A research-based approach to achieving long-term profitability in business

What does it take to guarantee success and profitability over time? Authors Christopher G. Worley, a senior research scientist, Thomas D. Williams, an executive advisor, and Edward E. Lawler III, one of the country's leading management experts, set out to find the answer. In The Agility Factor: Building Adaptable Organizations for Superior Performance the authors reveal the factors that drive long-term profitability based on the practices of successful companies that have consistently outperformed their peers. Of the 234 large companies across 18 industries that were studied, there were few companies that delivered sustained performance across the board. The authors found that across industries, the most successful companies were not the "usual suspects" found in the media, but companies who possessed a quiet agility that allowed them to quickly perceive and respond to changes so that they could continue to grow. Agility gives organizations the ability to adapt to fluctuations in the environment, test possible responses, and implement changes quickly. This book offers specific, research-based case studies to help organizational leaders use agility to achieve sustained profitability and performance while also becoming more adaptable to a changing marketplace.

For executives, leaders, consultants, board members and all those responsible for the long-term health of organizations, this insightful guide outlines:

The components of agility for business organizations

How to successfully build agility within an organization

How agility has its foundation in good management practices

How to use agility to gain a competitive advantage in the marketplace

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

The world breaks everyone…those that will not break, it kills. It kills the very good and the very gentle and the very brave impartially. If you are none of these, you can be sure it will kill you too but there will be no special hurry.

—Ernest Hemingway

The business environment is a merciless place. Before Microsoft, Apple, or Google, there was the Digital Equipment Corporation (DEC). Ken Olsen and Harlan Anderson incorporated DEC in Maynard, Massachusetts, in 1957, the same year that Hewlett-Packard went public. The investment community was so hostile toward computers that Georges Doriot, whose American Research and Development Corporation provided seed capital, suggested they change the originally proposed company name, “Digital Computer Corporation.”

DEC created the minicomputer with its PDP (Programmable Data Processor) family of machines. These interactive computers became mainstays of research departments, engineering laboratories, and academic institutions. Because it sold through original equipment manufacturers (OEMs ) as well as directly, DEC was not burdened with costly application software development and peripheral configuration. In 1970, the PDP-11, DEC's first 16-bit computer, firmly established itself as the market leader. Ironically, it was a crash program in response to Data General's NOVA machine, which had been developed by an engineering team of DEC defectors in 1968. Ultimately, over six hundred thousand PDP-11s of all models were sold. Most, if not all, of the computer engineers who created the PC revolution learned to program on PDP-11s.

In 1978, DEC introduced the 32-bit VAX (Virtual Address eXtension) computer, arguably the most successful minicomputer ever made. By 1990, VAX had propelled DEC to the number two position in the computer industry, behind IBM. That year, its peak, DEC had revenue of $14 billion and employed 120,000 people worldwide.

Eight years later, the Digital Equipment Corporation was gone, acquired by PC maker Compaq at a “discounted” price. In 1977, Ken Olsen had famously derided the emerging personal computer, saying, “There is no reason for any individual to have a computer in his home.” Unfortunately for Olsen, it was the dream of Apple cofounder Steve Wozniak to have a PDP-11 in his home. Digital was late with personal computers, introducing three product lines that were incompatible with each other and with emerging industry standards. They stuck with proprietary architectures and operating systems while the industry moved toward standardization and interoperability. They were slow to adopt UNIX and provide customers with access to its extensive suite of application software.

DEC's product group organization structure went from strength to liability as competition among different subgroups squandered resources and missed market opportunities. Olsen reorganized DEC three times between 1988 and 1991 in increasingly desperate attempts to regain focus and competitiveness. The result was confusion and defection; some of the best and brightest at DEC are now elsewhere, running major technology organizations.

After posting eleven straight profitable years between 1980 and 1990, DEC lost money in five of its last seven years, and Olsen was removed by the board in 1995. When it was acquired by Compaq in 1998, DEC employed 53,500 people, half of its 1990 peak. Four years later, Compaq was acquired by Hewlett-Packard.

Surviving versus Thriving

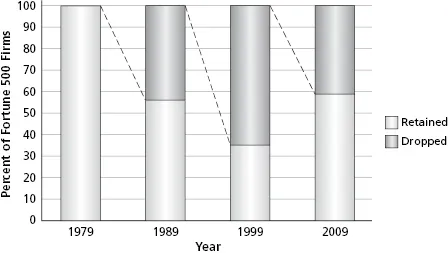

Digital's spectacular rise and fall over a forty-year arc is unusual in the business world. We tend to think of corporations as long-lived entities that span many human generations. Companies such as Ford Motor, Harley-Davidson, DuPont, Siemens, or General Electric have celebrated over a century of existence. But while the experience of these companies is not unique, they are the exceptions, not the rule. Most start-up companies—in fact, most organizations—do not last very long. Recent research suggests that the expected life of a new American company is on the order of six years.1 DEC lasted forty years, although the company that bought it, Compaq, had a total life span of only twenty years. Corporate life, like human life, can be nasty, brutish, and short. As Exhibit 1.1 shows, over the past forty years, about half of the U.S. Fortune 500 fell off the list each decade as companies dissolved, were acquired, or underwent a change of control and ceased to exist as independent going concerns.

Exhibit 1.1. Survival Rates of Fortune 500 Firms

The Old Way of Defining Sustained Performance

Survival is hard enough, but most people—investors and managers in particular—are interested in financial performance. The goal of “maximizing shareholder returns” is usually held up as the primary objective of management. Total shareholder return (TSR) is the preferred performance metric and, in the United States, the S&P 500 stock index is the appropriate benchmark for “the market” (see “Shareholder Returns” sidebar). These financial market measures are “objective,” are difficult to manipulate over anything but the very short term, reflect outside investors' perceptions of value, and have the benefit of being a single measure against which any public firm can be judged.

The data suggest that maximizing shareholder value over the long run is as hard as surviving. No company, for example, has consistently beaten “the market.” As Foster and Kaplan wrote in 2001:

…long-term studies of corporate birth, survival, and death in America clearly show that the corporate equivalent of El Dorado, the golden company that continually performs better than the markets, has never existed. It is a myth. Managing for survival, even among the best and most revered corporations, does not guarantee strong long-term performance for shareholders. In fact, just the opposite is true. In the long run, markets always win.2

Equity markets are subject to fads, irrational exuberance, and panics that have little to do with the quality of the business strategy, management insight, and organization designs that produce profits. Although all industries are subject to the effects of recession, inflation, and social change, the relative performance of industries changes according to their own events and cycles, causing even industry darlings to revert to market means. As a result, stock price and the resultant calculation of shareholder return are inadequate measures of both management effectiveness and sustained performance.3

Shareholder Returns

Finance theory holds that stock prices represent the market's rational expectations for future performance, and shareholder returns are a popular metric for determining absolute or relative performance for publicly traded companies. The rate of total shareholder returns (TSR) for any given time period is calculated as:

Where:

PE is the price per share at the end of the period;

PB is the price per share at the beginning of the period; and

D is dividends per share paid in the period.

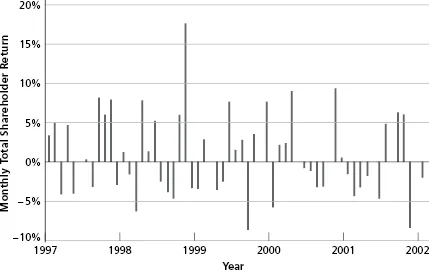

For example, Exhibit 1.2 shows monthly TSR, in percent, for ExxonMobil from May 1997 to June 2002. These returns swing from a high of 17.7 percent to a low of −8.6 percent.

Exhibit 1.2. ExxonMobil Monthly Total Shareholder Returns

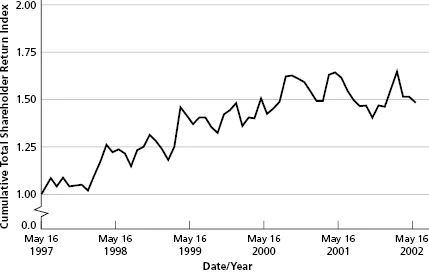

Plotting cumulative TSR provides a way to “see” what is happening to the value of an investment over time. By convention, the plot starts with a value of 1, as in $1 worth of ExxonMobil, and compounds intraperiod returns to create a graphical view of investment growth or decline. Cumulative TSR (CTSR) is given by the formula:

Where:

CTSRt is the cumulative TSR in time period t;

CTSRt−1 is the cumulative TSR in time period t − 1 (the prior period); and

TSRt is the total shareholder return in time period t (as calculated above). The monthly cumulative TSR for ExxonMobil from May 1997 to June 2002 is shown in Exhibit 1.3.

Exhibit 1.3. ExxonMobil Cumulative Total Shareholder Returns

At the end of our example five-year period, in June 2...

Table of contents

Cover

Table of Contents

More praise for The Agility Factor

Series page

Title page

Copyright page

Foreword

Preface

CHAPTER 1: Searching for Sustained Performance

CHAPTER 2: Organizing for Agility

CHAPTER 3: Strategizing and Perceiving

CHAPTER 4: Testing and Implementing

CHAPTER 5: Transforming to Agility

Afterword: Some Reflections on Agility

About the Authors

Acknowledgments

Index

End User License Agreement

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

Both plans are available with monthly, semester, or annual billing cycles.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go. Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access The Agility Factor by Christopher G. Worley,Thomas D. Williams,Edward E. Lawler, III in PDF and/or ePUB format, as well as other popular books in Commerce & Management. We have over 1.5 million books available in our catalogue for you to explore.