CHAPTER 1

A Multicentennial View of Trend Following

Cut short your losses, and let your profits run on.

—David Ricardo, legendary political economist

Source: The Great Metropolis, 1838

Trend following is one of the classic investment styles. This chapter tells the tale of trend following throughout the centuries. Before delving into the highly detailed analysis in subsequent chapters, it is interesting to discuss the paradigm of trend following from a qualitative historical perspective. Although data-intensive, this approach is by no means a bulletproof rigorous academic exercise. As with any long-term historical study, this analysis is fraught with assumptions, questions of data reliability, and other biases. Despite all of these concerns, history shapes our perspectives; history is arguably highly subjective, yet it provides contextual relevance.

This chapter examines a simple characterization of trend following using roughly 800 years of financial data. Despite this rather naive characterization and albeit crude set of financial data throughout the centuries, the performance of “cutting your losses, and letting your profits run on” is robust enough to garner our attention. The goal of this chapter is not to quote t-statistics and make resolute assumptions based on historical data. The goal is to ask the question of whether the legendary David Ricardo, the famous turtle traders, and many successful trend followers throughout history are simply a matter of overembellished folklore or whether they may have had a point.

In recent times, trend following has garnered substantial attention for deftly performing during a period of extreme market distress. Trend following managers boasted returns of 15 to 80 percent during the abysmal period following the credit crisis and infamous Lehmann debacle. Many have wondered if this performance is simply a fluke or if the strategy would have performed so well in other difficult periods in markets. For example, how would a trend follower have performed during past crises like those experienced in the Great Depression, the 1600s, or even the 1200s?

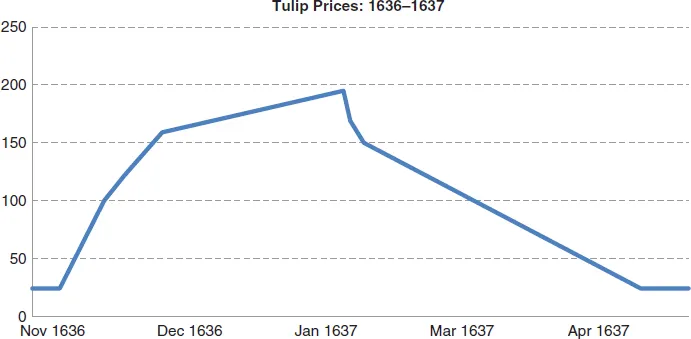

Given that this chapter engages in a historical discussion of trend following, it seems only fitting to begin with a rather controversial and relatively spectacular historical event, the Dutch Tulip Bubble of the early 1600s. Historical prices for tulips are plotted in Figure 1.1. One common type of trend following strategy is a channel breakout strategy. A channel breakout signal takes a long (short) position when a signal breaks out of a certain upper (lower) boundary for a range of values. Using a simple channel breakout signal,1 a trend following investor might have entered a long position before November 25th, 1636 and would have exited the trade (by selling tulip bulbs and eventually short selling if that was even possible) around February 9th, 1637. A trend following investor simply “follows the trend” and cuts losses when the trend seems to disappear. In the case of tulips, a trend following investor might have ridden the bubble upward and sold when prices started to fall. This approach would have led to a sizeable return rather than a handful of flower bulbs and economic ruin. Although it is one rather esoteric example, the tulip bulb example demonstrates that there may be something robust or fundamental about the performance of a dynamic strategy like trend following over the long run. It is important to note that in this example, as in most financial markets, the exit decision seems to be more important than the entry. The importance of cutting your losses and taking profits seems to drive performance. This is a concept that is revisited often throughout the course of this book.

Trend following strategies adapt with financial markets. They find opportunities when market prices create trends due to many fundamental, technical, and behavioral reasons. As a group, trend followers profit from market divergence, riding trends in market prices, and cutting their losses across markets. Examples of drivers that may create trends in markets include risk transfer (or economic rents being transferred from hedgers to speculators), the process of information dissemination, and behavioral biases (euphoria, panic, etc.). Despite the wide range of explanations, the underlying reasons behind market divergence are of little consequence to a trend follower. They seek simply to be there when opportunity arises. Throughout history, opportunities do arise. The robust performance of trend following over the past 800 years helps to historically motivate this point.2

■ The Tale of Trend Following: A Historical Study

Although almost two centuries have passed since the advice of legendary political economist David Ricardo, the same core principles of trend following have garnered significant attention in modern times. Using a unique dataset dating back roughly 800 years, the performance of trend following can be examined across a wide array of economic environments documenting low correlation with traditional asset classes, positive skewness, and robust performance during crisis periods.3

The performance of trend following has been discussed extensively in the applied and academic literature (see Moskowitz, Ooi, and Pedersen 2012).4 Despite this, most of the data series that are examined are typically limited to actual track records over several decades or futures/cash data from the past century. In this chapter, an 800-year dataset is examined to extend and confirm previous studies.5 To examine trend following over the long haul, monthly returns of 84 markets in equity, fixed i...