The Crypto Market Ecosystem has emerged as the most profound application of blockchain technology in finance. This textbook adopts an integrated approach, linking traditional functions of the current financial system (payments, traded assets, fundraising, regulation) with the respective functions in the crypto market, in order to facilitate the reader in their understanding of how this new ecosystem works.

The book walks the reader through the main features of the blockchain technology, the definitions, classifications, and distinct characteristics of cryptocurrencies and tokens, how these are evaluated, how funds are raised in the cryptocurrency ecosystem (ICOs), and what the main regulatory approaches are. The authors have compiled more than 100 sources from different sub-fields of economics, finance, and regulation to create a coherent textbook that provides the reader with a clear and easily understandable picture of the new world of encrypted finance and its applications.

The book is primarily aimed at business and finance students, who already have an understanding of the basic principles of how the financial system works, but also targets a more general readership, by virtue of its broader scope and engaging and accessible tone.

Häufig gestellte Fragen

Wie kann ich mein Abo kündigen?

Gehe einfach zum Kontobereich in den Einstellungen und klicke auf „Abo kündigen“ – ganz einfach. Nachdem du gekündigt hast, bleibt deine Mitgliedschaft für den verbleibenden Abozeitraum, den du bereits bezahlt hast, aktiv. Mehr Informationen hier.

(Wie) Kann ich Bücher herunterladen?

Derzeit stehen all unsere auf Mobilgeräte reagierenden ePub-Bücher zum Download über die App zur Verfügung. Die meisten unserer PDFs stehen ebenfalls zum Download bereit; wir arbeiten daran, auch die übrigen PDFs zum Download anzubieten, bei denen dies aktuell noch nicht möglich ist. Weitere Informationen hier.

Welcher Unterschied besteht bei den Preisen zwischen den Aboplänen?

Mit beiden Aboplänen erhältst du vollen Zugang zur Bibliothek und allen Funktionen von Perlego. Die einzigen Unterschiede bestehen im Preis und dem Abozeitraum: Mit dem Jahresabo sparst du auf 12 Monate gerechnet im Vergleich zum Monatsabo rund 30 %.

Was ist Perlego?

Wir sind ein Online-Abodienst für Lehrbücher, bei dem du für weniger als den Preis eines einzelnen Buches pro Monat Zugang zu einer ganzen Online-Bibliothek erhältst. Mit über 1 Million Büchern zu über 1.000 verschiedenen Themen haben wir bestimmt alles, was du brauchst! Weitere Informationen hier.

Unterstützt Perlego Text-zu-Sprache?

Achte auf das Symbol zum Vorlesen in deinem nächsten Buch, um zu sehen, ob du es dir auch anhören kannst. Bei diesem Tool wird dir Text laut vorgelesen, wobei der Text beim Vorlesen auch grafisch hervorgehoben wird. Du kannst das Vorlesen jederzeit anhalten, beschleunigen und verlangsamen. Weitere Informationen hier.

Ist An Introduction to Cryptocurrencies als Online-PDF/ePub verfügbar?

Ja, du hast Zugang zu An Introduction to Cryptocurrencies von Nikos Daskalakis, Panagiotis Georgitseas im PDF- und/oder ePub-Format sowie zu anderen beliebten Büchern aus Économie & Macroéconomie. Aus unserem Katalog stehen dir über 1 Million Bücher zur Verfügung.

1.1 The traditional financial system and its main counterparts

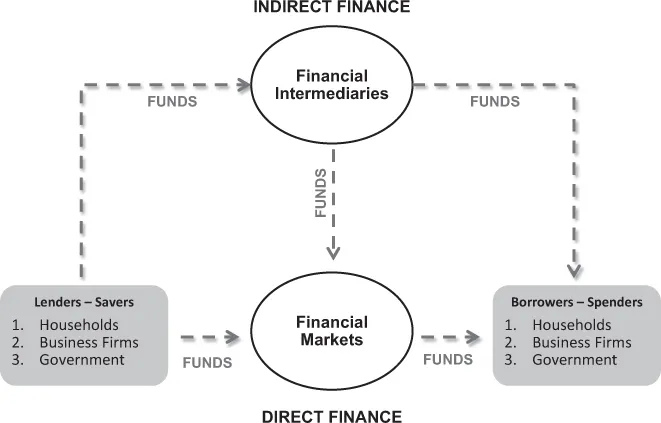

A broad definition of the “financial system” is that it is a set of interrelated activities or services structured to facilitate the flow of funds from where they stand to where they are needed. Specifically, for a set period of time, the income of some economic units (households, firms, government) is greater than their expenses, while the income of some others is lower than their expenses. Thus, there must be a way for the funds of the former, surplus economic units to flow to the latter, deficit economic units (Figure 1.1). This is what the financial infrastructure does; it facilitates this flow of funds from where they stand to where they are needed.

FIGURE 1.1 The financial system.

This financial infrastructure consists of two main parts: the financial markets (direct finance) and the financial intermediaries (indirect finance). In direct financing, lenders (savers) channel their funds directly to borrowers (spenders), while in indirect financing, lenders (savers) channel their funds to an intermediary, which then decides how to allocate the pool of money they have accumulated to borrowers (spenders). Just two simple examples, one per case. When Bob buys ten shares in the primary market of Sea and Sun plc., a listed company in the London Stock Exchange (LSE), he knows that his money is going directly to Sea and Sun plc. When Mary deposits £100 into her account in a bank, this amount of money is pooled with the deposits of millions of other depositors, and it is for the bank to decide to provide a loan to Sea and Sun plc. In both cases, all participants, Bob, Mary, and Sea and Sun plc. use the infrastructure of a financial market or financial intermediary, respectively, but Bob knows exactly where his money is going (direct finance), while Mary does not (indirect finance). There are plenty of other differences between these two main parts of the financial infrastructure, but this is the broad picture.

For a financial system to function properly, there has to be trust in the system. In fact, “a sufficient level of trust” is a necessary precondition for the stability and maintenance of any social, political, and economic system. When trust breaks down, the social system is threatened with unrest, and this is particularly true for the market-based economy, of which the financial system is a part. The notion of trust is of such high importance in finance that if trust is lost, the entire system might collapse, giving rise to what is known as “systemic risk”, a type of risk that is widely referred to in finance, especially in the aftermath of the Global Financial Crisis of 2008.

Turning to the basic functions of the financial system, the core objective, as already mentioned above, is to facilitate the allocation and deployment of economic resources, both spatially and across time, in an uncertain environment. This objective can be fulfilled via an efficient payment system, through which all transactions are cleared. The payment system is a core function of the financial system, alongside markets and institutions. Payment, clearing, and settlement arrangements are of fundamental importance for the functioning of the financial system and the conduct of transactions between economic agents in the wider economy. All economic units need to have effective and convenient means of making and receiving payments. Banks and other financial institutions are the primary providers of payment and financial services to end users, as well as being major participants in financial markets and important owners and users of systems for the processing, clearing, and settlement of funds and financial instruments.

Other, subsequent, but equally important, functions are those of: (a) fundraising, where capital is raised for economic units that need it, (b) finance pooling, where small amounts of capital are transformed into larger amounts of funding, (c) liquidity transformation, where the short-term investors’/savers’ horizon is transformed to long-term funding for fundraisers, (d) cost reduction, due to the large volume of repeated transactions, (e) risk pooling, which is the practice of sharing risks among a group of other companies, and (f) information and advice providers because of their expertise in the field of finance.

All these functions are carefully embedded in the way the financial infrastructure is developed. Trust is a necessary precondition for the entire system to function properly, while the payment system is a horizontal service that can be seen as the circulatory system of the financial infrastructure. Over time, technology has been constantly creating innovations of how the infrastructure evolves and how the notions of trust and payments can be facilitated, so that the efficiency of the entire system is improved. The most recent innovation that disrupts the way this infrastructure works is the blockchain technology, which is the core technological application in the new era of encrypted finance.

1.2 The new era of finance: encrypting the financial system

The previous section described the basics of the traditional financial system, briefly summarizing the main counterparts, participants, and functions thereof. This section explores how the recent technological innovation of blockchain has already started introducing new and more efficient ways to facilitate certain processes that the financial system currently offers.

It all started back in 2008, when an unknown person or group of people, using the name Satoshi Nakamoto, invented bitcoin. In October 2008, Satoshi Nakamoto published a white paper titled “Bitcoin: A Peer-to-Peer Electronic Cash System”1 describing bitcoin as “a purely peer-to-peer version of electronic cash, that would allow online payments to be sent directly from one party to another without going through a financial institution”. It is worth mentioning that the idea of having a digital currency was already a three-decade-old idea by 2008. From David Chaum’s “ecash” in the early 1980s to Wei Dai’s “B-money” and Nick Szabo’s “Bit Gold” in 1998, this idea was already there. But the main issue of all these early efforts was the double-spending problem, namely, how to make sure that a digital asset is only used once, and how a system can be designed to prevent copying and counterfeiting it. Satoshi Nakamoto’s idea of a peer-to-peer electronic cash system, based on the blockchain technology, provided answers to these problems. So, on 3 January 2009, Satoshi Nakamoto mined the Genesis Block, the first mined block in Bitcoin (Figure 1.2), and a new era of encrypted finance began.

FIGURE 1.2 First bitcoin transaction.

The idea of transacting values without the need of a financial institution is a truly disruptive idea for the financial system. The previous section underlined the importance of “trust” as a fundamental prerequisite for the financial system to function without problems. Note that in the absence of trust, the financial system faces systemic risk, that the whole system (not just one participant of the system) might collapse. Financial institutions also make sure that all transactions are recorded in a way that the double-spending problem is eliminated. So, anything that could emerge to challenge the way transactions services work should fulfill the main prerequisites of trust and double-spending avoidance. Satoshi Nakamoto’s idea to create a cryptocurrency using the blockchain technology seemed to fulfill these two necessary requirements.

The key idea behind the notion of “encrypted finance” lies in how the blockchain technology works. Although this technology will be explained in more detail in Chapter 2, it is worth referring here to some main functions of the technology. Blockchain technology uses cryptography. Cryptography is the method of disguising (i.e., encrypting) and revealing (i.e., decrypting) information through complex mathematics. This means that the information can only be viewed by the intended recipients and nobody else. Cryptography is used in blockchain in two ways. The first is via algorithms called cryptographic hash functions, which create a chain of hashes and ensure that the order of transactions is preserved. This resembles the function that the financial institutions use to record transactions in, what is called, a ledger. But unlike a centralized ledger held at one bank, blockchain creates the so called “distributed ledgers” system, where the ledger is distributed across many computers, with each computer having the same view of the ledger. The second way cryptography is used in the blockchain technology is to create digital signatures, which are used to ensure the data put on the blockchain is valid. In bitcoin, the digital signatures are used to ensure the correct amount of value is transferred from one bitcoin wallet to another.

This brief description of how the blockchain technology works shows how trust and the avoidance of the double-spending problem are dealt with. Encrypted transactions, which are practically impossible to break, bring trust to the system, while the distributed ledgers system, where all computers have the same view of the ledger, avoids the double-spending problem. So, when people transact using the blockchain technology, they trust the system for the fact that their transaction is recorded and cannot be counterfeited. For example, when Bob sends one bitcoin to Mary, they both trust that this transaction is valid and recorded, while anyone has access to the ledger that records transactions, thanks to the distributed ledger system, without necessarily knowing who Bob and Mary are.

These key features of the blockchain technology allow transactions to take place without the need of a financial middleman (markets and/or intermediaries). Bearing in mind that the main function of the financial system is to facilitate the flow of funds from lenders to borrowers, as discussed in Section 1.1, now it is worth looking at how certain participants and processes of the traditional system can be replaced via the use of the blockchain technology.

1.3 Introducing the main counterparts of the new encrypted financial system

Markets and banks act as middlemen in the financial system. They run, control, and own the necessary infrastructure needed for the financial processes to take place. The blockchain technology comes to disrupt certain functions that the traditional financial system offers by suggesting new ways of doing (financial) business. This section will briefly introduce what changes the technology seems to bring in the traditional players and parts of the financial system.

The purpose of this last section of Chapter 1 is to link the functions of the traditional financial system to a set of new processes/services/institutions that seem to emerge in the context of the new, encrypted financial system. Drawing direct links between the traditional and the new system aims to facilitate the understanding of how this new system works. Note that the subsections that follow practically offer a summarized context of the respective remaining chapters of the book.

1.3.1 The infrastructure

The infrastructure of recording transactions in a reliable and foolproof way is key to gain trust for the system. From B...