Austrian Economics Re-examined: The Economics of Time and Ignorance is an expanded version of the 1996 edition of The Economics of Time and Ignorance. This work is a classic statement of the role of subjectivism, radical uncertainty and change through real time in Austrian economics specifically, and in modern economics more generally.

The new book contains the full text and Introductions of the earlier edition as well as the comprehensive previously-unpublished essay "What is Austrian Economics?" and a new Introduction. The essay is a comprehensive overview of the central themes of the book from a somewhat different perspective than in the book itself. It supplements the analysis in the book. The new Introduction explains that the 2007-8 financial crisis and recent developments in behavioural economics have made the book more relevant than ever before.

Austrian Economic Re-examined develops and systematizes the fundamental principles of the Austrian tradition to the analysis of rational expectations, business cycles, monetary theory competition and monopoly, and capital theory.

The Open Access version of this book, available at https://www.taylorfrancis.com/books/oa-edit/10.4324/9781315776736, has been made available under a Creative Commons Attribution-Non Commercial-No Derivatives 4.0 license.

Häufig gestellte Fragen

Wie kann ich mein Abo kündigen?

Gehe einfach zum Kontobereich in den Einstellungen und klicke auf „Abo kündigen“ – ganz einfach. Nachdem du gekündigt hast, bleibt deine Mitgliedschaft für den verbleibenden Abozeitraum, den du bereits bezahlt hast, aktiv. Mehr Informationen hier.

(Wie) Kann ich Bücher herunterladen?

Derzeit stehen all unsere auf Mobilgeräte reagierenden ePub-Bücher zum Download über die App zur Verfügung. Die meisten unserer PDFs stehen ebenfalls zum Download bereit; wir arbeiten daran, auch die übrigen PDFs zum Download anzubieten, bei denen dies aktuell noch nicht möglich ist. Weitere Informationen hier.

Welcher Unterschied besteht bei den Preisen zwischen den Aboplänen?

Mit beiden Aboplänen erhältst du vollen Zugang zur Bibliothek und allen Funktionen von Perlego. Die einzigen Unterschiede bestehen im Preis und dem Abozeitraum: Mit dem Jahresabo sparst du auf 12 Monate gerechnet im Vergleich zum Monatsabo rund 30 %.

Was ist Perlego?

Wir sind ein Online-Abodienst für Lehrbücher, bei dem du für weniger als den Preis eines einzelnen Buches pro Monat Zugang zu einer ganzen Online-Bibliothek erhältst. Mit über 1 Million Büchern zu über 1.000 verschiedenen Themen haben wir bestimmt alles, was du brauchst! Weitere Informationen hier.

Unterstützt Perlego Text-zu-Sprache?

Achte auf das Symbol zum Vorlesen in deinem nächsten Buch, um zu sehen, ob du es dir auch anhören kannst. Bei diesem Tool wird dir Text laut vorgelesen, wobei der Text beim Vorlesen auch grafisch hervorgehoben wird. Du kannst das Vorlesen jederzeit anhalten, beschleunigen und verlangsamen. Weitere Informationen hier.

Ist Austrian Economics Re-examined als Online-PDF/ePub verfügbar?

Ja, du hast Zugang zu Austrian Economics Re-examined von Gerald P O'Driscoll Jr, Mario Rizzo im PDF- und/oder ePub-Format sowie zu anderen beliebten Büchern aus Business & Business General. Aus unserem Katalog stehen dir über 1 Million Bücher zur Verfügung.

The world has changed tremendously since the first Blackwell edition of the book in 1985, and since the Routledge edition in 1996. There have been very important changes in the economy and in the discipline of economics. Paradoxically, these have made our book much more relevant than it was. The changes in the external world and in the economics profession have destroyed, or at least seriously weakened, many of the taboos that used to dominate economic thought. The passage of time and the growth of knowledge combined to bring about a new era.

It used to be the case that questioning the static nature of competitive theory was not fashionable, but clearly economists are more concerned now about dynamic issues. How could they not when innovations are springing up everywhere around us? The universal applicability of rigid and narrow axiomatic rationality assumptions (preference completeness, transitivity, and independence of framing, etc.) is under severe pressure from behavioral economics. The questioning of these opens the door to a greater appreciation of the pragmatic nature of economic rationality and to the subjective interpretation of economic “data.” We are also now permitted to question the intrapersonal stability of tastes. Economists are thus more willing to embrace the importance of change even at the level of the individual.

The financial crisis of 2007–08 and the associated Great Recession were extremely important economic events that have had a still difficult-to-evaluate impact on economic thinking. The general revival of Keynesian thought during the financial panic and the Great Recession and its aftermath brought with it a renewed appreciation of the old Keynes-Hayek debate as it became obvious that Keynes and Hayek were the true antipodes on the fundamental macroeconomic issues. We were extremely interested in this in our book – as well as in those areas in which we believe Keynes had valuable things to say.

The importance of Knightian and radical uncertainty has not gone unnoticed by economists in view of the financial crisis. We remember many neoclassical economists saying that the distinction between risk and uncertainty is not very important. Situations could be modeled, they said, as if they were merely risky, especially in light of subjective probability. However, insofar as the riskiness of new asset forms were judged by the “stable” data of recent history the possibility of structural change was ignored to the detriment of all.

The rule of law (a topic long of concern to Hayek) became an issue of renewed importance in understanding the policy response to the financial crisis, the Great Recession and other problems. Increasingly critics worried about the violations of the rule of law in Federal Reserve policy, in TARP and in the auto bailout.1

These developments naturally led to an accelerated appreciation of the importance of institutions. This was a development that had been gaining importance, perhaps ever since the work of Ronald Coase. But institutions become even more important – a matter of economic life or death – during rough patches.

Institutions cannot be fully understood except in the context of local knowledge, another Hayekian theme, as was seen in the still-limited recovery from Hurricane Katrina in New Orleans.2 In a development-economics context, the neglected importance of local knowledge became a critical point in analyzing what critics believe is the overall failure of World Bank policies.

Thus, the shifting and dissolution of scientific taboos and the recognition of certain “Austrian issues” promoted by recent events, even when they are not recognized as Austrian, have given the ideas in the book new and heightened relevance. We believe that our ideas provide, in many cases, an alternative to the increasingly obvious poverty of standard approaches.

The plan

In this new introduction there will be two main parts. In the first we sketch the impact of recent economic history on (mainly) the macroeconomic and monetary ideas that we sought to promote in this book. In the second we describe recent developments in behavioral economics that strengthen the case for our general approach.

I. The impact of economic crises

The financial crisis began with the Panic of 2007, and continued into 2008 with multiple crisis events involving, among others, mortgage giants Fannie Mae and Freddie Mac; failed investment banks like Bear Stearns (bailed out) and Lehman Brothers (not bailed out); and many financial firms whose solvency was in doubt at some point (e.g., Citigroup and Morgan Stanley).3 The Panic involved a great housing boom financed by innovative financial instruments. After the housing boom ended there was a crisis in housing finance involving actual or perceived insolvency of firms at the center of housing finance.

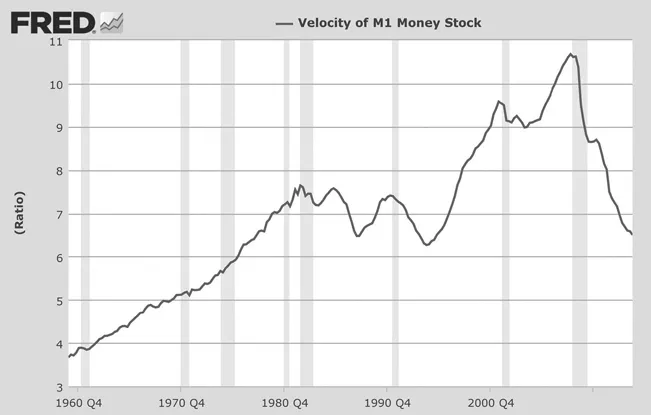

The crisis occurred in the midst of a period known as the Great Moderation (Taylor, 2009, pp. 34–46). It was a period in which the growth rates of monetary aggregates moderated. Macroeconomic flow variables, like real GDP, became less volatile. But it was also a period of a great expansion in the velocity of the M1 monetary aggregate.

Figure I.1 Velocity of M1 money stock

Source: Federal Reserve Bank of St. Louis. 2014 research. stlouisfed.org.

The increase in velocity, or decrease in money demand, accompanied the rise of “shadow banking,” in which housing loans (and other bank lending) were securitized. Long-term debt, like home mortgages, was increasingly financed by short-term credit, even overnight funding as was so famously the case with Lehman Brothers. A credit pyramid was erected upon a narrow base of bank money. The possession of Treasury securities or other eligible collateral financed transactions in repo (overnight repurchase agreements) markets. Gorton succinctly described the process.

Another important feature of repo is that the collateral can be rehypothecated. In other words, the collateral received by the depositor can be used – “spent” – in another transaction, i.e., it can be used to collateralize a transaction with another party. Intuitively, rehypothecation is tantamount to conducting transactions with the collateral received against the deposit. There is no data on the extent of rehypothecation.

(Gorton, 2010, p. 44)

Traditional banking was increasingly being replaced by securities markets. Banks and thrift institutions continued to play a role in originating home mortgages (though origination was also done by mortgage companies). But they no longer held the mortgages, which were bundled with others and sold off as securities. Information about the underlying risk of each mortgage was lost in the process. Yet securitization only grew. Investment banks supplanted commercial banks, and repo markets grew in importance relative to the federal funds market.

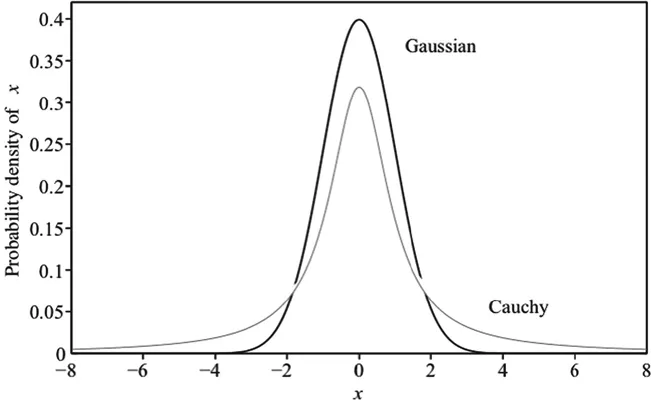

Figure I.2 Gaussian vs. Cauchy distribution chart http://research.stlouisfed.org/fred2/series/M1V/

During the crisis, the repo market dried up. But so, too, has the federal funds market. The Federal Reserve’s extraordinary monetary policy actions (quantitative easing or QE) have made it, and not interbank lending, the source of liquidity in banking. Today the Federal Reserve is increasingly operating in repo markets.4

The conventional modern analysis of risk was challenged by these developments in financial markets. The challenge has been analyzed in two, ultimately complementary, ways. One line of analytical criticism of standard risk models we will describe as immanent. It questions the properties of the distribution of risk. Standard risk analysis models risk with a Gaussian distribution. That is typically described as a normal or bell curve. The events in the recent financial crisis suggest “that financial returns are not Gaussian – or even remotely so” (Dowd et al., 2011, p. 14).

The Cauchy distribution is one “fat-tail” distribution, and it is reproduced here along with a normal distribution. The Cauchy distribution implies that “extreme losses are much more likely than under the Gaussian” (Dowd et al., 2011, p. 14). How much more likely? In August 2007, Goldman Sachs’ CFO David Viniar stated that “we were seeing things that were 25-standard deviation moves, several days in a row.”5 Dowd et al. estimate that a single 25-standard deviation event should occur only once every 10 (to the 137th power) years. They conclude that “to be plausible, risk models need to be based on alternative distributions to the Gaussian” (Dowd et al., 2011, p. 14).

Alternatively, one can view recent events as manifestations of Knightian uncertainty. Frank Knight argued there was (1) an absence of objective probabilities and (2) an inability to list, or determine beforehand, the complete set of possible outcomes. Risk managers extrapolated recent history to model the riskiness of new types of complex and bundled securities, especially mortgage-backed securities (MBS). In 2009, Edmund Phelps asked rhetorically, “why did big shareholders not move to stop over-leveraging before it reached dangerous levels? Why did legislators not demand regulatory intervention?” He went on:

The answer, I believe, is that they had no sense of the existing Knightian uncertainty. So they had no sense of the possibility of a huge break in housing prices and no sense of the fundamental inapplicability of the risk management models used in the banks. “Risk” came to mean volatility over some recent past. The volatility of the price as it vibrates around some path was considered but not the uncertainty of the path itself: the risk that it would shift down. The banks’ chief executives, too, had little grasp of uncertainty. Some had the instinct to buy insurance but did not see the uncertainty of the insurer’s solvency.

(Phelps, 2009)

The Knightian critique is more fundamental, since it questions whether there are discoverable distributions of risk in all instances. Knight certainly recognized that many risks are calculable. Modern risk analysis collapses Knightian uncertainty into quantifiable risk, and then assumes a normal distribution of risk. In the wake of the financial crisis, each of those steps must be questioned.

When the housing boom went bust, economists of the Austrian school saw it as a textbook example of malinvestment ending in a crisis. The Austrian analysis built on that of classical political economy – as Mises, Hayek and others long emphasized (Mises 1966, p. 204). Some financial analysts, economists and members of the public acknowledged the applicability of Austrian analysis. Many members of the economics profession busily defended theories that neither predicted nor accounted for what had happened.

The most surprising thing, however, was that the public policy response was to fall back on crude versions of Keynesian income-expenditure models. Hoary myths of fiscal-expenditure multipliers greater than one were resurrected, in some cases by advisers to President Obama whose own work undermined such beliefs. Of such beliefs, Milton Friedman observed more than 50 years ago that “they are part of economic mythology, not the demonstrated conclusions of economic analysis or quantitative studies” (Friedman, 2002, p. 84). In the ensuing 50 years, a large body of economic research – economic analysis and quantitative studies – debunked that mythology. Much of the work was done by Friedman, his colleagues and students. As this is written, we have just passed the fifth anniversary of the Obama “stimulus” program. No one, to our knowledge, has mounted a serious argument that it had concrete, measurable benefits.

An important conference put on in March 2009 by the Mont Pelerin Society focused on whether the Great Recession was best explained by Austrian economic analysis or that of another school, Keynesian or otherwise. In a seminal paper, Axel Leijohnufvud (2009) examined whether the downturn was one best analyzed by an income-expenditure model, i.e., in terms of economic flows. He concluded that it was not. Instead, he declared it to be a classic balance-sheet recession, and one best analyzed by Austrian analysis.

All of the macroeconomic policies implemented in the Great Recession ignored its character as a balance-sheet recession. When h...