased by investors, ending up en masse on the books of a large number of financial institutions as well as in the portfolios of many institutional and retail investors. When the real estate bubble finally popped in 2008, these loans went bad, sending the institutions that had many of these mortgages on their books into insolvency.

In keeping with the fact that history often rhymes with the present, government officials attempted to deflect part of the blame for the financial crisis of 2008 onto short-sellers who were accused of the predatory practice of “naked” short-selling as they swarmed vulnerable financial stocks on the short side and helped to drive their prices lower. Forget the fact that short-sellers were doing little more than what smart speculators do in the first place, which is to identify a potential or emerging trend and to then capitalize on it by investing in the direction of that trend. The excesses of the mortgage and housing industries by 2008 deserved to be exposed for the frauds that they were, and short-sellers were simply part of that process of exposure and “cleansing.” As well, investors who were foolish enough to buy the stocks of financial companies on the way down did not heed what the trend was telling them. Obviously, anyone who understood what was going on knew that the only logical endpoint for the excesses of the housing and mortgage industry and the resulting insolvencies that it produced once the bubble popped was bankruptcy. And that is precisely what happened to venerable financial institutions like Lehman Brothers, Merrill Lynch, and Bear Stearns, which went belly-up or were absorbed by other financial companies.

Aggressive short-selling was alleged by regulators to have played a role in the demise of both Lehman Brothers and Bear Stearns, but the fact is that the insolvency of the financial system in 2008 was real, and true insolvency leads to bankruptcy, whether the stock is a favorite target of short-sellers or not. Without the Fed stepping in to flood the system with unprecedented amounts of liquidity using unprecedented systemic schemes collectively known as quantitative easing, or QE for short, more such financial institutions would have suffered the same fate as Lehman Brothers and Bear Stearns. Ultimately, the Financial Accounting Standards Board (FASB) would also step in to aid the Fed's QE propping by changing Rule 157, otherwise known as the “mark-to-market rule,” which required financial institutions to value their assets at fair market value. By allowing banks and other financial institutions to value their bad mortgages at whatever they wanted to rather than what they were in fact worth, further insolvencies in the system were avoided, at least temporarily and on paper.

What is interesting to observe is that the government's creation of an entirely artificial force to prop up and stimulate a reversal in the deleterious downtrend of the financial sector stocks is accepted as a legitimate way to influence stock prices, but the actions of short-sellers are seen as an unnatural and evil influence. We would argue that short-selling is a natural part of the process that defines the life-cycles of all stocks as they benefit from growth and the ensuing speculative excess on the upside, but at some point must go through a process of correction and downside price movement that clears the decks, so to speak, and either helps to build a foundation for a new uptrend and cycle of growth or results in a final and complete demise of a company that is no longer able to compete in its core industry. In a sense, the demise of older companies also helps to foster new growth cycles in that the way is cleared for newer, more innovative companies to supplant the older, slower, and larger companies that have lost their innovative and, hence, competitive edge. Short-selling, at its core, is nothing less than the investment manifestation of the virtuous cycle of creation and destruction, as well as the periodic need to cleanse excesses from the system that is the hallmark of an entrepreneurial economy.

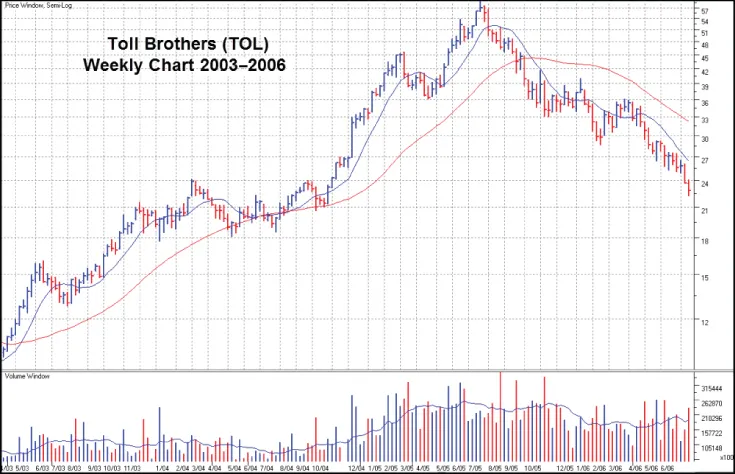

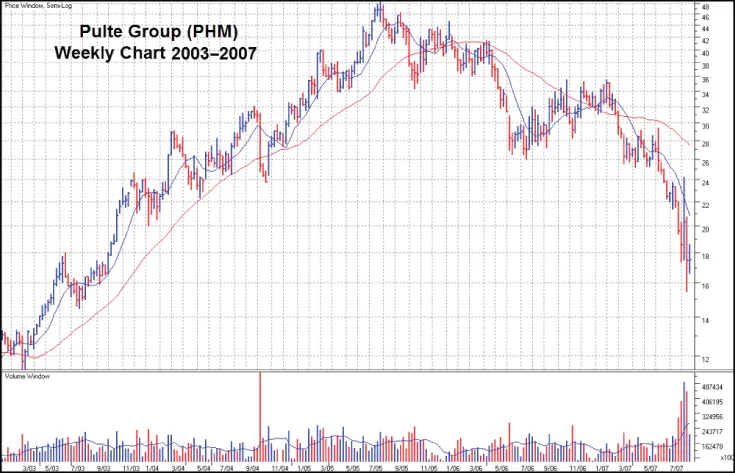

As a very instructive and current example, one need look no further than the financial crisis of 2008 and the market events that led up to it. The reality is that the financial crisis of 2008 and the severe bear market that accompanied it actually began well before it reached full-blown crisis proportions between September 2008 and April 2009. It began quietly with the topping of home-building stocks in July of 2005. Recall that the financial crisis was a function of a mortgage crisis based on the promotion and writing of ridiculously risky home loans by banks and other home-lending institutions. The lowering of lending standards in turn fueled what was really a ballooning artificial demand for houses, and this heroin-induced rush of home buying drove home prices higher, spurring a homebuilding boom that manifested in the stock market as a strong uptrend in the prices of homebuilding and building-related stocks from 2000–2005. While the demand for housing reached a crescendo in 2006–2007, homebuilding stocks had already begun to top, as the charts of two separate homebuilding stocks, Toll Brothers (TOL) and Pulte Group (PHM) (Figures 1.1 and 1.2) show.

Figure 1.1 Toll Brothers (TOL) weekly chart, 2003–2006. Luxury homebuilder TOL topped in July of 2005 with the rest of the homebuilding stocks, presaging the coming housing and mortgage crisis that would shake the financial market three years later.

Figure 1.2 Pulte Group (PHM) weekly chart, 2003–2007. This builder of single-family homes, townhouses, condominiums, and duplexes in 28 states had a nearly tenfold price move from 2000 to midsummer 2005.

Homebuilding stocks to a large extent represented the point at which the rubber meets the road for the financial crisis as the consumer “end-product” of the housing stimulus, provided by an extremely low interest rate environment and lax lending standards both mandated and promoted by government policies that were readily embraced by the home-loan industry. As more and more consumers purchased homes they could not afford, eventually the chickens...

Table of contents

Cover

Title Page

Copyright

Table of Contents

Dedication

Preface

Acknowledgments

Chapter 1: Introduction to Short-Selling

Chapter 2: Short-Selling Essentials

Chapter 3: Short-Selling Set-Ups: Chart Patterns for the Dark Side

Chapter 4: In and Out: The Mechanics of Short-Selling

Chapter 5: Case Study #1: Apple (AAPL) in 2012–2013

Chapter 6: Case Study #2: Netflix (NFLX) in 2011

Chapter 7: Case Study #3: Keurig Green Mountain (GMCR) in 2011

Chapter 8: Case Study #4: 3D Systems (DDD) in 2014

Chapter 9: Case Study #5: Molycorp (MCP) in 2011

Chapter 10: Templates of Doom: A Short-Selling Model Book

About the Authors

Index

End User License Agreement

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

Both plans are available with monthly, semester, or annual billing cycles.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go. Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Short-Selling with the O'Neil Disciples by Gil Morales,Chris Kacher in PDF and/or ePUB format, as well as other popular books in Business & Trading. We have over 1.5 million books available in our catalogue for you to explore.