Artificial Intelligence in Accounting: Practical Applications was written with a simple goal: to provide accountants with a foundational understanding of AI and its many business and accounting applications. It is meant to serve as a guide for identifying opportunities to implement AI initiatives to increase productivity and profitability.

This book will help you answer questions about what AI is and how it is used in the accounting profession today. Offering practical guidance that you can leverage for your organization, this book provides an overview of essential AI concepts and technologies that accountants should know, such as machine learning, deep learning, and natural language processing. It also describes accounting-specific applications of robotic process automation and text mining. Illustrated with case studies and interviews with representatives from global professional services firms, this concise volume makes a significant contribution to examining the intersection of AI and the accounting profession.

This innovative book also explores the challenges and ethical considerations of AI. It will be of great interest to accounting practitioners, researchers, educators, and students.

Häufig gestellte Fragen

Wie kann ich mein Abo kündigen?

Gehe einfach zum Kontobereich in den Einstellungen und klicke auf „Abo kündigen“ – ganz einfach. Nachdem du gekündigt hast, bleibt deine Mitgliedschaft für den verbleibenden Abozeitraum, den du bereits bezahlt hast, aktiv. Mehr Informationen hier.

(Wie) Kann ich Bücher herunterladen?

Derzeit stehen all unsere auf Mobilgeräte reagierenden ePub-Bücher zum Download über die App zur Verfügung. Die meisten unserer PDFs stehen ebenfalls zum Download bereit; wir arbeiten daran, auch die übrigen PDFs zum Download anzubieten, bei denen dies aktuell noch nicht möglich ist. Weitere Informationen hier.

Welcher Unterschied besteht bei den Preisen zwischen den Aboplänen?

Mit beiden Aboplänen erhältst du vollen Zugang zur Bibliothek und allen Funktionen von Perlego. Die einzigen Unterschiede bestehen im Preis und dem Abozeitraum: Mit dem Jahresabo sparst du auf 12 Monate gerechnet im Vergleich zum Monatsabo rund 30 %.

Was ist Perlego?

Wir sind ein Online-Abodienst für Lehrbücher, bei dem du für weniger als den Preis eines einzelnen Buches pro Monat Zugang zu einer ganzen Online-Bibliothek erhältst. Mit über 1 Million Büchern zu über 1.000 verschiedenen Themen haben wir bestimmt alles, was du brauchst! Weitere Informationen hier.

Unterstützt Perlego Text-zu-Sprache?

Achte auf das Symbol zum Vorlesen in deinem nächsten Buch, um zu sehen, ob du es dir auch anhören kannst. Bei diesem Tool wird dir Text laut vorgelesen, wobei der Text beim Vorlesen auch grafisch hervorgehoben wird. Du kannst das Vorlesen jederzeit anhalten, beschleunigen und verlangsamen. Weitere Informationen hier.

Ist Artificial Intelligence in Accounting als Online-PDF/ePub verfügbar?

Ja, du hast Zugang zu Artificial Intelligence in Accounting von Cory Ng, John Alarcon im PDF- und/oder ePub-Format sowie zu anderen beliebten Büchern aus Business & Contabilità. Aus unserem Katalog stehen dir über 1 Million Bücher zur Verfügung.

Artificial Intelligence (AI) is transforming how we live and work. Intelligent virtual assistants on smartphones (e.g., Siri on Apple devices), facial recognition software on social media platforms (e.g., Facebook), and self-driving autonomous vehicles (e.g., Tesla) all utilize AI. Hospitals used AI in the battle against Covid-19. For example, Tampa General Hospital in Florida has deployed an AI system that performs facial thermal scans on patients entering the building to detect potential coronavirus symptoms such as sweat, discoloration, and fever (Wittbold et al., 2020). The convergence of big data analytics, advances in computing power, the Internet of Things (IoT), and large scale investment by governments, universities, and high-tech organizations such as Google, Amazon, Microsoft, and IBM have accelerated the adoption of AI for consumers and businesses.

These cases are just a few examples of the digital transformation we are currently experiencing, an era described by Klaus Schwab, founder and executive chairman of the World Economic Forum, as “The Fourth Industrial Revolution”. Schwab notes that the current revolution is distinct from the previous three due to the velocity of technological change, the breadth and depth of these technologies, and its impact on entire systems (i.e., countries, companies, industries, and society as a whole) (Schwab, 2017). AI is one of the key technologies driving this digital revolution.

So, what exactly is AI? Artificial intelligence is a computer program or software application that can imitate or simulate human behavior. AI applications are expected to automate a significant portion of the repetitive tasks performed by accountants, though the implications of this change for the accounting profession has divided scholars. Some critics speculate that sufficiently sophisticated AI will eliminate the need for accountants in the future. Others predict that the accounting profession will experience increased productivity and cost savings by incorporating AI technology. What is evident on both sides is that AI will have a significant impact on the accounting profession in the coming decades. As we will discuss throughout this book, and in more detail in Chapter 7, our view is that AI will not eliminate the need for accountants but empower them to deliver more accurate, timely, and forward-looking insights into the business(es). As part of the impending transformation of the profession, accountants will need to develop the skills necessary to provide mission-critical judgment and oversight of AI-enabled systems and processes in order for organizations to realize productivity gains and meet other objectives expected from AI. The purpose of this book is to provide accountants with a practical guide for identifying opportunities to implement artificial intelligence (AI) initiatives to increase productivity and profitability.

History of AI

Given the recent widespread media coverage on AI, the field of AI may seem like a new discipline. However, the roots of AI’s can be traced back to 1943 when neurophysiologist Warren McCulloch and logic expert Walter Pitts proposed the first model of artificial neurons (Russell & Norvig, 2010). The field of AI was established as an academic and research discipline when the first AI conference was organized at Dartmouth College in 1956 (Bringsjord & Govindarajulu, 2018). Today, AI is an interdisciplinary field of science, engineering, statistics, philosophy, neuroscience, psychology, computer engineering, and others.

History of Accountants Using Technology

Technology has always played an important role in accounting for business transactions through the ages – from the use of an abacus over 2,000 years ago (New York State Society of CPAs, 2015), to the purchase of a computer in 1955 exclusively for accounting purposes (Untapped Editorial Team, 2018), to the creation of electronic spreadsheets in the 1980s (Pepe, 2011). AI is the next significant technological advancement that will play an essential role in the accounting profession for years to come.

Overview of How Accountants Are Using AI

Accountants currently use AI in a variety of applications, from identifying high-risk transactions in audits to performing accounts payable processing tasks. As a result, AI is increasingly taking the place of human processing and decision-making, which will continue to have a transformative impact on business practices. Although AI adoption in the accounting profession is in its early stages, practitioners must understand the implications of this technology.

The adoption of AI has been on a steady rise in both public and corporate accounting. For example, EY1 uses AI drones to perform inventory counts with increased accuracy and efficiency. Deloitte2 uses a tool called “Argus” to extract critical accounting information from any type of electronic document to improve the quality and efficiency of an audit (Deloitte, 2015). In management accounting, AI is used to automatically code accounting entries, forecast revenues, and analyze unstructured data such as contracts and emails (ICAEW, 2017).

Going forward, it is even more exciting to think about how AI will be used in accounting. Imagine if you could ask an intelligent virtual assistant (such as Alexa or Siri) to analyze accounts payable for duplicate payments as part of your audit procedures. Technological advances in artificial intelligence could make this possible very soon. Researchers Burns and Igou (2019) suggest that accountants should consider using intelligent virtual assistants to interface with AI applications to perform audit analysis, data retrieval, spreadsheet creation, and data visualizations – all activated by human commands.

Human Intelligence versus Artificial Intelligence

For more than 2,000 years, philosophers have pondered questions such as “how does the human mind work?” and “can non-humans have minds?” (Negnevitsky, 2011, p. 1). The Merriam-Webster dictionary (2020) defines intelligence as follows:

1. The ability to learn or understand or to deal with new or trying situations

2. The ability to apply knowledge to manipulate one’s environment or to abstractly think as measured by objective criteria (such as tests)

For decades, scholars in the field of psychology have debated what constitutes human intelligence (Weiner & Freedheim, 2013). Some experts describe human intelligence as the capacity for “reasoning, problem solving and learning” (Colom et al., 2010). Additional common characteristics of human intelligence include logical thinking, spatial perception, and pattern recognition (Yao et al., 2018). Human intelligence also involves the ability to perceive, understand, and predict (Russell & Norvig, 2010) as well as the capacity for planning and adaptability (Siegel et al., 2003).

The goal of AI is to build machines that “can perform complex tasks as well as, or better than, humans. In order to perform those complex tasks, machines must be able to perceive, reason, learn, and communicate” (Siegel et al., 2003, p. 1). Achieving this goal has been the quest of computer scientists and engineers for more than half a decade. Computers are very good at performing specific tasks, such as complex math calculations, with speed and accuracy. Yet, today’s computers are not as good at performing tasks such as abstract reasoning, concept formulation, and strategic planning (Yao et al., 2018).

What Accountants Need to Know About AI

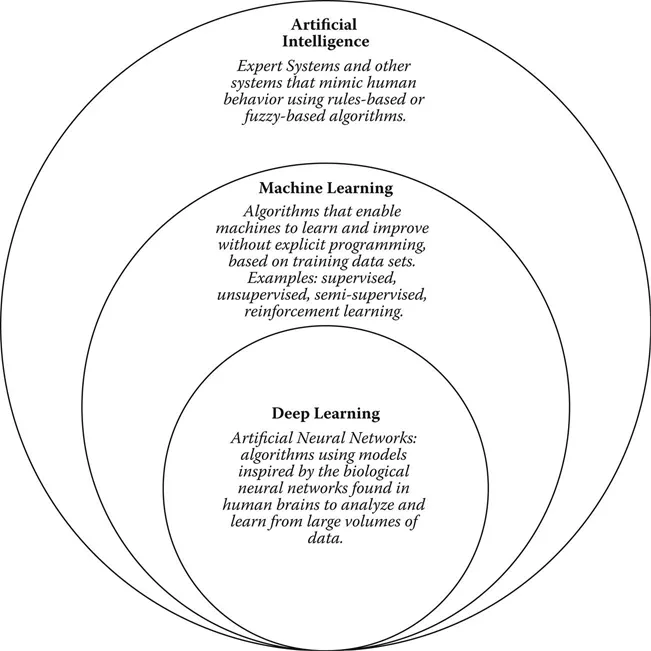

Artificial intelligence is divided into a variety of sub-fields, including but not limited to machine reasoning, machine learning, deep learning, and natural language processing. Each of these sub-fields has essential applications in accounting. In effect, AI has fields that may even be nested as sub-fields, such as Deep Learning (DL) is a sub-field of Machine Learning (ML), as illustrated in Figure 1.1.

Figure 1.1 Relationship between AI, ML, and DL.

Artificial Intelligence

As stated in the introduction, artificial intelligence is defined broadly as a computer program or software application that can imitate or simulate human behavior. This definition works well with a variety of technologies that we use every day. For example, the words that you are currently reading were spoken into a dictation tool in a popular word processing software. This form of AI uses speech recognition software to translate audio data into text, mimicking the actions of a human transcriber.

However, it is important to recognize that a generally accepted definition of artificial intelligence remains open for debate (Dobrev, 2012). An influential textbook in AI research entitled Artificial Intelligence: A Modern Approach offers four possibilities: systems that think like humans, systems that act like humans, systems that think rationally, and systems that act rationally (Russell & Norvig, 2010). Today speech recognition is considered a form of AI and tomorrow it may be relegated to straightforward automation. The bottom line here is that what constitutes AI continues to evolve with time and technological advances. Although a consensus may not exist on a formal definition of AI, experts often make a distinction between two subtypes of AI – artificial narrow intelligence (ANI) and artificial general intelligence (AGI).

Artificial Narrow Intelligence (ANI)

Artificial narrow intelligence (ANI), also known as weak or narrow AI, focuses on a task, such as speech recognition, computers that can play chess, or autonomous vehicles. Virtually all of the AI with which we are familiar can be classified as ANI, as computer scientists have yet to create machines that can experience emotion and the ability to perceive or feel things (Jajal, 2018). ANI machines that are programmed for these specific tasks are typically much better than their humans at doing the same task.

Examples of narrow AI include chatbots that are built for the narrow purpose of conversation. Chatbots are capable of verbal responses, using algorithms and a database, based on a statement or question.

Artificial General Intelligence (AGI)

The goal of artificial general intelligence (AGI), also known as strong or broad AI, is to create machines capable of performing all the cognitive tasks of the human brain. The essential elements of AGI include: (1) the ability to apply knowledge from one domain to another; (2) the ability to plan for the future based on experience and knowledge; and (3) the ability to adapt based on changing circumstances (Walch, 2019).

Machine Reasoning

Machine reasoning (MR) is the ability of a computer to draw conclusions from a knowledge base using automated inference techniques that can imitate or simulate human inference, such as deduction and induction. León Bottou, a reasoning expert, provides a more technical definition of MR as an “algebraic manipulation of previously acquired knowledge in order to answer a new question” (Bottou, 2014, p. 136).

Expert Systems

The initial applications of reasoning systems were referred to as expert systems (ES). Expert systems are an early form of AI, first developed in the 19...