Frequently Asked Questions in International Standards on Auditing

Steven Collings

This is a test

This is a test

Buch teilen

English

ePUB (handyfreundlich)

Über iOS und Android verfügbar

eBook - ePub

Frequently Asked Questions in International Standards on Auditing

Steven Collings

Angaben zum Buch

Buchvorschau

Inhaltsverzeichnis

Quellenangaben

Über dieses Buch

Auditing has hit the headlines over recent years, and for all the wrong reasons, and in today's environment, the result of negligent auditing can be serious resulting in sizeable fines and even withdrawal of audit registration which can be costly in terms of fee income.

Frequently Asked Questions in International Standards on Auditing presents the relevant standards in a concise and jargon-free way, enabling auditors to appreciate the reasoning behind the standards and undertake audit work effectively. This book focuses on the main areas of the auditing standards and also addresses some key areas where audit firms are failing and which have been flagged up by audit regulators. The FAQs cover the main parts of each standard, and each question will be answered in a practical context, with worked examples showing how the standards are applied in real situations.

Häufig gestellte Fragen

Wie kann ich mein Abo kündigen?

Gehe einfach zum Kontobereich in den Einstellungen und klicke auf „Abo kündigen“ – ganz einfach. Nachdem du gekündigt hast, bleibt deine Mitgliedschaft für den verbleibenden Abozeitraum, den du bereits bezahlt hast, aktiv. Mehr Informationen hier.

(Wie) Kann ich Bücher herunterladen?

Derzeit stehen all unsere auf Mobilgeräte reagierenden ePub-Bücher zum Download über die App zur Verfügung. Die meisten unserer PDFs stehen ebenfalls zum Download bereit; wir arbeiten daran, auch die übrigen PDFs zum Download anzubieten, bei denen dies aktuell noch nicht möglich ist. Weitere Informationen hier.

Welcher Unterschied besteht bei den Preisen zwischen den Aboplänen?

Mit beiden Aboplänen erhältst du vollen Zugang zur Bibliothek und allen Funktionen von Perlego. Die einzigen Unterschiede bestehen im Preis und dem Abozeitraum: Mit dem Jahresabo sparst du auf 12 Monate gerechnet im Vergleich zum Monatsabo rund 30 %.

Was ist Perlego?

Wir sind ein Online-Abodienst für Lehrbücher, bei dem du für weniger als den Preis eines einzelnen Buches pro Monat Zugang zu einer ganzen Online-Bibliothek erhältst. Mit über 1 Million Büchern zu über 1.000 verschiedenen Themen haben wir bestimmt alles, was du brauchst! Weitere Informationen hier.

Unterstützt Perlego Text-zu-Sprache?

Achte auf das Symbol zum Vorlesen in deinem nächsten Buch, um zu sehen, ob du es dir auch anhören kannst. Bei diesem Tool wird dir Text laut vorgelesen, wobei der Text beim Vorlesen auch grafisch hervorgehoben wird. Du kannst das Vorlesen jederzeit anhalten, beschleunigen und verlangsamen. Weitere Informationen hier.

Ist Frequently Asked Questions in International Standards on Auditing als Online-PDF/ePub verfügbar?

Ja, du hast Zugang zu Frequently Asked Questions in International Standards on Auditing von Steven Collings im PDF- und/oder ePub-Format sowie zu anderen beliebten Büchern aus Betriebswirtschaft & Wirtschaftsprüfung. Aus unserem Katalog stehen dir über 1 Million Bücher zur Verfügung.

Chapter 1 What is the Role of the International Auditing and Assurance Standards Board?

The International Auditing and Assurance Standards Board (IAASB) is responsible for setting the International Standards on Auditing (ISAs). It is an independent standard-setting body that sets high-quality, international standards on aspects of:

Auditing;

Assurance;

Quality control;

Review; and

Related services.

The IAASB was founded in March 1978 and was previously known as the International Auditing Practices Committee (IAPC) whose work was then focused on three areas, namely:

Objects and scope of audits of financial statements;

Engagement letters; and

General auditing guidelines.

As one can appreciate, the work of the IAASB has significantly evolved and in 1991 the IAPC's guidelines were renamed the International Standards on Auditing.

In 2002, the IAPC changed its name to the IAASB and the International Federation of Accountants (IFAC) approved a series of reforms that were primarily designed (among other things) to strengthen the standard-setting process, which included the processes at the IAASB, in order to best serve the public interest.

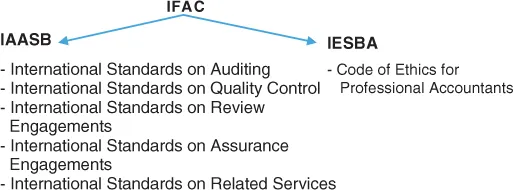

The IAASB is a technical standing committee of IFAC which is also closely linked to the International Ethics Standards Board for Accountants (IESBA) which produces the Code of Ethics for Professional Accountants. An illustration of the hierarchy is as follows:

The standards issued above by the IAASB are authoritative material (as stated in the Preface to International Standards on Quality Control, Auditing, Assurance and Related Services Pronouncements (Revised 2011)). As these standards are authoritative, they must be followed in an audit that is conducted in accordance with the ISAs.

In addition to ‘authoritative’ material published by the IAASB, they also publish ‘non-authoritative’ materials which offer a form of ‘guidance’ rather than mandatory requirements. These are:

International Auditing Practices Notes (IAPNs). These are designed to provide practical assistance to auditors rather than impose mandatory requirements.

Practice Notes Relating to Other International Standards.

Staff Publications: these are designed to raise awareness of new or emerging issues in relation to the standards and to direct attention to the relevant parts of IAASB pronouncements.

Some jurisdictions will have their own standard-setting bodies. For example, the Financial Reporting Council is responsible for standard-setting in the UK. Some countries do adopt ISAs but have to amend them to be country-specific. For example, in the UK, ISAs are adopted but are amended in some areas to be compatible with UK practices and these are then referred to as ISA (UK and Ireland).

Example

ISA 570 Going Concern requires the auditor to consider whether management have made a going concern assessment which covers a period of 12 months from the date of the financial statements. However, in the UK and Ireland, this going concern assessment should cover a period of 12 months from the date of approval (or expected date of approval) of the financial statements.

The UK and Ireland ISA therefore covers a different time span which demonstrates how the standard-setters have amended the mainstream ISA to be specific to the UK and Ireland. In the UK the going concern ISA is known as ISA (UK and Ireland) 570 Going Concern. In the UK and Ireland ISAs are often coined ‘ISA pluses’ because they contain additional or amended requirements to the mainstream ISA issued by the IAASB.

The Clarity Project

In 2004, the IAASB undertook a programme in which the objective was to enhance the clarity of the ISAs. The overall aim of this Clarity Project was to enhance the understandability of the ISAs which would, in turn, enable consistent application of the standards and go to improve overall audit quality on a worldwide level. This was an important exercise following some well-publicised corporate disasters and the decimation of confidence within the auditing profession.

Following the Clarity Project, each standard now has a clear structure with transparent objectives, definitions and requirements, together with application and other explanatory material which drill down further into the requirements of the ISAs. The structure of the new standards makes it easier to understand what is required and what is guidance. In addition, ISQC 1 Q...