Traditionally, a market is a place where people go to buy or sell things to meet their needs. Financial markets are very similar except that we find stocks, bonds, and other things. A financial market is a market in which financial assets are traded. In addition to enabling exchange of previously issued financial assets, financial markets facilitate borrowing and lending by facilitating the sale by newly issued financial assets. Examples of financial markets include the New York Stock Exchange (resale of previously issued stock shares), the U.S. government bond market (resale of previously issued bonds), and the U.S. Treasury bills auction (sales of newly issued T-bills). A financial institution is an institution whose primary source of profits is through financial asset transactions. Examples of such financial institutions include discount brokers, banks, insurance companies, and complex multifunction financial institutions.

Traditionally, financial markets serve six basic functions. These functions are briefly listed below:

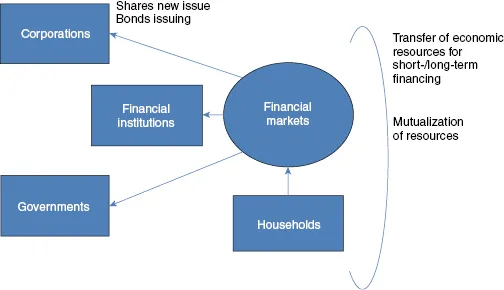

- Borrowing and Lending. Financial markets permit the transfer of funds (purchasing power) from one agent to another for either investment or consumption purposes. Borrowers can be either government or companies. Borrowers are driven by costs when accessing financial markets where Investors (institutional or non-institutional investors) are looking for return and profit. Financial markets bring them together.

- Price Determination. Financial markets provide vehicles by which prices are set both for newly issued financial assets and for the existing stock of financial assets. An asset is any item of value that can be owned. A financial instrument is an asset that represents a legal agreement. There are numerous financial instruments—for example, stocks, bonds, T-bills, personal loans, futures, forwards, options, swaps, and so on. An asset class is a group/classification of financial instruments that share similar characteristics—for example, equity-based assets, debt-based assets, and cash-based assets (money market, etc.).

- Information Aggregation and Coordination. Financial markets act as collectors and aggregators of information about financial asset values and the flow of funds from lenders to borrowers.

- Risk Sharing. Financial markets allow a transfer of risk from those who undertake investments to those who provide funds for those investments.

- Liquidity. Financial markets provide the holders of financial assets with a chance to resell or liquidate these assets.

- Efficiency. Financial markets reduce transaction costs and information costs.

In attempting to characterize the way financial markets operate, one must consider both the various types of financial institutions that participate in such markets and the various ways in which these markets are structured (Figure 1.1). Thus, a financial market is a marketplace in which financial instruments are traded.

There are four admitted primary financial markets, but we will see that there are also other important markets:

- The stock (equities) market

- The bond (fixed-interest) market

- The derivatives market (futures, options, etc.)

- The foreign exchange market

Many companies either occasionally or regularly must raise money for either (a) operations purposes such as covering payroll, adjusting inventory level, or managing any other operating expenses or (b) expansion purposes such as purchasing real estate (land, buildings, factories, etc.), purchasing equipment (e.g., an airline company wants to buy some additional aircrafts), purchasing raw materials, or hiring new employees. How can companies raise money?

In the area of debt financing, a company may borrow some money from an outside source with the promise to repay the principal and interest. Thus they can borrow money either from a bank or from issue such as bonds, bills, or notes. Borrowing money is not necessarily a bad decision, because debt is also a form of leverage and is a common and often cost-effective method of raising money. Corporate balance sheets of all companies, even the healthiest ones, include some level of debt. Another form of corporate financing is equity financing. A company sells a portion of itself to an outside source. Actually, it is selling shares of the company. A share is a unit of ownership in a company. The company decides how many shares to authorize when it incorporates. Usually, some of the authorized shares are issued to the founders, and some shares are retained by the corporation.

Here is an easy example to understand:

Example.

Let's imagine that a new corporation is formed. This corporation authorizes 2,000,000 shares of stock. If the total combined value of the corporation's asset is $200,000, then how much is each share of the company worth? This is not complex to calculate, and the following formula answers that question.

Each of these markets is highly regulated (even if for some individuals they are never enough!). Regulation of the U.S. financial markets is the responsibility of the U.S. Securities and Exchange Commission, the SEC.1

The SEC was formed during the Great Depression after the stock market crash of 1929. It has been created by the Securities Exchange Act of 1934. It is headquartered in Washington, D.C. and currently employs approximately 4000 people. The original purpose if the SEC is to regulate the stock market and prevent corporate abuses relating to the reporting and sale of securities. Trust is the backbone for all financial markets. The SEC was given the power to license and regulate stock exchanges, companies that issue stock, stockbrokers, and dealers.

Currently, the SEC is in charge for overseeing eight major laws that govern the securities industry:

- Securities Act of 1933

- Securities Exchange Act of 1934

- Trust Indenture Act of 1939

- Investment Company Act of 1940

- Investment Advisers Act of 1940

- Sarbanes–Oxley Act of 2002

- Credit Rating Agency Reform Act of 2006

- Dodd–Frank Wall Street Reform and Consumer Protection Act of 2010 as a result of the credit and financial crisis2

The SEC can bring civil enforcement actions against individuals or companies who are alleged to have committed fraud, engaged in insider trading, or violated any other securities law.

In Europe this task is spread among national regulators and a pan-European authority called ESMA.3

1.1 The Money Market

The term money market refers to the network of corporations, financial institutions, professional investors, and governments that deal with the flow of short-term capital. The money market is for transactions up to one year. It is an over-the-counter market. When a professional requires cash for a short period, when a bank wishes to invest money for a while, when a government needs to meet its payroll, and so forth, a short-term liquidity transaction occurs in the money market.

The money markets have expanded significantly in recent years because of the general outflows of money from the banking industry, a process referred to as disintermediation. Financial deregulation has caused banks to lose market share in both deposit gathering and lending. Consequently, market forces rather than regulators determine interest rates. However, it has to be noted that central bank's intervention in short-term rates may have their undoubted impact on the markets.

There are numerous types of short-term instruments apart from plain deposits and loans.

Deposits and Loans.

For deposits and loans, quotes are given with bid4 and offer rates—for example, 3.25–3.35 for a given period, which means that the bank is inviting you to place money at 3.25 less its margin and will allow you to borrow at 3.35 plus its margin.

Periods are standard, and the computation of interest is done on an exact day count basis. The computation of interest is done in the eurozone on a basis of 360 days.

Commercial Paper.

It is a short-term debt obligation of a private-sector company or government-sponsored corporation. In most cases, the paper has a lifetime between 3 and 9 months.

Bankers' Acceptances.

A promissory note is issued by a nonfinancial company to a bank in return for a loan. The bank resells the note in the money market at a discount and guarantees payment. Acceptances usually have a maturity of less than six months.

Treasury Bills (T-Bills).

These are securities with a maturity of one year or less, issued by national governments. Treasury bills issued by an AAA country are generally considered the safest of all possible investment until now. Those securities account for a larger share of the money market trading than any other type of instrument.

Certificate of Deposit (CD).

CDs are negotiable interest-bearing deposits that cannot be withdrawn without penalty before a specific date.

Repurchase Agreements (Repos).

Repos play a critical role in the money markets. A repo is a combination of two transactions. In the first transaction, a security dealer sells securities it owns to an investor, agreeing to repurchase the securities at a specified higher price at a future date. In the second transaction, days or months later, the repo is unwound as the dealer buys back the securities from the investor. The amount the investor lends is less than the market value of the securities in order to ensure that there is sufficient collateral if the value of the securities should fall before the dealer repurchases them. For the investor the repo offers a profitable short-term use for unneeded cash.