![]()

Chapter 1

Introduction to Funds

1.1 WHY THIS BOOK?

I have sought to write the manual I always wanted to find on the shelves. In my career as both an asset manager and a legal adviser to asset managers and investors, I have often been asked to recommend a guide that covers the broad ambit of fund and manager structures.

In the world of asset management, knowledge is often assumed, jargon is sometimes opaque and there can be a tendency towards mystification. Frequently, for example, I am asked ‘What is market?’, and certainly one possible answer to that question is that ‘market’ means whatever is investment worthy at that particular moment in time and given the particular investment: following the money has, after all, always been a plausible strategy. However, in these fast changing times where the industry is being required to adapt to survive, it is more crucial than ever to understand the logic behind the structures that have come to dominate this sector.

Broadly, these pages are intended to function as a guide to all things funds and fund managers. Although approached principally from a United Kingdom (UK), United States (US) and European Union (EU) perspective, this book also references other core fund establishment locations, as well as core economic or asset jurisdictions such as China and Japan. The book approaches its subject from a structural, legal, tax and regulatory perspective. It is, however, a guide and not an in-depth review. The latter would require a number of separate volumes. I hope it succeeds in pointing the reader in the right direction.

1.2 ALTERNATIVE ASSETS

I am going to focus principally on funds comprising what are known as alternative assets. ‘Alternative’ as opposed to the mainstream world that is largely composed of listed equities and bonds. The phrase derives from the pension fund term ‘alternative allocation’, which refers to the proportion of a fund’s portfolio that is invested in alternative assets.

This type of fund comprises principally private equity, hedge, venture capital, real estate, energy, infrastructure, credit and related funds. The managers of these funds tend to fall into the category of ‘2 and 20’ managers, where the ‘2’ refers to the annual percentage fee received by management of the cost or value of assets under management and the ‘20’ refers to the percentage of profit to be made by the manager as a percentage of profit for investors as a whole.

A fund is a fluid concept. It can refer to any pooling of capital or assets. Historically, the concept of alternative assets and funds perhaps finds its origins in the age of exploration. At the heart of Christopher Columbus’s expedition to the Americas was an agreement that is an example of financial pooling. Columbus was backed in part by a ‘fund’ from Italian financiers and was able to convince the King of Spain to provide the top-up funding required for the trip. Columbus and his ‘management team’ had their overheads covered and were promised a generous share of performance profits, as well as real management power within any newly discovered lands, the ‘portfolio assets’. Success would also mean prestigious titles and backing for the next ‘fund’. The agreement was in fact quite detailed. Together with any treasure looted, Columbus would receive 10% of revenues reaped from newly discovered lands as well as having a right of first refusal to invest at a discount in any commercial venture deriving from the newly discovered territories – the King of Spain apparently believed that success or indeed Columbus’s return were unlikely investment outcomes. Management and co-investment opportunities rarely come better!

1.3 WHAT IS A FUND?

A fund is a broad term, but as we have seen is used to describe any pooling of assets. These assets may be cash, shares, loans or tangible or intangible assets. A fund can even be a vehicle that holds a single asset (such as Vallar (now Bumi plc) and Vallares (now Genel Energy plc) – both originally special purpose cash shells established by the financier Nathaniel Rothschild to acquire specific companies), although, typically, a fund is established to hold more than one asset.

The term fund can of course be applied to other industries and concepts, for example:

- a fund or ‘stable’ of pop artists, managed by an expert pop promoter, manager or agent. The more stars under management, the greater the diversification

- a fund or ‘library’ of knowledge or

- a fund or ‘team’ of football stars (where the assets are footballers) that are bought and sold.

Almost any economic gathering or pooling may be regarded in terms of a fund. A fund could almost better be defined by describing what does not constitute a fund, such as a single purpose operating company with a small balance sheet, unlike Rothschild’s cash shells referred to above. Typically, a fund would not otherwise include a large single purpose operating company, unless of courses it uses off (or near-off) balance sheet side vehicles underpinned by external capital, a fairly common feature of large energy, real estate and infrastructure companies.

A fund may have one owner, or many owners who subscribe, acquire and sell positions, shares or units. One of the defining features of a fund is that it often has a professional fund manager (usually regulated) that manages and advises the fund.

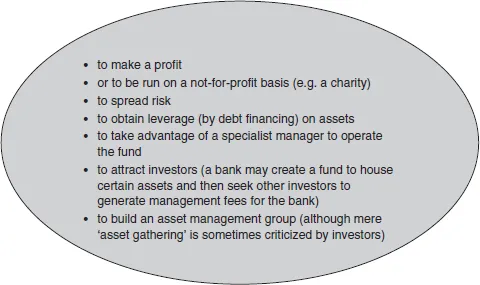

Funds can be operated for a variety of different purposes:

1.4 CATEGORIES OF FUNDS

1.4.1 Ways to categorize

It is clear the term ‘fund’ is a broad one. However, in this book we are considering funds that occur in the investment management or financial services industries. But even within these sectors the range of different types of fund is wide. Investors and managers refer to a ‘hedge fund’ or ‘private equity fund’ or ‘mutual fund’, descriptions which embrace many investment strategies, structures and management arrangements. I would categorize funds within the alternative asset sector using the categories below.

Categorization by industry (by example):

Table 1.1 Categorization by investor returns (or how they get their money back plus a profit)

Drawdown and distribution model

Most private equity funds

The fund ‘draws down’ money from investors when required for investment. Drawing down funds only when required as opposed to in their entirety in advance should have the effect of enhancing the fund’s internal rate of return (IRR) when measured against the date of exit or realization of a particular investment.

On exits, the original cost and the capital gain or profits relating to each asset are then ‘distributed’ to investors and are seldom re-invested. The fund usually has a fixed life, and the intention is to invest and then ‘return’ the entire capital and profits, before winding up the fund. A share of the fund profits (‘carried interest’ or ‘carry’) is distributed to the management team. In a drawdown and distribution model fund, assets remaining after distribution at the end of the life of a fund can be sold on the ‘secondary market’, as can an investor’s position.

Income generated from investments is usually distributed as it arises, for example, net yield from real estate, rental receipts or fixed-income gilts.

The fund is usually ‘closed’ and not ‘open’ (meaning that the number of investors and amount invested are fixed and have a fixed life). | Tradable model

Many retail or tax-driven funds

A tradable fund is one where the shares or units in the fund are traded, usually on a public market. The capital is not distributed to investors although regular and larger one-off dividends can be made. The funds may or may not have a fixed life and gains and profits made within the fund should cause the fund’s share price to increase. However, tradable funds are subject to the ups and downs of trading and:

- illiquidity

- ‘trading at a discount’ to asset value

- market, economy or investor sentiment.

What this often leads to is a tradable fund trading at a premium to embedded value at moments of investor exhilaration, but at a discount the rest of the time. Sentiment or recognition can bear little correlation to actual asset value. | NAV or redemption model

Most hedge funds

This fund redeems or prepays units held by investors in the fund and on (or within a defined time of) redemption also pays investors any profit ‘attaching’ to those units. A share of the profits is paid as a performance fee to the fund’s management team. Units are often redeemed at, or correlated to, the net asset value (NAV) of that unit. A unit’s NAV is the total of the fund’s gross assets, less leverage and liabilities, divided by the number of units in the fund. It is typically the manager or administrator and also third party valuers that calculate NAV. The fund is usually ‘open’ and not ‘closed’ (meaning the number of investors and amount invested fluctuate as investor commitments are made and redeemed) and can exist for an undetermined period of time, unless the fund is wound up. |

Categorization by investment strategy (by example):

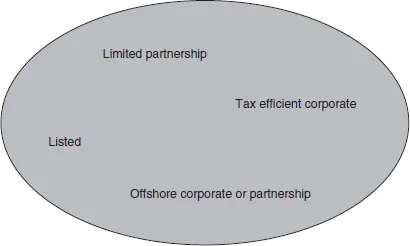

Categorization by vehicle:

1.5 CHOOSING A VEHICLE

Choosing the correct vehicle for a particular fund will depend on a number of factors. Some to consider are:

- the vehicle that is most tax efficient for the target investor base and for the fund’s management team (taking into account the fund’s likely asset...