Detect fraud faster—no matter how well hidden—with IDEA automation

Fraud and Fraud Detection takes an advanced approach to fraud management, providing step-by-step guidance on automating detection and forensics using CaseWare's IDEA software. The book begins by reviewing the major types of fraud, then details the specific computerized tests that can detect them. Readers will learn to use complex data analysis techniques, including automation scripts, allowing easier and more sensitive detection of anomalies that require further review. The companion website provides access to a demo version of IDEA, along with sample scripts that allow readers to immediately test the procedures from the book.

Business systems' electronic databases have grown tremendously with the rise of big data, and will continue to increase at significant rates. Fraudulent transactions are easily hidden in these enormous datasets, but Fraud and Fraud Detection helps readers gain the data analytics skills that can bring these anomalies to light. Step-by-step instruction and practical advice provide the specific abilities that will enhance the audit and investigation process. Readers will learn to:

Understand the different areas of fraud and their specific detection methods

Identify anomalies and risk areas using computerized techniques

Develop a step-by-step plan for detecting fraud through data analytics

Utilize IDEA software to automate detection and identification procedures

The delineation of detection techniques for each type of fraud makes this book a must-have for students and new fraud prevention professionals, and the step-by-step guidance to automation and complex analytics will prove useful for even experienced examiners. With datasets growing exponentially, increasing both the speed and sensitivity of detection helps fraud professionals stay ahead of the game. Fraud and Fraud Detection is a guide to more efficient, more effective fraud identification.

Häufig gestellte Fragen

Wie kann ich mein Abo kündigen?

Gehe einfach zum Kontobereich in den Einstellungen und klicke auf „Abo kündigen“ – ganz einfach. Nachdem du gekündigt hast, bleibt deine Mitgliedschaft für den verbleibenden Abozeitraum, den du bereits bezahlt hast, aktiv. Mehr Informationen hier.

(Wie) Kann ich Bücher herunterladen?

Derzeit stehen all unsere auf Mobilgeräte reagierenden ePub-Bücher zum Download über die App zur Verfügung. Die meisten unserer PDFs stehen ebenfalls zum Download bereit; wir arbeiten daran, auch die übrigen PDFs zum Download anzubieten, bei denen dies aktuell noch nicht möglich ist. Weitere Informationen hier.

Welcher Unterschied besteht bei den Preisen zwischen den Aboplänen?

Mit beiden Aboplänen erhältst du vollen Zugang zur Bibliothek und allen Funktionen von Perlego. Die einzigen Unterschiede bestehen im Preis und dem Abozeitraum: Mit dem Jahresabo sparst du auf 12 Monate gerechnet im Vergleich zum Monatsabo rund 30 %.

Was ist Perlego?

Wir sind ein Online-Abodienst für Lehrbücher, bei dem du für weniger als den Preis eines einzelnen Buches pro Monat Zugang zu einer ganzen Online-Bibliothek erhältst. Mit über 1 Million Büchern zu über 1.000 verschiedenen Themen haben wir bestimmt alles, was du brauchst! Weitere Informationen hier.

Unterstützt Perlego Text-zu-Sprache?

Achte auf das Symbol zum Vorlesen in deinem nächsten Buch, um zu sehen, ob du es dir auch anhören kannst. Bei diesem Tool wird dir Text laut vorgelesen, wobei der Text beim Vorlesen auch grafisch hervorgehoben wird. Du kannst das Vorlesen jederzeit anhalten, beschleunigen und verlangsamen. Weitere Informationen hier.

Ist Fraud and Fraud Detection als Online-PDF/ePub verfügbar?

Ja, du hast Zugang zu Fraud and Fraud Detection von Sunder Gee im PDF- und/oder ePub-Format sowie zu anderen beliebten Büchern aus Betriebswirtschaft & Buchhaltung. Aus unserem Katalog stehen dir über 1 Million Bücher zur Verfügung.

ORGANIZATIONS GENERATE AND RETAIN more information stored in electronic format than ever before, yet even though there is more analysis performed with the available data, fraud persists. With such vast amounts of data, abusive scheme transactions are hidden and are difficult to detect by traditional means. Data analytics can assist in uncovering signs of potential fraud with the aid of software to sort through large amounts of data to highlight anomalies.

This book will help you understand fraud and the different types of occupational fraud schemes. Specific data analytical tests are demonstrated along with suggested tests on how to uncover these frauds through the use of data analytics.

DEFINING FRAUD

A short definition of fraud is outlined in Black’s Law Dictionary:

An act of intentional deception or dishonesty perpetrated by one or more individuals, generally for financial gain.1

This simple definition mandates a number of elements that must be addressed in order to prove fraud:

The statement must be false and material.

The individual must know that the statement is untrue.

The intent to deceive the victim.

The victim relied on the statement.

The victim is injured financially or otherwise.

The false statement must substantially impact the victim’s decision to proceed with the transaction and that perpetrator must know the statement is false. A simple error or mistake is not fraudulent when it is not made to mislead the victim. The victim reasonably relied on the statement that caused injury to the victim or placed him or her at a disadvantage.

It is intentional deception that induces the victim to take a course of action that results in a loss that distinguishes the theft act.

In addition to the employer suffering a financial or other loss, occupational fraud involves an employee violating the trust associated with the job and hiding the fraud. The employee takes action to conceal the fraud and hopes it will not be discovered at all or until it is too late.

The word abuse is employed when the elements for defining fraud do not explicitly exist. In terms of occupational abuse, common examples include actions of employees:

Accessing Internet sites such as Facebook and eBay for personal reasons.

Taking a sick day when not sick.

Making personal phone calls.

Deliberately underperforming.

Taking office supplies for personal use.

Not earning the day’s pay while working offsite or telecommuting.

There is an endless list that can fall under the term abuse, but no reasonable employer would use this word to describe any employee unless the actions were excessive. Organizations may have policies in place for some of these items, such as an Acceptable Internet Use Policy, but most would be considered on a case-by-case basis, as the issue is a matter of degree that can be highly subjective. There would unlikely be any legal actions taken against an employee who participated in a mild form of abuse.

ANOMALIES VERSUS FRAUD

In the data analysis process, “Detecting a fraud is like finding the proverbial needle in the haystack.”2 Typically, fraudulent transactions in electronic records are few in relation to the large amount of records in data sets. Fraudulent transactions are not the norm. Other anomalies, such as accounting records anomalies, are due to inadequate procedures or other internal control weaknesses. These weaknesses would be repetitive and will occur frequently in the data set. Sometimes, they would regularly and consistently happen at specific intervals, such as at month- or year-end. Understanding the business and its practices and procedures helps to explain most anomalies.

TYPES OF FRAUD

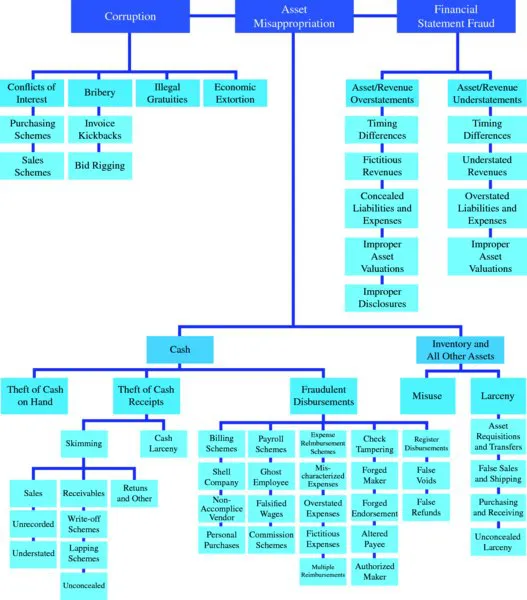

The Association of Certified Fraud Examiners (ACFE) in the 2012 Report to the Nations3 outlines the three categories of occupational fraud and their subcategories in Figure 1.1.

Figure 1.1 Occupational Fraud and Abuse Classification System

Source: Association of Certified Fraud Examiners

It was found that:

As in our previous studies, asset misappropriation schemes were by far the most common type of occupational fraud, comprising 87% of the cases reported to us; they were also the least costly form of fraud, with a median loss of $120,000. Financial statement fraud schemes made up just 8% of the cases in our study, but caused the greatest median loss at $1 million. Corruption schemes fell in the middle, occurring in just over one-third of reported cases and causing a median loss of $250,000.4

Among the three major categories—corruption, asset misappropriation, and financial statement fraud—there are far more types of occupational fraud in the asset-misappropriation category. There are many known schemes and areas where fraud may occur. Thefts of cash on hand have been occurring ever since there was cash. With globalization and the availability of the Internet, newer and more innovative types of fraud are coming to light.

An example is the case study published in Verizon’s security blog titled “Pro-Active Log Review Might Be a Good Idea.”5 A U.S .-based corporation had requested Verizon to assist them in reviewing virtual private network logs that showed an employee logging in from China while he was sitting at his desk in the United States. Investigation revealed that the employee had outsourced his job to a Chinese consulting firm at a fraction of his earnings. The employee spent most of his day on personal matters on the Internet. The blog notes that the employee’s performance reviews showed that “he received excellent remarks. His code was clean, well written, and submitted in a timely fashion. Quarter after quarter, his performance review noted him as the best developer in the buildin...