A Client-Centered approach to Financial Planning Practice built by Research for Practitioners

The second in the CFP Board Center for Financial Planning Series, Client Psychology explores the biases, behaviors, and perceptions that impact client decision-making and overall financial well-being.

This book, written for practitioners, researchers, and educators, outlines the theory behind many of these areas while also explicitly stating how these related areas directly impact financial planning practice. Additionally, some chapters build an argument based solely upon theory while others will have exclusively practical applications.

Defines an entirely new area of focus within financial planning practice and research: Client Psychology

Serves as the essential reference for financial planners on client psychology

Builds upon and expands the body of knowledge for financial planning

Provides insight regarding the factors that impact client financial decision-making from a multidisciplinary approach

If you're a CFP® professional, researcher, financial advisor, or student pursuing a career in financial planning or financial services, this book deserves a prominent spot on your professional bookshelf.

Trusted by 375,005 students

Access to over 1 million titles for a fair monthly price.

Ben (59) and Colleen (49) Orr are not entirely uncommon clients in the practice of financial planning. While they are entrenched in a successful family business and rewarding careers, they are typical clients with a host of financial challenges, somewhat undefined long- and short-term goals, and a family with complex interpersonal dynamics.

This is the second marriage for both. Ben has three children with his first wife, Nina (58). Nina retained 33% ownership of the private cleaning supplies corporation that she and Ben started 25 years ago and she remains actively involved in company management. Ben and Colleen almost never discuss Nina’s continued involvement in the business and family. Of Ben and Nina’s three children, Mary Jo (34) and Ernest (32) are principals in the family business and both are married and have children of their own. Their 29-year-old son, Jacob, resides in a local community serving adults with developmental disabilities.

Colleen’s first spouse was killed in an automobile accident soon after their second anniversary. With modest life insurance benefits, she completed graduate school and now loves her work as a professor of math education at the state university. She currently has no plans or intentions for retirement. She and Ben married 15 years ago, and have two children, John (14) and Joan (10).

Ben and Colleen are committed to planning for Jacob’s needs for the rest of his life. Ben would like to retire in 7 years and wants to transfer ownership of the company to his adult children Mary Jo and Ernest, but he doesn’t know what Nina wants to do with her interest in the company. Ben has no clear plans for what he may do in retirement. He just knows the work of the company is all-consuming and he needs a change. Ben and Colleen are committed to setting aside some funds in a separate account to help support John and Joan when they attend college and believe they have adequate resources to do so.

Another looming concern for Ben and Colleen is Ben’s 81-year-old father, Jack. Ben lost his mother to cancer 10 years ago. Since that time, Jack has lived alone in a town about an hour’s drive from Ben and Colleen. Ben visits when he can, but makes a point to call and talk with his father at least once a week. Jack is in relatively good health and enjoys several volunteer activities and golfing with friends. Lately, though, Ben has noticed that his father has become more forgetful and he is not sure if what he is seeing is a normal part of aging or the early signs of dementia or Alzheimer’s. Ben worries that his father might forget to pay his bills or become vulnerable to fraud. He knows Jack meets with a financial advisor a few times a year. Ben wonders if he should give his father’s financial advisor a call, to share his concerns and see what she has noticed during client appointments with his dad. Under most objective measures, Ben and Colleen are financially healthy. Not including the value of the cleaning supplies company, their net worth is approximately $2,600,000. This is comprised of approximately $3,000,000 in assets and $400,000 in debt, in the form of a home mortgage and a personal loan taken to grow the business. A recent independent valuation of the business came in just under $9,000,000. The bulk of their financial assets are in conservative, income-driven investments within qualified retirement plans. Ben has never been a fan of financial risk and equity investing. He still talks about the few equity funds he held, and quickly sold, in 2008. He is more comfortable with direct control over his company assets and has never been open to others controlling his money. Most of the retirement assets are Ben’s with Colleen designated as the beneficiary. Colleen considers herself more of a risk taker when it comes to investing and her retirement assets (approximately $110,000) are mostly invested in small cap index funds within her university’s 403(b) plan.

Colleen believes Ben spends too much on travel, company and family celebrations, and charity. She is the primary manager of the family budget and tries to keep their spending on track but has been frustrated lately that their annual rate of saving is almost zero, excluding retirement contributions through the company and the university. They own a four-bedroom home in a neighborhood of homes valued between $250,000 and $300,000. Their mortgage balance is approximately $175,000.

Ben and Colleen believe they have adequate protection against the risk of financial loss, but it has been at least 5 years since they have given insurance coverage significant thought. Both are so busy that the thought of evaluating life, home, automobile, health, disability, umbrella liability, and long-term care options seems overwhelming, yet it is something they know they need to do. Colleen has life insurance through the university with benefits of 2.5 times her $88,000 annual salary. She is not sure who her beneficiaries are for the policy. Ben has a $3,000,000 term life policy connected to the family business, with Nina as the primary beneficiary and their three adult children as secondary beneficiaries. They are covered under a group health plan connected to Colleen’s university and have homeowner and automobile policies but don’t remember the last time they reviewed coverage and costs. Ben and Colleen each drive older, reliable vehicles with no automobile loans. They have a $1,000,000 umbrella liability policy but no disability or long-term care insurance.

Ben and Colleen have simple wills and healthcare power of attorney documents that were drafted 13 years ago, just after the birth of John. In their 15 years of marriage, Ben and Colleen have never committed to working with a financial planner. Ben is hesitant to turn everything over to one person or company. He likes bouncing ideas off his many financial advisors (accountant, attorney, retirement investment advisor, and insurance agent), but prefers to make his own decisions in the end. Colleen is growing increasingly frustrated with the lack of coordination between the finances of the business and their household. She has been suggesting that they use the services of a Certified Financial Planner™ (CFP) for years. They have visited with a few planners for initial consultations, but never made the commitment. Ben and Colleen’s situation is complex: There are not only difficult decisions to make, but the number of decisions is overwhelming.

As you move through the methods of inquiry in this book, keep a case family like the Orrs in mind. Keep asking yourself, “What really guides Ben and Colleen’s decisions? How have these decisions been shaped by both mathematical calculations as well as gut-level intuition? When is it mostly about money, and when is it family relations that matter most? How do clients’ understanding of risk impact the decisions they make? How do the dynamics of marriage and communication patterns impact the formulation of life plans and goals? How do personalities, upbringing, and personal identities influence spending and saving patterns and retirement investment choices? How often and in what ways do clients like Ben and Colleen communicate with one another about their goals and vision for the future, and to what extent should that communication matter to you as their counselor and advisor?

Ben and Colleen are in mid-life, but Ben is a decade older than Colleen. How might the aging process affect their decision-making capacities now and in years to come? Will the age difference matter more or less in later life? At what point might each be at risk of cognitive decline and loss of financial capacity? Since Ben is older, what should Colleen understand about age-related changes in cognition? What makes them, and clients like them, more or less willing to trust your advice?

These are the types of questions this book is attempting to address. By working more systemically and holistically beyond the tenets of optimal resource allocation theory and behavioral finance, we find new approaches to the deeply human questions defining the financial lives of Ben and Colleen. All of these questions require an in-depth analysis of multiple academic disciplines to help better serve Ben, Colleen, and their family that goes beyond the traditional content areas associated with financial planning, such as estate planning, taxation, and investments. This leads us to client psychology.

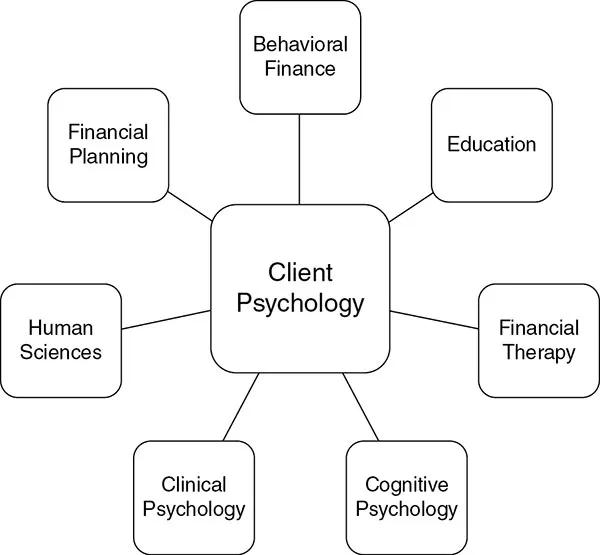

FIGURE 1.1 The Academic Disciplines of Client Psychology

For the purpose of this book, client psychology is defined as the biases, behaviors, and perceptions that impact client decision-making and financial well-being. By anyone’s standards, that is a broad umbrella. However, holistically serving a financial planning client requires a broad approach, taking multiple academic disciplines, research methodologies, and traditions from various programs of study and professions. Biases are our inclinations for or against a certain object or person. Client biases may relate to interpersonal matters and could be based upon one’s past experiences. Behaviors are our responses to a given situation and stimulus, which, in a client context, are more likely to be observable. Perceptions are recognitions of the lived experiences of the individual, the lenses by which they look at the environment around them. Essentially, it is not just what the client does, it is also her perceptions: perceptions of her spouse and family; her motivations; and of herself that impact almost all aspects of her as a client. The first three words of this working definition purposely represent a broad approach to understanding the attitudes and behaviors of the client. Implicit within this broad umbrella are a variety of research methodologies needed to answer many of the questions about our clients, including any combination of quantitative, qualitative, theoretical, experimental, or historical approaches.

Behavioral finance is an important component of our working definition of client psychology and certainly this book. It is a product of cognitive and behavioral psychology within the context of economics and finance to examine why humans, in this case the individual client, make what would appear to be irrational financial decisions when compared to a pure economic or optimization model. Heuristics, or mental shortcuts, are a big cause of these irrational decisions and lead to inherent biases on the part of the individual, particularly when the problem is complex and motivation to think slowly and deliberately is low.

Chapters of this book focus on the foundational elements of behavioral finance, heuristics and biases, prospect theory, mental accounting, choice architecture, and personality and financial behavior. The approach within client psychology is not only to present a theoretical framework for each of these content areas, but also outline the implications of this theory specifically for the field of financial planning and the financial-planning client.

Education is also critical in the field of financial planning, exploring topics such as self-determination theory and self-efficacy, both of which have roots in cognitive psychology but have evolved further in the more practitioner-based profession of education. Self-determination theory focuses on the motivation of the individual with a specific focus on innate psychological needs (Ryan & Deci, 2000). Bandura (1994) defines self-efficacy as “people’s beliefs about their capabilities to produce designated levels of performance that exercise influence over events that affect their lives” (p. 1). Self-efficacy is a focus on the individual’s perception of their own ability to perform a certain task within a specific task setting. A financial planner should have a keen understanding of self-determination theory, as knowing the intrinsic motivation of the client can be a powerful tool in helping keep client behaviors on track and consistent with the client’s long-term financial goals. Self-efficacy and client financial literacy are intertwined. If individuals feel that they have knowledge and aptitude with regard to their own financial decision-making and overall well-being, they are more likely to both seek out a financial planner and stay the course as life challenges intervene.

Financial therapy is a key component to client psychology; as with other aspects of client psychology, it focuses on client behaviors, but from the perspective of the influences of personal relationships. Grounded in the practice and theory of couples and family counseling, financial therapy draws from the relational life of the client. While financial professionals have long acknowledged that advising is a relationship business, the focus has been mainly on the relationship between planner and client. The body of knowledge within the financial therapy discipline continues to grow and has been an integral part of financial planning practice. The inter-relational elements of client decision-making and financial well-being have a powerful impact on the client, with equally powerful implications for advisors working with clients dealing with complex family relationships.

Cognitive psychology focuses on mental processes such as attention, memory, and creativity, and has provided the theoretical underpinning for educational psychology and behavioral finance. The amount of cognitive load that a client, or planner for that matter, uses during the presentation of a financial plan or articulation of goals may have a significant impact on the success of a given client–planner interaction. Similarly, cognitive psychology has a deep impact on the motivations of the individual, which is useful in defining why clients make decisions that enable their long-term financial well-being, or even why they seek a financial planner in the first place. Obviously, behavioral finance topics such as heuristics and biases, anchoring, and mental accounting are greatly influenced by work in cognitive psychology.

Clinical psychology is defined by the American Psychological Association as the “psychological specialty that provides continuing and comprehensive mental and behavioral health care for individuals and families; consultation to agencies and communities; training, education and supervision; and research-based practice” (American Psychological Association, 2017). Within this book, we explore financial psychology, which blends aspects of broader elements of psychology with behavioral finance.

The human sciences add an ecological perspective to the field of fin...

Table of contents

Cover

Title Page

Copyright

Acknowledgments

Preface

About the Contributors

Chapter 1 Client Psychology

Chapter 2 Behavioral Finance

Chapter 3 Understanding Client Behavior: Rational or Irrational?

Chapter 4 Heuristics and Biases

Chapter 5 Decision-Making under Risk

Chapter 6 The Role of Mental Accounting in Household Spending and Investing Decisions

Chapter 7 Intentional Choice Architecture

Chapter 8 Cognition, Distraction, and the Financial Planning Client

Chapter 9 Personality and Financial Behavior

Chapter 10 Risk Literacy

Chapter 11 Automated Decision Aids: Understanding Disuse and Designing for Trust, with Implications for Financial Planning

Chapter 12 Self-Determination Theory and Self-Efficacy in Financial Planning

Chapter 13 Marriage and Family Therapy, Financial Therapy, and Client Psychology

Chapter 14 Client Diversity: Understanding and Leveraging Difference to Enhance Financial Planning Practice

Chapter 15 Client Psychology: The Older Client

Chapter 16 Financial Psychology

Chapter 17 Money Disorders and Other Problematic Financial Behaviors

Chapter 18 Situation Awareness in Financial Planning: Research and Application

Chapter 19 Final Remarks

Index

EULA

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.4M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

Both plans are available with monthly, semester, or annual billing cycles.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go. Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Client Psychology by Charles R. Chaffin in PDF and/or ePUB format, as well as other popular books in Business & Wealth Management. We have over one million books available in our catalogue for you to explore.