How Companies Win with Design Thinking, Agile, and Lean Startup

Pascal Dennis, Laurent Simon

This is a test

This is a test

218 Seiten

English

ePUB (handyfreundlich)

Über iOS und Android verfügbar

eBook - ePub

Harnessing Digital Disruption

How Companies Win with Design Thinking, Agile, and Lean Startup

Pascal Dennis, Laurent Simon

Angaben zum Buch

Buchvorschau

Inhaltsverzeichnis

Quellenangaben

Über dieses Buch

Our world has changed, probably for good. Until now, the shift from brick-and-mortar to the smartphone has been about service, cost, and convenience. Now, it's also a matter of public health. How do we win this uncertain new game? How do we prosper in a digital world?

In a cool, readable style Harnessing Digital Disruption: How Companies Win with Design Thinking, Agile, and Lean Startup tells the story of a major multi-national organization facing digital disruption and looming irrelevance. In a compelling novel format, the book demonstrates how to harness the power of digital technology, methods and thinking on the path to revival and prosperity. It illustrates the situations, characters, and blockers you'll likely face as you progress through your journey.

The setting is Singapore and the heady world of international banking, but the prescription, methods and lessons apply equally to manufacturers, utilities, hospitals, insurers, and government agencies. You will learn how to:

· Develop your Digital Transformation strategy and Innovation Portfolio · Reform customer journeys, launch new digital offerings, and validate new beta businesses · Develop senior leader digital literacy, and understanding of growth leadership · De-risk your journey using a proven overall approach based on proven principles · Cultivate a network of pragmatic entrepreneurs practicing a structured scalable innovation process

Häufig gestellte Fragen

Wie kann ich mein Abo kündigen?

Gehe einfach zum Kontobereich in den Einstellungen und klicke auf „Abo kündigen“ – ganz einfach. Nachdem du gekündigt hast, bleibt deine Mitgliedschaft für den verbleibenden Abozeitraum, den du bereits bezahlt hast, aktiv. Mehr Informationen hier.

(Wie) Kann ich Bücher herunterladen?

Derzeit stehen all unsere auf Mobilgeräte reagierenden ePub-Bücher zum Download über die App zur Verfügung. Die meisten unserer PDFs stehen ebenfalls zum Download bereit; wir arbeiten daran, auch die übrigen PDFs zum Download anzubieten, bei denen dies aktuell noch nicht möglich ist. Weitere Informationen hier.

Welcher Unterschied besteht bei den Preisen zwischen den Aboplänen?

Mit beiden Aboplänen erhältst du vollen Zugang zur Bibliothek und allen Funktionen von Perlego. Die einzigen Unterschiede bestehen im Preis und dem Abozeitraum: Mit dem Jahresabo sparst du auf 12 Monate gerechnet im Vergleich zum Monatsabo rund 30 %.

Was ist Perlego?

Wir sind ein Online-Abodienst für Lehrbücher, bei dem du für weniger als den Preis eines einzelnen Buches pro Monat Zugang zu einer ganzen Online-Bibliothek erhältst. Mit über 1 Million Büchern zu über 1.000 verschiedenen Themen haben wir bestimmt alles, was du brauchst! Weitere Informationen hier.

Unterstützt Perlego Text-zu-Sprache?

Achte auf das Symbol zum Vorlesen in deinem nächsten Buch, um zu sehen, ob du es dir auch anhören kannst. Bei diesem Tool wird dir Text laut vorgelesen, wobei der Text beim Vorlesen auch grafisch hervorgehoben wird. Du kannst das Vorlesen jederzeit anhalten, beschleunigen und verlangsamen. Weitere Informationen hier.

Ist Harnessing Digital Disruption als Online-PDF/ePub verfügbar?

Ja, du hast Zugang zu Harnessing Digital Disruption von Pascal Dennis, Laurent Simon im PDF- und/oder ePub-Format sowie zu anderen beliebten Büchern aus Negocios y empresa & Cultura del lugar de trabajo. Aus unserem Katalog stehen dir über 1 Million Bücher zur Verfügung.

Amy Tay sits down opposite Martin Picard. “This is one of my favorite places,” she says, taking in the panorama. They order lunch and exchange pleasantries.

“Why did we lose your business, Amy?” Martin asks. “We’ve worked with your family for half a century.”

Amy takes a breath. “Asia Pacific Bank (APB) is slow, unreliable and expensive.”

Martin looks out across the Central Business District (CBD) and the iconic Marina Bay Sands building. The Strait of Malacca is busy, as usual, with ships pouring in from both the Andaman and South China seas. He has a good relationship with Amy and her father, Kwong Yip, who is now semi-retired. That’s why she’s here, he realizes, and being so blunt. She’s trying to help.

Martin remembers when their clothing design and retail business, KY Tay International, was just a few stores. Now it’s an East Asian power-house, a regional dynamo, with hundreds of stores and a striking on-line presence. A dream client for APB’s Corporate banking division.

“It pains me to hear that, Amy. It would really help if you can be specific.”

“On the commercial side,” Amy replies, “getting paid, and paying our suppliers and employees was often a hassle. There were always overpayments, underpayments, and missed payments. On the wealth management side, your advisors were slow, disorganized and expensive. Sometimes, I felt like I was educating them. On the personal side, you even lost my daughter’s tuition money a few months ago. She was crying and worried she might lose her place at Oxford. It took several days to fix the problem and you still wanted to charge me!”

Martin has only been CEO for a few months. Profitability is declining, costs are rising, and Martin is counting on growth to solve his problems. Now Amy Tay is saying that three of his core businesses – Commercial Banking, Wealth Management and Retail Banking – are lousy. Have I accepted a poisoned chalice, he wonders?

“I don’t mean to be disrespectful,” Amy continues. “You know how important relationships are to our family. But we have other alternatives now, and your service issn’t getting any better.”

“What kind of alternatives?” Picard asks.

Amy holds up her smartphone. “Look Martin, digital methods help me manage design, sourcing, inventory, sales, and warehousing. We’re hoping digital can also help manage our complex logistics and Trade Finance. You know what our bottleneck is? Asia Pacific Bank – working with you is like going back in time. Forgive me for speaking severely.”

Picard listens quietly, Amy’s words reverberating: slow, unreliable, and expensive…

“Amy,” he says finally, “what do we have to do to get better?”

“You have to wake up, Martin.”

Martin lingered after Amy Tay left. He looked out again toward the Port of Singapore, one of the world’s biggest and most successful. You’d think they’d stand pat, thought Martin. But the Republic was betting big on unseen long-term trends. The massive TUAS port expansion project to the west would triple the port’s size. And it would be a ‘Smart’ port, with digital technology, sensors, automated cranes, driverless vehicles, drones to inspect equipment, and a smart grid. The executive team was committed to seamless and efficient port clearance. “We want to cut turnaround times in half,” the port’s Chief Operating Officer had told him. “Nobody wants to wait.”

But Asia Pacific Bank clients have to wait for everything, thought Martin. They wait for accounts to open, payments to clear, loans to be approved, and for APB to fix the many transaction errors. Delay, errors and hassle, that’s us, thought Martin. Can we learn to apply technology the way the Port of Singapore – or Amy’s company does, he wondered? Can we become a digital bank? And is Technology alone the answer? A respected colleague told him transformation was fundamentally about culture.

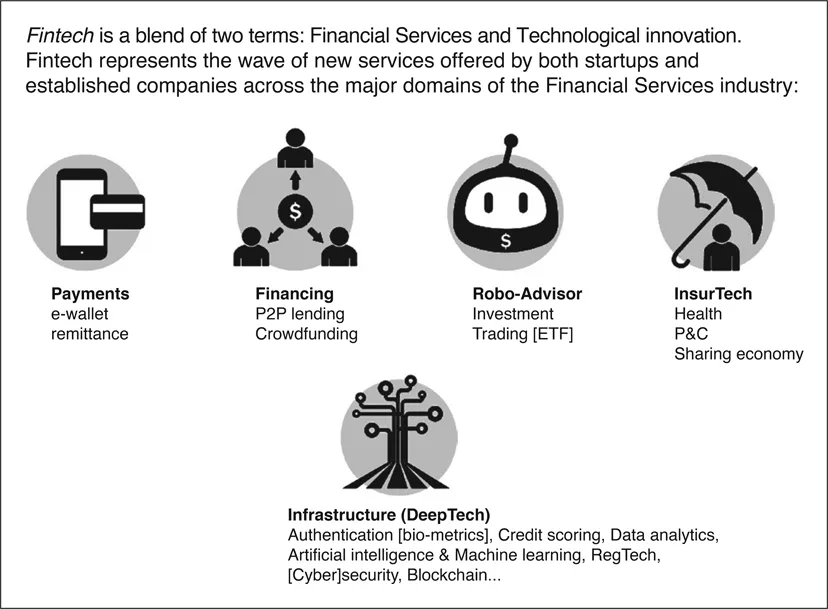

Martin was a business guy, primarily interested in strategy, budgets and technology, and less so in the ‘soft stuff’ like culture. He was well aware of the so-called Fintech disruption, but had believed the threat was overblown [See Figure 1.1]. We have trust, Martin had told himself, and in banking that’s the most important thing. Our retail customers, business clients and regulators trust us with money and information. We also have scale, resources, a banking license and matchless marketing muscle. How can the Fintechs compete with that? On the other hand, Fintechs, not banks, seem to be doing most of the hiring.

Figure 1.1What Is Fintech?

Source: FutureFintech.io

And now here is Amy Tay, he thought, telling us we’re dinosaurs. Have I been a bozo? If this is how Amy feels, what chance do we have with her children and the next generation of entrepreneurs?

Revenue was flat, cost was rising, and Cost-to-Income ratio2 continued to worsen, which meant that investors didn’t like what they saw either. Martin was feeling old and tired, but he had never lacked courage. Maybe we can turn this threat into an opportunity, he thought. Maybe APB can learn from Fintechs and technology firms in general, and thereby improve our capability, operations and current offering. And that’s when he decided to call Yumi Saito.

2 The cost-to-income ratio is a key financial measure in valuing banks. To get the ratio, divide the operating costs (administrative and fixed costs, such as salaries and property expenses, but not bad debts that have been written off) by operating income. The ratio gives investors a clear view of how efficiently the firm is being run – the lower it is, the more profitable the bank will be.

For both corporate clients and individual customers, the best Fintechs offer services and products that are cheaper, faster, more convenient, and more transparent than those of traditional financial institutions. They’re compelling banks, insurers, and Financial Services regulators around the world to revisit their overall approach and activities.

“Hello Yumi-san, it’s Martin,” he said. “Long time no see… Listen, I want you to come back to Asia Pacific Bank!”

After a moment, Martin heard a familiar laugh roll out of his cell phone. “Martin Picard, subtle as always! I heard about your promotion: CEO of Asia Pacific Bank – congratulations!”

“Thanks, Yumi. But I’m serious, we need you back. I’m not so sure about this place anymore.”

“You haven’t changed at all, Martin-san. How are Monique and the kids?”

“The family is great. The boys are finishing high school, and Monique is back at work. Life is good. Business-wise, we’re in trouble, Yumi-san. I feel a typhoon coming. I’m afraid it’s going to be worse than the Global Financial Crisis.”

Martin told Yumi what Amy Tay had said, what losing a key client like KY Tay international meant for APB and all that he’d learned since becoming CEO. “I want you to help me transform our business, Yumi. I want to learn and apply the latest and greatest technologies. I want to learn from Fintechs and technology firms in general, and maybe even partner with them. I want to change our culture. I intend to create a new senior position for you and to give you all the resources you need.”

Martin Picard had spent his first three months as CEO talking to clients, employees, suppliers, and partners of Asia Pacific Bank’s core businesses: Retail Banking, Commercial Banking, and Wealth Management. He met with APB leaders at all levels and with front-line employees. He talked to regulators, competitors and pundits. He read books, watched videos, and attended lectures.

Fintechs were sprouting up all over Singapore and the Asia Pacific region. They seemed to be full of creative, motivated young people doing interesting things. Their mantras seemed to resonate with people. ‘Think big, start small, scale fast’ and ‘Build products your customer wants’.

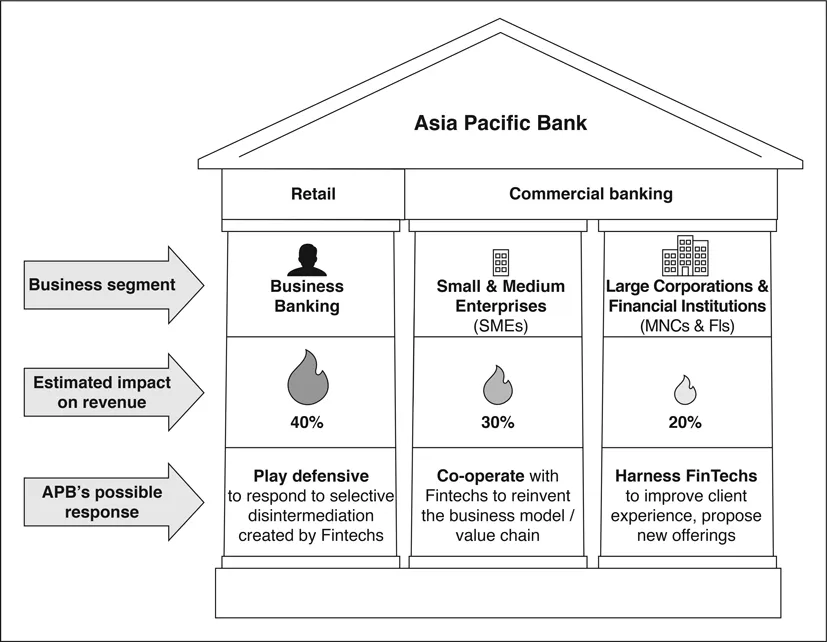

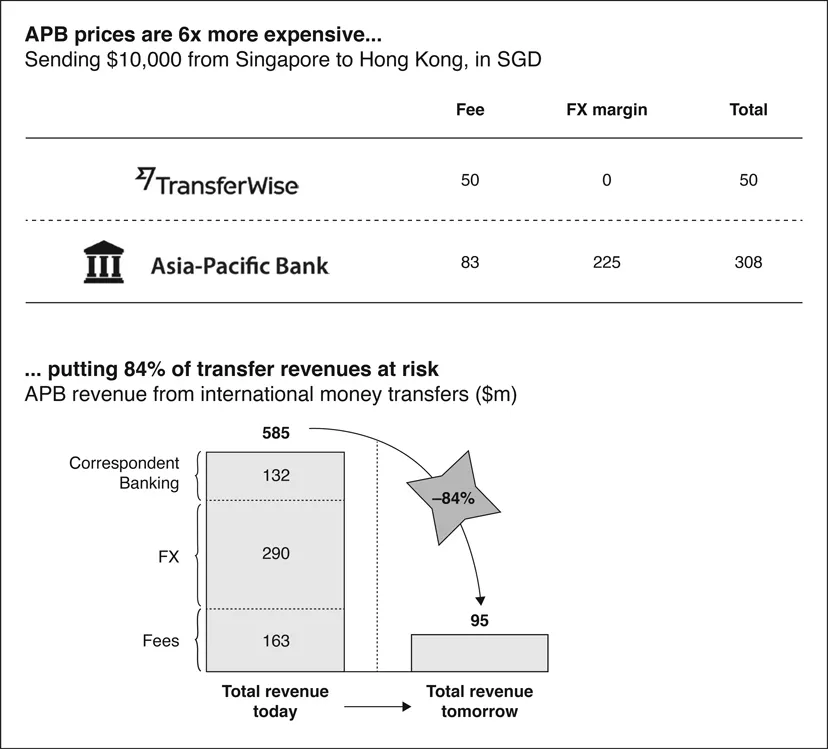

Martin’s feelings were mixed. Fintechs were direct competitors with cutting edge technology and few regulatory constraints. There were worrisome presentations on Fintech’s potential effect on APB’s business [See Figure 1.2]. As Jamie Dimon put it: “Hundreds of startups with a lot of brains and money are working on various alternatives to traditional banking. They all want to eat our lunch. Every single one of them is going to try.”3[See Figure 1.3]

3 JP Morgan CEO, in JPMC 2014 Letter to Shareholders/.

Figure 1.2Potential Impact of Fintech on APB’s Overall Business

Source: Singapore Fintech Festival (iso Singapore Fintech Festival)

Figure 1.3Impact of Fintech on APB’s Payment Business

Source: Digital Pathways (inspired by a real-life situation)

On the other hand, thought Martin, maybe we can learn from Fintechs – not just their technology, but also how they work. Maybe they can help us reassess our offering, channels and how we work.

To Martin’s chagrin, few established Fintechs had any interest in...

Inhaltsverzeichnis

Zitierstile für Harnessing Digital Disruption

APA 6 Citation

Dennis, P., & Simon, L. (2020). Harnessing Digital Disruption (1st ed.). Taylor and Francis. Retrieved from https://www.perlego.com/book/2039296/harnessing-digital-disruption-how-companies-win-with-design-thinking-agile-and-lean-startup-pdf (Original work published 2020)

Chicago Citation

Dennis, Pascal, and Laurent Simon. (2020) 2020. Harnessing Digital Disruption. 1st ed. Taylor and Francis. https://www.perlego.com/book/2039296/harnessing-digital-disruption-how-companies-win-with-design-thinking-agile-and-lean-startup-pdf.

Harvard Citation

Dennis, P. and Simon, L. (2020) Harnessing Digital Disruption. 1st edn. Taylor and Francis. Available at: https://www.perlego.com/book/2039296/harnessing-digital-disruption-how-companies-win-with-design-thinking-agile-and-lean-startup-pdf (Accessed: 15 October 2022).

MLA 7 Citation

Dennis, Pascal, and Laurent Simon. Harnessing Digital Disruption. 1st ed. Taylor and Francis, 2020. Web. 15 Oct. 2022.