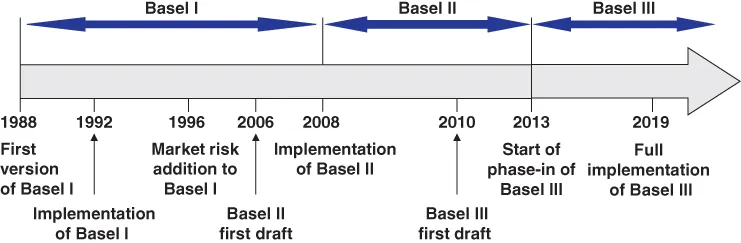

The Handbook of Basel III Capital – Enhancing Bank Capital in Practice delves deep into the principles underpinning the capital dimension of Basel III to provide a more advanced understanding of real-world implementation. Going beyond the simple overview or model, this book merges theory with practice to help practitioners work more effectively within the regulatory framework, and utilise the complex rules to more effectively allocate and enhance capital. A European perspective covers the CRD IV directive and associated guidance, but practitioners across all jurisdictions will find value in the strategic approach to decisions surrounding business lines and assets; an emphasis on analysis urges banks to shed unattractive positions and channel capital toward opportunities that actually fit their risk and return profile. Real-world cases demonstrate successful capital initiatives as models for implementation, and in-depth guidance on Basel III rules equips practitioners to more effectively utilise this complex regulatory treatment.

The specifics of Basel III implementation vary, but the underlying principles are effective around the world. This book expands upon existing guidance to provide a deeper working knowledge of Basel III utility, and the insight to use it effectively.

- Improve asset quality and risk and return profiles

- Adopt a strategic approach to capital allocation

- Compare Basel III implementation varies across jurisdictions

- Examine successful capital enhancement initiatives from around the world

There is a popular misconception about Basel III being extremely conservative and a deterrent to investors seeking attractive returns. In reality, Basel III presents both the opportunity and a framework for banks to improve their assets and enhance overall capital – the key factor is a true, comprehensive understanding of the regulatory mechanisms. The Handbook of Basel III Capital – Enhancing Bank Capital in Practice provides advanced guidance for advanced practitioners, and real-world implementation insight.