Introducing a revolutionary new quantitative approach to hybrid securities valuation and risk management

To an equity trader they are shares. For the trader at the fixed income desk, they are bonds (after all, they pay coupons, so what's the problem?). They are hybrid securities. Neither equity nor debt, they possess characteristics of both, and carry unique risks that cannot be ignored, but are often woefully misunderstood. The first and only book of its kind, The Handbook of Hybrid Securities dispels the many myths and misconceptions about hybrid securities and arms you with a quantitative, practical approach to dealing with them from a valuation and risk management point of view.

Describes a unique, quantitative approach to hybrid valuation and risk management that uses new structural and multi-factor models

Provides strategies for the full range of hybrid asset classes, including convertible bonds, preferreds, trust preferreds, contingent convertibles, bonds labeled "additional Tier 1," and more

Offers an expert review of current regulatory climate regarding hybrids, globally, and explores likely political developments and their potential impact on the hybrid market

The most up-to-date, in-depth book on the subject, this is a valuable working resource for traders, analysts and risk managers, and a indispensable reference for regulators

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

This chapter provides a general introduction to the different categories of hybrid debt and delivers the basic knowledge needed to move deeper into hybrid territory. Hybrid instruments are often misunderstood and hence mismanaged. They are not equity instruments with bond-like risk. Neither are they instruments with bond returns flavored with equity risk. Further, it is also difficult to come up with a standardization when it comes to categorizing hybrid debt. In this introductory chapter we cover the obvious and well-known instruments, such as preferreds and convertible bonds. These are the cornerstones of corporate hybrid debt. The chapter also contains a primer on bail-in capital, contingent convertibles, and financial hybrid debt such as Tier 1 and Tier 2 bonds.

1.2 HYBRID CAPITAL

Hybrid securities are located at the crossroads between debt and equity. This asset class combines properties of common equity and corporate debt. The most outspoken subcategories of hybrid securities are convertible bonds and preference shares (preferreds). Further, in the capital structure of banks and corporates, one can also find quite often hybrid instruments belonging to the category of subordinated debt. These are hybrid bonds and have an equity-like character because of their long (sometimes perpetual) maturity, deep subordination, loss absorption, and the possibility of a coupon deferral. These securities illustrate that the split between debt and equity is a continuum and far from crystal clear. Moody’s, Standard & Poor’s (S&P), and Fitch have each developed their own proprietary methodologies to determine the equity character to be attributed to a hybrid bond. Needless to say, the outcomes sometimes differ very much between these three rating agencies for one and the same bond.

Hybrids have never received the same amount of attention from investors, the financial press, or researchers as the two main stream asset classes – bonds and equity. Investment banks have typically structured their trading operations in fixed-income and equity departments. The first desk covers corporate debt and senior debt, while the second desk takes care of equity trading. Bond and equity trading also has a much larger scope than hybrids. Equity trading is indeed much broader than just buying or selling shares. The equity derivatives market for listed or exotic options is enormous, and has in turn been given a boost with the rise of the structured product market. The same holds for the fixed-income desks, where trading corporate bonds has received support from the advent of the credit default swap (CDS) market. Credit derivatives offer the owners of corporate debt the possibility to buy protection on these securities. According to ISDA, 1 the gross notional amount of all CDS contracts outstanding was $25.9 tn on December 31, 2011. The size of this CDS market is a multiple of the GDP of the United States, which was by contrast $15.6 tn. Hybrids do not have a similar firm link with a vast underlying derivatives market. From this perspective, the hybrid market stands more or less on its own feet.

Companies use a wide spectrum of instruments to finance their balance sheet. Here also, equity and standard corporate debt dwarfed the hybrid bonds. Hybrids remain, without doubt, the smallest component on the average corporate balance sheet. ALCOA, an aluminum producer in the United States, has, for example, a $40 bn balance sheet financed through $17 bn of equity, a $3.7 bn loan, and $12.6 bn in bonds. The hybrid component of the liabilities is rather limited and consists of a $55 mn preferred and a $575 mn convertible bond (Table 1.1).

Table 1.1 ALCOA: Structure of the liabilities on the balance sheet (Q4, 2011). The equity component consists of share capital, retained earnings, and minority interests

Liabilities (mn USD)

Current

6 013

Loans

3 750

Bonds

12 587

Convertible Bonds

575

Preferred

55

Equity

17 140

TOTAL

40 120

Source: Bloomberg.

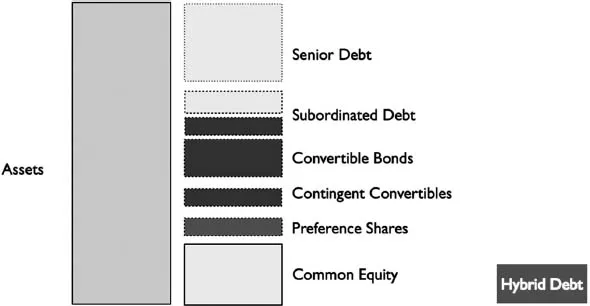

In Figure 1.1, we show an example of a capital structure including a new kid on the block, namely, the contingent convertible or CoCo. This newcomer in the hybrid family is typically issued by a financial institution and contributes to the loss absorbency of the balance sheet. Indeed, in case the regulatory capital of a financial institution fails to meet a predetermined level, these contingent convertibles convert into shares or suffer a write-down. One can consider them as automated measures to swap debt into equity or write down the face value of debt, without causing default.

Figure 1.1 Sample balance sheet of a financial institution.

1.3 PREFERREDS

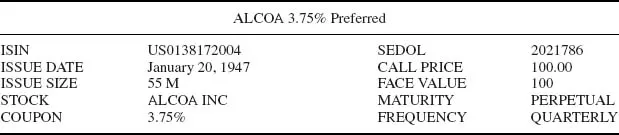

Preferreds are a straightforward mixture between debt and equity. These look at first sight like a combination between equity and bonds. Preferreds offer regular income payments, have no voting rights, and are senior to common stock since they have priority over common equity in dividends payouts. Are preferreds equity investments with bond-like characteristics or should we consider them as bonds with an equity-like behavior? We use the preferred share of ALCOA as a concrete example to develop a possible answer to this question. The ALCOA preferred pays a coupon of 3.75% on a face value of $100. This corresponds to a quarterly payment of $0.9375 every 3 months (January, April, July, and November). A summary of the instrument-specific features of the ALCOA preferred is given in the Table below.

The closing price of the ALCOA preferred on April 20, 2012 was $83.56. We apply a yield measure such as a current yield on the ALCOA bond to compare this preferred security against the bonds of the same issuer. The current yield (CY) is given by:

(1.1)

The current yield indicates the annual income one earns on an investment in this preferred security if everything else remains unchang...

Table of contents

Cover Page

The Handbook of Hybrid Securities

Title Page

Copyright Page

Dedication

Contents

Reading this Book

Acknowledgments

1 Hybrid Assets

2 Convertible Bonds

3 Contingent Convertibles (CoCos)

4 Corporate Hybrids

5 Bail-In Bonds

6 Modeling Hybrids: An Introduction

7 Modeling Hybrids: Stochastic Processes

8 Modeling Hybrids: Risk Neutrality

9 Modeling Hybrids: Advanced Issues

10 Modeling Hybrids: Handling Credit

11 Constant Elasticity of Variance

12 Pricing Contingent Debt

13 Multi-Factor Models for Hybrids

References

Index

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

Both plans are available with monthly, semester, or annual billing cycles.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go. Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access The Handbook of Hybrid Securities by Jan De Spiegeleer,Wim Schoutens,Cynthia Van Hulle in PDF and/or ePUB format, as well as other popular books in Business & Finanza. We have over 1.5 million books available in our catalogue for you to explore.