A passionate, detailed, quantified argument for state-level tax reform

An Inquiry into the Nature and Causes of the Wealth of States explains why eliminating or lowering tax burdens at the state level leads to economic growth and wealth creation. A passionate argument for tax reform, the book shows that even states with small populations can benefit enormously with the right policies. The authors' detailed exposition evaluates the impact state and local government policies have on a state's relative performance and economic growth overall, backed up with economic data and analysis.

Facts don't lie. But they do point clearly to the failure of so-called progressive tax schemes designed more to curry favor with selected constituencies than to create an economic system that leads to individual wealth as the reward for hard work and entrepreneurial risk taking. An Inquiry into the Nature and Causes of the Wealth of States is a detailed and critical look at income taxation across the nation, and drills down into an analysis of the economic growth or malaise that results from tax policy. Arguing eloquently that a state cannot tax itself into prosperity, just as the impoverished cannot spend themselves into wealth, the authors point out what many inherently know but often fear to say out loud. The book provides detailed quantitative analysis, and discusses the policy variables that can have enormous effects on the financial well-being of states and individual residents, such as:

Personal and corporate income tax rates

Total tax burden as a percentage of personal income

Estate and inheritance taxes

Right-to-work laws

An Inquiry into the Nature and Causes of the Wealth of States shows everyone how to evaluate state-level fiscal and economic policies to become more competitive.

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

CHAPTER 1 The Fall from Grace The Story of States 11 and the Income Tax Adopted

The mark of genuine science is that its explanations take the mystery out of things. Imposture dresses things up to seem more wonderful than they would be without the dress.

—Philip Ball, Curiosity

Foremost among the economic policies available to state and sometimes even local governments is the income tax. Today, 41 out of 50 states collect income taxes on so-called earned income. Of the nine states that have chosen not to tax earned income, two tax what is called unearned income. Thus, there are really only seven states where income of any sort is not taxed at either the state or local level. But this wasn’t always the case.

The Implementation of an Income Tax— A Terrible Mistake

Immediately prior to 1960, there were 19 states where earned income was not taxed and 31 states where it was. Between 1960 and the present, 11 of those 19 states adopted an income tax, and one lone state—Alaska—got rid of its income tax.

The story of the 11 states that adopted an income tax summarizes the object lesson of this book. Here’s their unabridged story:

The 11 states that adopted a state income tax in the past half century encompass a wide cross section of American life, but do not include any states from the South or Far West. As it so happens, there are only three states in the South without an earned income tax—Tennessee, Florida, and Texas—and there are four states in the Far West without income taxes—Nevada, Wyoming, Washington, and Alaska. The other two states without earned income taxes are South Dakota and New Hampshire.

The 11 states that deserted the no-income-tax team are Maine, Rhode Island, Connecticut, New Jersey, Pennsylvania, West Virginia, Ohio, Indiana, Illinois, Michigan, and Nebraska. At the time the income tax was adopted, each of these states believed the economic damage done by the income tax would be minimal and that the increase in public services would be considerable. They were dead wrong!

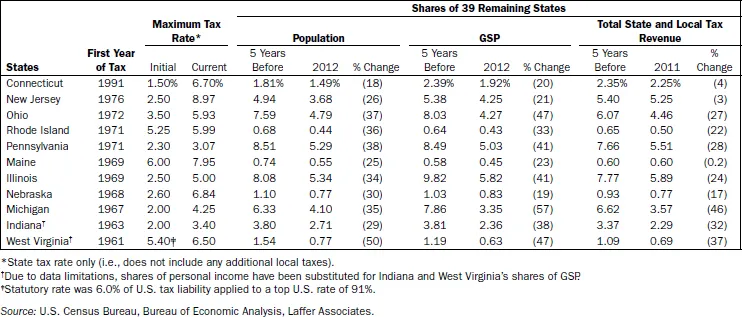

Table 1.1 shows exactly what happened to the primary economic metrics of the 11 states once they adopted an earned income tax. Because these states adopted income taxes in different years, we use the four years preceding the actual implementation of the income tax and the year of implementation itself as their pre–income tax era. We then compare their pre–income tax era to the most recent year’s performance.

Table 1.1 Metrics of the 11 States That Adopted an Income Tax Post-1960 versus the Percentage of 39 Remaining States*

Comparing the 11 states to all 50 states introduces a measurement bias, in that the 11 states are double counted; that is, they would be part of the 11 as well as the 50. A preferable measure, and the one we’ve chosen to use in this chapter for evaluation purposes, is to compare the 11 states that adopted the income tax to the 39 remaining states. While comparing the 11 states to all 50 states creates a bias in the magnitudes, the conclusions would be minimally affected because the directions of change all remain the same. Qualitatively, whether comparing the 11 states to all 50 states or only to the 39 remaining states, the results are basically the same. Quantitatively, they are significantly different.

That Giant Sucking Sound Is People, Output, and Tax Revenue Fleeing Income Taxes

In Table 1.1, we list each of the 11 states that has adopted an income tax over the past 50-plus years and, for each state, the year in which the income tax was adopted, the highest income tax rate when the tax was adopted, the current highest income tax rate, the percentage of each state’s population to the total population of the 39 states in the five years prior to and including the year of adopting the income tax, the percentage of each state’s population to the total of the 39 states in 2012, the percentage of the total of the 39-state gross domestic product (or gross state product [GSP]) for each of the 11 states in the five years preceding and including the adoption year of the income tax, the percentage of total 39-state GSP in 2012 for each of the 11 states, total state and local tax revenues as a share of the total of the 39 states’ state and local taxes in the five years prior to adopting an income tax, and, finally, each state’s share of total 39-state state and local taxes in 2011.1 Pay close attention. The results are dramatic.

Economic Malaise

In terms of population, every single one of the 11 states that introduced the income tax over the past 50-plus years declined in relation to the total of the 39 remaining states. West Virginia, the first state in the modern era to adopt the income tax, reduced its share of the population of the 39 remaining states by a full 50 percent. West Virginia went from a population of 1.83 million in 1961 to 1.86 million in 2012. While no other of the 11 states was able to match West Virginia’s precipitous decline in relative population, each and every one of the 11 states reduced its percentage of the remaining 39 states. Especially hard-hit were the industrial giants Pennsylvania, Ohio, Michigan, and Illinois.

Compared to the 39 remaining states since the inception of the income tax, Pennsylvania’s population has fallen by 38 percent, Ohio’s population by 37 percent, Michigan’s population by 35 percent, and Illinois’s population by 34 percent.

The whole reason for adopting an income tax by each of the 11 states was, of course, to increase tax revenues. But not one state of the 11 experienced a rise in revenues relative to the other 39 states. It makes you wonder just how much consideration the politicians in these 11 states gave to the welfare of their citizens. It’s clear what many of the citizens thought—they left.

In terms of state gross domestic product, each state that introduced an income tax since 1960 has also declined as a share of the 39 remaining states. The differences vary in size, but the change in each state’s GSP relative to the remaining 39 states’ GSP is universally negative. Michigan’s results are especially devastating, with a fall in GSP of 57 percent relative to the 39 remaining states.

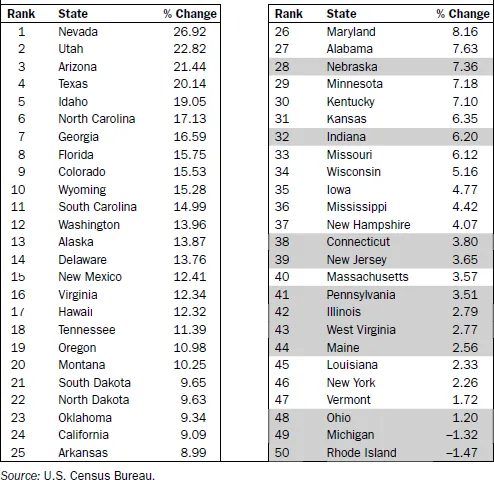

Table 1.2 really says it all when it comes to the economic consequences of adopting an income tax. We have listed all 50 states’ population growth over the past decade from highest to lowest. Just look at the highlighted rankings of those 11 states that have adopted an income tax since 1960. Each of those 11 states is in the bottom half of the U.S. rankings; nine are in the worst 13 states, and three are the worst three states.

Table 1.2 Ten-Year Population Growth by State: Percentage Change, 2002 to 2012 (ranked highest to lowest)

The long-term debilitating consequences of adopting an income tax just keep on getting worse. Like a bad case of poison ivy, the state income tax is the gift that just keeps on giving.

But as dramatic as these results are, they don’t tell the whole story by any means. The human condition is more than just dollars and cents.

Misleading Measures

As if primed to corroborate our earlier admonition to avoid measures such as average income (income per capita), while each of the 11 states declined as a share of the 39 remaining states in both population and income, five of the 11 states experienced increases in income per capita relative to the rest of the nation, and six had declines in income per capita. While each of these 11 states was a loser in the competition of all states, six were bigger losers in changes in GSP than they were in population, and five were bigger losers in changes in population than they were in changes in GSP.

Our critics point to the fact that almost half of the 11 states that adopted an income tax since 1960 had increases in average income (i.e., income per capita relative to the rest of the nation) as proof positive that adopting an income tax has no measureable effect on the prosperity of a state. We know better. They’re all losers!

To see just how far off track so-called experts can be...

Table of contents

Cover

Titlepage

Copyright

Dedication

Prologue

CHAPTER 1: The Fall from Grace

CHAPTER 2: Economic Metrics

CHAPTER 3: The Nine Members of the Fellowship of the Ring to Balance Out the Nine Nazgûl1

CHAPTER 4: Piling On

CHAPTER 5: Give unto Caesar

CHAPTER 6: Why Growth Rates Differ

CHAPTER 7: Fiscal Parasitic Leakages

CHAPTER 8: Au Contraire, Mon Frère

Bibliography

Acknowledgments

About the Authors

Index

End User License Agreement

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

Both plans are available with monthly, semester, or annual billing cycles.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go. Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access An Inquiry into the Nature and Causes of the Wealth of States by Arthur B. Laffer,Stephen Moore,Rex A. Sinquefield,Travis H. Brown,Arthur Laffer in PDF and/or ePUB format, as well as other popular books in Business & Taxation. We have over 1.5 million books available in our catalogue for you to explore.