Financialization of the economy and income inequality in selected OIC and OECD countries

The role of institutional factors

Fatima Muhammad Abdulkarim, Abbas Mirakhor, Baharom Abdul Hamid

This is a test

This is a test

Buch teilen

127 Seiten

English

ePUB (handyfreundlich)

Über iOS und Android verfügbar

eBook - ePub

Financialization of the economy and income inequality in selected OIC and OECD countries

The role of institutional factors

Fatima Muhammad Abdulkarim, Abbas Mirakhor, Baharom Abdul Hamid

Angaben zum Buch

Buchvorschau

Inhaltsverzeichnis

Quellenangaben

Über dieses Buch

Income inequality is a serious problem confronting not only the developed world but also developing countries. Recently, financialization has been one of the culprits identified in literature as one of the cause of income inequality. This book offers the only detailed presentation of the how financialization aided the spread of income inequality in Organization of Islamic Cooperation, OIC countries. Finance has taking a center stage in the affairs of most developing economies, surpassing the real sector of the economy. The result is the creation of an indebted society in which people are comfortable with financing their financial needs through credit. This creates a debt laden society that is trapped in the cycle of debt.

This book represents a comprehensive and indispensable source for students, practitioners and the general public at large. It presents data which shows the buildup of debt and the rising income inequality in Muslim countries. It includes discussion of the rise in rentier income, financialization of everyday life, decline in physical capital accumulation and deregulation of the financial sector. The book therefore, proffers solutions on how Muslim countries can come out of the present economic problem facing them. The promotion and adoption of Islamic principles, which promotes risk sharing based contracts as against debt based transaction is the way to go. When financial contracts are based on the principles of risk sharing, any gains from economic activities get to be shared equitably. Hence, not only capital owners get to enjoy the benefit from the income derived from investments, but rather, all parties that partake in the contract.

Distinguished by its clarity and readability as it is written in a very easy to understand language, it is an important reference work for any concerned individual interested on the recent causes of income inequality in Muslim World.

Häufig gestellte Fragen

Wie kann ich mein Abo kündigen?

Gehe einfach zum Kontobereich in den Einstellungen und klicke auf „Abo kündigen“ – ganz einfach. Nachdem du gekündigt hast, bleibt deine Mitgliedschaft für den verbleibenden Abozeitraum, den du bereits bezahlt hast, aktiv. Mehr Informationen hier.

(Wie) Kann ich Bücher herunterladen?

Derzeit stehen all unsere auf Mobilgeräte reagierenden ePub-Bücher zum Download über die App zur Verfügung. Die meisten unserer PDFs stehen ebenfalls zum Download bereit; wir arbeiten daran, auch die übrigen PDFs zum Download anzubieten, bei denen dies aktuell noch nicht möglich ist. Weitere Informationen hier.

Welcher Unterschied besteht bei den Preisen zwischen den Aboplänen?

Mit beiden Aboplänen erhältst du vollen Zugang zur Bibliothek und allen Funktionen von Perlego. Die einzigen Unterschiede bestehen im Preis und dem Abozeitraum: Mit dem Jahresabo sparst du auf 12 Monate gerechnet im Vergleich zum Monatsabo rund 30 %.

Was ist Perlego?

Wir sind ein Online-Abodienst für Lehrbücher, bei dem du für weniger als den Preis eines einzelnen Buches pro Monat Zugang zu einer ganzen Online-Bibliothek erhältst. Mit über 1 Million Büchern zu über 1.000 verschiedenen Themen haben wir bestimmt alles, was du brauchst! Weitere Informationen hier.

Unterstützt Perlego Text-zu-Sprache?

Achte auf das Symbol zum Vorlesen in deinem nächsten Buch, um zu sehen, ob du es dir auch anhören kannst. Bei diesem Tool wird dir Text laut vorgelesen, wobei der Text beim Vorlesen auch grafisch hervorgehoben wird. Du kannst das Vorlesen jederzeit anhalten, beschleunigen und verlangsamen. Weitere Informationen hier.

Ist Financialization of the economy and income inequality in selected OIC and OECD countries als Online-PDF/ePub verfügbar?

Ja, du hast Zugang zu Financialization of the economy and income inequality in selected OIC and OECD countries von Fatima Muhammad Abdulkarim, Abbas Mirakhor, Baharom Abdul Hamid im PDF- und/oder ePub-Format sowie zu anderen beliebten Büchern aus Business & Finance. Aus unserem Katalog stehen dir über 1 Million Bücher zur Verfügung.

Throughout the world, the income gap between the rich and the poor continues to widen. This disparity in income has become more obvious in the last two decades as the income of the vast majority of the world’s population has been somewhat stagnant over time, while small segments of the population have experienced an upward trend in income. In a recent report by (Oxfam 2016),1 it was reported that income inequality is spiraling out of control and this is a dangerous trend that poses a significant threat to the global sustainability. Similarly, in 2015, income equality was ranked as the most pressing issue confronting the global economy by the World Economic Forum (WEF, 2015), surpassing the previous year’s ranking (when it was ranked 2nd). In a similar vein, in the same year, Credit Suisse estimated that the top one percent of the global population accounts for 48 percent of global wealth, while 50 percent of the world’s population holds only one percent of the global wealth.2 These reports highlight income inequality as a serious problem confronting almost every global economy. Income inequality is defined as a situation where the wealth of the country is distributed unequally among individuals within a group, or among groups in a population or among countries (SESRIC, 2015).

Income inequality is a serious problem facing the world today. This is due to the fact that extreme inequality gives rise to resentments that can result in serious economic, social and political upheavals. This is demonstrated by several events that happened in the last decade; ranging from the Occupy Wall Street movement of the United States, to the recent Arab uprisings – all of these are thought to be the result of economic inequality that exists between the rich and the poor and failure to address these issues will result in disastrous consequences.

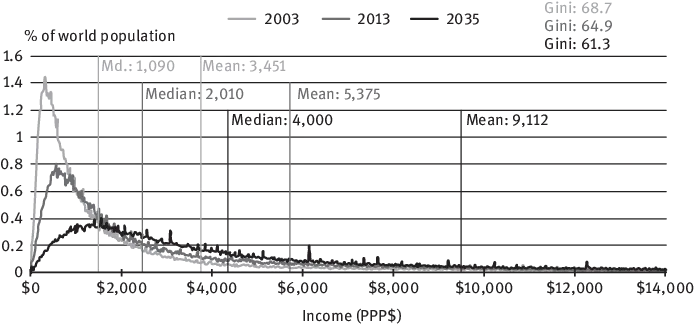

There is no doubt that inequality differs considerably between developed and developing countries, with the latter being more unequal than the former. The rising trend in income started since the 1980s in both developed and developing countries and these phenomena became more widespread in the early 2000s. Even countries that were known to be equal are now affected (Abdul Khalid, 2014). According to Atkinson et al. (2011), extreme inequality is a result of income concentration at the top since this group of people makes the majority of domestic investment, thus the gains realized from these investments are pocketed by capital owners, further worsening income distribution. Fig. 1 depicts the global distribution of income.

Source: Chris Weller, 2015.

Fig. 1: Global Income Distribution.

Although inequality is more prevalent in developed countries such as the United States, it also exists in Muslim countries under the Organization for Islamic Cooperation umbrella – henceforth known as OIC countries.3 These countries have, in the last two decades, witnessed increasing income inequality between the haves and the have-nots. This trend is alarming as it threatens the social and economic stability of these countries. Although the selected OIC countries4 in this study have realized positive economic growth, this growth has led to significant income inequality. This gap is more pronounced in countries like Malaysia, Pakistan, Indonesia and Turkey. For example, the gap between the rich and the poor in Turkey is rising at an alarming rate with 78 percent of the total wealth in the country held by 10 percent of the population, (Zaman, 2014). Against this backdrop, the high degree of income inequality and high poverty rate in most of the OIC countries are the reasons why poverty reduction in these countries are slow despite the anti-poverty reduction programs in place.5

In the same vein, developed countries such as the Organization for Economic Co-operation and Development (henceforth OECD),6 have witnessed a persistent rise in income inequality. In fact, due to the severity of this problem, these countries are aggressively seeking ways to curtail this threat and several policies7 have been proposed to solve this problem. Some of the factors that have contributed to this rise include, but are not limited to, financial deregulation, financial integration, increase income share for capital going to the rich segment of the population and technological change (OECD, 2011).

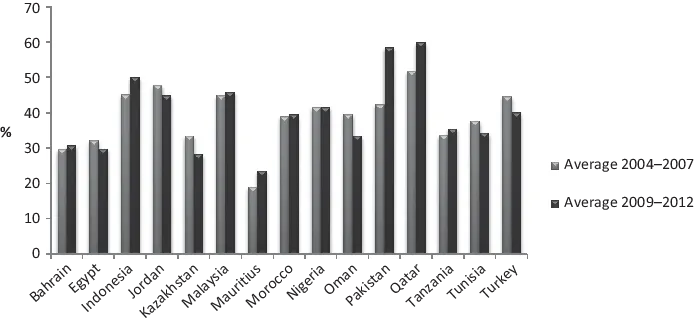

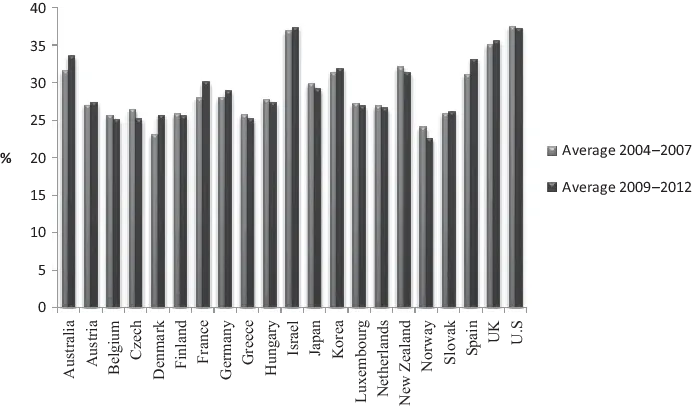

The GINI coefficient is a standard measure of income inequality which ranges from 0 (when everybody receives equal income) to 1 (when only one person receives the entire income of a country). Based on Fig. 2, the GINI coefficient was 0.4 on average between 2004 and 2007 in OIC countries. However, a cursory glance at Fig. 2 suggests that by late 2008, income inequality had risen significantly by almost 18 percent to 0.58 in countries like Pakistan, Qatar and Nigeria. Similarly, in OECD countries (Fig. 3) the GINI coefficient increased by more than 5% in countries like Australia, Israel, United States, Germany and Sweden. This implies that income inequality is increasing at an alarming rate.

Source: Authors calculations.

Fig. 2: Average GINI Coefficient for OIC countries between 2004–2007 vs 2009–2012.

Source: Authors calculations.

Fig. 3: Average GINI Coefficient for OECD countries between 2004–2007 and 2009–2012.

Researchers in the field of finance and economics have identified numerous causes of increased inequality. The most commonly cited factors are: globalization (Majeed, 2015; Asteriou et al., 2014), openness to trade (Franco and Gerussi, 2013; Tiwari Kumar et al., 2013; Jalil, 2012), declining union power (Dierk, 2014; Tomaskovic-Devey and Lin, 2011), rising compensation of top management (Alvaredo et al., 2013; Atkinson et al., 2011) and the nature of the international monetary system8 (Reyes, 2016). Recently, there is evidence to believe that increased income inequality is a result of the financialization of the economy. This is evidenced by growing research that observes the link between financialization and inequality (Kwon and Roberts 2015; Lin and Tomaskovic-Devey, 2013; Dunhaupt, 2012; Volscho and Kelly, 2012; Nau, 2011 and Palley, 2007).

Before going into detail about financialization, it is important to highlight what gives rise to financialization. Firstly, financialization is a result of the increasing role of finance in our daily lives. Finance is simply defined as a science that relates to money and markets.9 Most frequently, the term is used to designate inter-temporal exchanges that give rise to some form of debt and credit with regard to lending and borrowing to someone else (Hendrik, n.d.). Finance is not without its benefit as it provides available funds to those in need to carry out projects that would have otherwise been impossible to achieve. However, this is done at a cost as most of the facilities are granted based on fixed-term contracts (debt contract) that guarantees fixed returns without considering the outcome of the projects. Debt produces something that could be used in place of money which has some store of value characteristics, and since debt could be used in exchange for real assets, it consequently serves as a medium of inter-temporal exchange. Therefore, the main component of financialization is debt creation which tends to resonate throughout the modern capitalist economy.

This leads us to define the concept of financialization that has in the last two decades gained wide usage in social sciences to refer to a wide range of evolution that took place in modern capitalist economies. Numerous authors have used the term widely, including Tomaskovic-Devey et al. (2015), Palley (2007), Epstein (2005)Stockhammer (2004). Financialization is defined on two different levels namely: general definitions which cover broader macroeconomic aspects of the economy and a narrower definition which is more industry specific. The general definition covers a broader area, the most widely cited definition of financialization is the definition by Epstein (2005,) as “the increasing role of financial motives, financial markets, financial actor and financial institutions in the operation of domestic and international economy”. Other authors however provided a narrower definition and define financialization as the innovation and expansion of the financial industry (Orhangazi, 2008a), or increased profit accumulation from the financial sector rather than the real sector (Krippner, 2005; Stockhammer, 2004). The narrower definition of financialization is transformation in corporate governance to a more shareholder value-maximization orientation (Froud et al., 2000). Similarly, Orhangazi (2008b) defines financialization as the evolution in the way non-financial corporations (NFCs) and financial markets interact with one another.

Notwithstanding its definition, financialization encapsulates some common themes: dominance of financial activities over real sector activities, increased income derived from financial transactions and growing participation of NFCs in the realm of financial activities. For the purpose of this research, the definition of financialization covers the macroeconomic aspect of the economy and it is used for analysis in this study. Financialization is thus defined as the disproportionate growth of the financial sector compared to GDP through rapid growth of debt and large increases in financial sector profits.

Financialization is said to come to being due to the high inflationary environment that prevailed in the late 1970s following the abandonment of the Bretton Woods system.10 The breakdown of the Bretton Woods system heightened inflationary pressures of the late seventies resulting in the collapse of the dollar and the subsequent retaliation by the Organization of Petroleum Countries (OPEC) through oil price hikes, resulting in a host of embargoes which in turn heightened inflationary pressure. As a policy response to this, interest rates rose sharply (popularly known as the Volker Shock), paving the way for financialization. These developments brought drastic changes to the international economic system and altered the behavior of economic authorities which tend to favor price stability, competitiveness and financial liberalization with severe consequences. This also threatened financial stability, leading to increased unemployment and worsening inequality (Reyes, 2016).

Financialization can exist in both domestic and international markets. In the context of the domestic financial market, financialization comes about as a result of a shift from a regulated finance industry that existed in the late 1970s to a more relaxed one, where the distinction between various financial institutions have become blurred11 (Askari and Mirakhor 2015). This is followed by the snowballing inclusion of NFCs in financial markets and their increased involvement in both financial and non-bank financial intermediaries -such as hedge funds, insurance companies, and mutual funds – in the financial markets. In addition, the NFCs have remodeled their investment strategy from the traditional “reinvest and distribute” model to a “downsize and distribute” model (Riccetti and Gallegati, 2016; Crotty, 2005). The flourishing of the domestic stoc...