"During a time of tremendous change and uncertainty, Healthcare Disrupted gives executives a framework and language to determine how they will evolve their products, services, and strategies to flourish in a increasingly value-based healthcare system. Using a powerful mix of real world examples and unanswered questions, Elton and O'Riordan lead you to see that 'no action' is not an option—and push you to answer the most important question: 'What is your role in this digitally driven change and how can your firm can gain competitive advantage and lead?'"—David Epstein, Division Head, Novartis Pharmaceuticals

"Healthcare Disrupted is an inspirational call-to-action for everyone associated with healthcare, especially the innovators who will develop the next generation of therapeutics, diagnostics, and devices."—Bob Horvitz, Ph.D., David H. Koch Professor of Biology, MIT; Nobel Prize in Physiology or Medicine

"In a time of dizzying change across all fronts: from biology, to delivery, to the use of big data, Health Disrupted captures the impact of these forces and thoughtfully develops new approaches to value creation in the healthcare industry. A must-read for those who strive to capitalize on change and reinvent the industry."—Deborah Dunsire, M.D., president and CEO, FORUM Pharmaceuticals

Healthcare at a Crossroad: Seismic Shifts, New Business Models for Success

Healthcare Disrupted is an in-depth look at the disruptive forces driving change in the the healthcare industry and provides guide for defining new operating and business models in response to these profound changes.

Based on original research conducted by Accenture and years of experience working with the most successful companies in the industry, healthcare experts Jeff Elton and Anne O'Riordan provide an informed, insightful view of the state of the industry, what's to come, and new emerging business models for life sciences companies play a different role from the past in to driving superior outcomes for patients and playing a bigger role in creating greater value for healthcare overall. Their book explains how critical global healthcare trends are challenging legacy strategies and business models, and examines why historical leaders in the industy must evolve, to stay relevant and compete with new entrants.

Healthcare Disrupted captures this pivotal point in time to give executives and senior managers across pharmaceutical, biopharmaceutical, medical device, medical diagnostics, digital technology, and health services companies an opportunity to step back and consider the changing landscape. This book gives companies options for how to adapt and stay relevant and outlines four new business models that can drive sustainable growth and performance. It demonstrates how real-world data (from Electronic Medical Records, health wearables, Internet of Things, digital media, social media, and other sources) is combining with scalable technologies and advanced analytics to fundamentally change how and where healthcare is delivered, bridging to the health of populations, and broadening the resposibility for both. It reveals how this shift in healthcare delivery will significantly improve patient outcomes and the value health systems realize.

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Chapter 1 Why and How the Healthcare Industry is Changing So Rapidly The collective throw-weight of socio-economic and policy changes, technological advances, and structural shifts has primed the healthcare industry for upheaval and disruption—and presented an incredible opportunity to advance the standard of care worldwide.

Over the past several decades, as the healthcare industry (including providers, payers, life science companies, health services companies, and other ancillary businesses) has grown in size and complexity, choices regarding patient care have often become entangled in a myriad of objectives and controls. To survive and thrive, healthcare-related companies and organizations have focused increasingly on individual objectives—the products companies on product sales, the healthcare delivery organizations on providing services at the right price point, the payers on actuarial modeling. And somewhere in the mix, the common goal of achieving the best outcomes for the patient and overall value for the healthcare system was diminished.

But that's all changing. There have been periods throughout economic history where a confluence of policy, technological, and industry structural changes has created a foundation for upheaval and disruption—times where opportunistic strategies have offered handsome near-term rewards, where new entrants have had the potential to be the better operators, and where consolidations and integrated approaches have created unprecedented opportunities. Healthcare is in one of those periods now. And in 10 to 15 years, it will function fundamentally differently than it currently does. Value, defined anew, will increasingly be the metric that matters as healthcare pivots back to the patient in extraordinarily new and different ways.

The world changed, and healthcare—broadly speaking—did not. Like all good catalytic circumstances, this one offers to healthcare the opportunity to leapfrog and make fundamental and sweeping changes that will sustain for years to come. As a result, many of us who work in, with, and around the industry now find ourselves simultaneously playing catch-up and looking forward with a new sense of responsibility to ensure that those without care can access it, to build strength into our national health systems, and to see that healthcare truly re-emerges as patient-responsive, responsible, and centric. We're directly confronting the companies and business models we've built or built upon, and we're defining what worked, what did not work, and what will work in the future. We are also comparing where healthcare stands relative to other industries that have transformed themselves in recent years.

But we're doing all of this under increasing pressure.

The global population is expected to increase by 1 billion by 2025. By then, more than 500 million people will be over the age of 50. Projections from a variety of sources (including the United Nations and the World Health Organization) report that by that same year, 70 percent of all illnesses will be chronic diseases. Overall we are living longer, living with an increasing amount of chronic and comorbid illnesses, and doing so regardless of what country or region of the world we are living in.

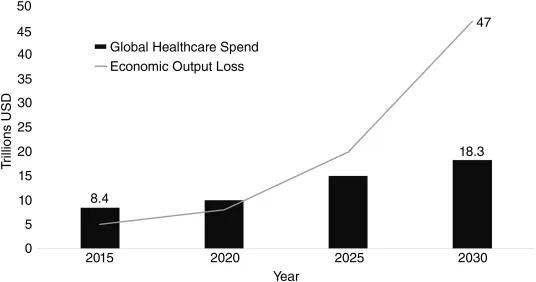

We're also spending more money. In developed countries such as the United States and Germany, where the aging workforce is a key driver of rising healthcare costs, spending on healthcare ranges from 11 to 18 percent of gross domestic product (GDP). In recently developed countries such as China and Brazil, it is between 5 and 10 percent. Overall healthcare spending will be doubling from an aggregate $8.4 trillion in 2015 to $18.3 trillion in 2030 with an estimated lost productivity from chronic diseases alone of $47 trillion over the same period. As Figure 1.1 shows, all of the world's major healthcare systems face enormous cost pressures and potential productivity losses.

Figure 1.1 Global Healthcare Spend and Value of Lost Output Opportunities

Source: WHO Global Health Data Repository, World Healthcare Outlook, Economist Intelligence Unit; http://www.eiu.com/industry/Healthcare and http://apps.who.int/gho/data/node.main.

Opportunities

We may be behind the curve and facing unprecedented challenges, but there are also considerable forces pushing us forward.

One piece of good news is that concurrent with (and perhaps as a result of) aging populations and the prevalence of chronic disease, many markets have seen a significant rise in “health consciousness,” which is framing new opportunities for companies to develop (and do very well selling) entire lines of consumer goods and services that facilitate health and wellness.

These offerings increasingly leverage disruptive digital forces that are a key enabler of the changes we are witnessing. Some of them, for example, built into wearable technologies (e.g., watches and activity monitors) and even mobile phones offer customers unprecedented capability to track and store health data. And so the manufacturers of these devices and their digital ecosystems (e.g., app stores) are thus increasingly bringing the healthcare system right to patients—changing the nature of how the healthcare system understands and interacts with patients, and making healthcare look more and more like a consumer market.

Other digital data—from electronic medical records (EMRs) and personalized genomic information, to lifestyle and personal health data—along with the ability to analyze that data, represent another revolutionary force driving unprecedented insights and facilitating scientific breakthroughs in the development of new drugs and therapeutic services.

Healthcare is relatively nascent in its ability to use these data, whereas consumer markets, financial services, and other areas are highly advanced. But that imbalance itself is revealing pockets of opportunity. While external macroeconomic and demographic trends shape the healthcare environment, internal market forces are taking advantage of these trends to change every aspect of how the healthcare market operates and serves patients.

The Signs of Change

Disruptive indicators lead the way in all major marketplace changes, and we're seeing them now in healthcare. For example:

An unprecedented number of mergers and acquisitions (M&A) have taken place recently in the pharmaceutical and medical device fields. In 2014 alone in those fields, there was $438 billion worth of M&A activity.1 A similar trend is evident among payers. Traditional private health insurers are increasingly aware of their own modest scale; in the United States even the largest private health insurers cover only 10 to 15 percent of prospective individuals, a small proportion by any industrial standards. This awareness is driving meta-scale combinations, which will in turn accelerate the pace of healthcare innovation through applications of large-scale, real-world health claims data sets.2,3

New business models are emerging, and they're breaking old boundaries. Traditionally, there were three distinct types of healthcare players: health providers (delivering treatment and services), health manufacturers (pharmaceutical and medical device companies), and health payers (insurers). However, the traditional lines of distinction among different types of companies are blurring. Device companies are transforming into service entities, providing catheterization lab management services and focusing on the remote management of specific patient populations. Pharmaceutical companies are focusing on service. Providers are extending services beyond their traditional regimens into home care and post-discharge monitoring. Additionally, we're seeing new types of collaborative pairings—medical device companies with pharmaceutical firms, digital technology companies with pharmaceutical firms, payers with providers, payers with digital technology companies, and so forth, for example, Novartis co-investing with Qualcomm, or Humana's acquisition of Concentra.4

New players are making noise and resetting expectations of what's possible. Chief among these are influential consumer digital technology companies that bring new capabilities to the table and offer new forms of partnership. Apple Inc., for example, has launched an app that provides a network for the sharing of health information between its vast consumer base and researchers interested in large-scale data sets.5 Additionally, Google Inc.'s partnership with AbbVie Inc. promises to yield $1.5 billion in research activity around developing solutions for age-related illnesses.6

And all of these changes are taking place against a backdrop of full-fledged industry reform.

A Closer Look at Healthcare Reform

Admittedly, w...

Table of contents

Cover

Title Page

Copyright

Preface

Acknowledgments

Introduction

Part I: The Tsunami of Change

Part II: From Strategy to Value with New Business Models

Part III: Building New Organizations

Part IV: Looking Back—Looking Forward

Glossary

About the Authors

Index

End User License Agreement

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

Both plans are available with monthly, semester, or annual billing cycles.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go. Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Healthcare Disrupted by Jeff Elton,Anne O'Riordan in PDF and/or ePUB format, as well as other popular books in Business & Insurance. We have over 1.5 million books available in our catalogue for you to explore.