The book provides a rigorous introduction to corporate finance and the valuation of equity. The first half of the book covers much of the received theory in these areas such as the relationship between the risk of an equity security and the return one can expect from it, the effects of leverage (that is, the borrowing policies of the firm) on the return one can expect from the firm's shares and the role that dividends, operating cash flows and accounting earnings play in the valuation of equity. The second half of the book is more advanced and deals with the important role that "real options" (that is, as yet unexploited investment opportunities) play in the valuation of equity.

Preguntas frecuentes

¿Cómo cancelo mi suscripción?

Simplemente, dirígete a la sección ajustes de la cuenta y haz clic en «Cancelar suscripción». Así de sencillo. Después de cancelar tu suscripción, esta permanecerá activa el tiempo restante que hayas pagado. Obtén más información aquí.

¿Cómo descargo los libros?

Por el momento, todos nuestros libros ePub adaptables a dispositivos móviles se pueden descargar a través de la aplicación. La mayor parte de nuestros PDF también se puede descargar y ya estamos trabajando para que el resto también sea descargable. Obtén más información aquí.

¿En qué se diferencian los planes de precios?

Ambos planes te permiten acceder por completo a la biblioteca y a todas las funciones de Perlego. Las únicas diferencias son el precio y el período de suscripción: con el plan anual ahorrarás en torno a un 30 % en comparación con 12 meses de un plan mensual.

¿Qué es Perlego?

Somos un servicio de suscripción de libros de texto en línea que te permite acceder a toda una biblioteca en línea por menos de lo que cuesta un libro al mes. Con más de un millón de libros sobre más de 1000 categorías, ¡tenemos todo lo que necesitas! Obtén más información aquí.

¿Perlego ofrece la función de texto a voz?

Busca el símbolo de lectura en voz alta en tu próximo libro para ver si puedes escucharlo. La herramienta de lectura en voz alta lee el texto en voz alta por ti, resaltando el texto a medida que se lee. Puedes pausarla, acelerarla y ralentizarla. Obtén más información aquí.

¿Es Principles of Equity Valuation un PDF/ePUB en línea?

Sí, puedes acceder a Principles of Equity Valuation de Ian Davidson, Mark Tippett en formato PDF o ePUB, así como a otros libros populares de Negocios y empresa y Negocios en general. Tenemos más de un millón de libros disponibles en nuestro catálogo para que explores.

1 The measurement of returns on bonds, equities and other financial instruments

§1-1. The calculation and indeed, the manipulation of returns pervades our everyday lives. When one opens a bank account or line of credit with a financial institution, the rate of interest on surplus funds and/or the rate of interest on the overdraft facilities we expect to use figure highly in the decisions we make about which bank/and or financial institution we will lend our custom to. When it comes to risky assets such as the shares and bonds of publicly listed companies, we make investment decisions by weighing the returns we expect to get from our proposed investments against the risks that are likely to arise from them. Our retirement plans also hinge crucially on the returns earned by the superannuation funds with which we deposit our retirement funds and on the prospective benefits these returns will enable us to enjoy after we retire. All of this presupposes of course that we have a clear understanding of how the returns on a given portfolio or financial instrument ought to be calculated. Hence, the principal brief of this chapter is to identify the pitfalls that may arise from the incorrect calculation and averaging of the returns that accrue on shares, bonds, portfolios and other financial instruments. We begin our analysis with a consideration of the procedures that can be used to compute the returns on bonds.

§1-2. A bond is a written contract by a debtor to pay a creditor a redemption payment V on an indicated date and to pay a pre-specified amount K (normally termed interest) on a periodic basis. The typical bond mentions a borrowed principal H, called the face value or par value of the bond. Bonds typically make interest payments on a semi-annual basis and are redeemable at par – in which case V = H. Consider, then, the purchaser of a bond who demands that his money be invested at a pre-specified rate r. We call this the investment rate. The price the investor will pay for the bond is given by

the present value of the final redemption payment (V) plus the present value of the remaining interest payments (K)

One can demonstrate how this valuation formula is implemented using the following simple example.

An H = £100 par 6 per cent bond pays interest on a semi-annual basis. This means that interest of K = (0.06/2) × H = 0.03 × £100 = £3 is paid at the mid-point of the year and also at the end of year until such time as the bond is redeemed. The bond is to be redeemed on 30 June 2012. Determine the price to be paid for the bond if (a) the bond is purchased on 1 July 2009, (b) the investment rate is 2 per cent (per half year); that is, r = 4 per cent (per annum) compounded semi-annually and (c) the bond is redeemable at par; that is V = £100 = H. Now the present value of £100 receivable in three years’ time, compounded at 4 per cent (per annum) compounded semi-annually, is

Likewise, the present value of the interest payments compounded at 4 per cent (per annum) compounded semi-annually is

Hence, the investor would be prepared to pay no more than (£88.80+£16.80) = £105.60 for the bond.

§1-3. The rate of interest quoted on a bond is normally what is known as the nominal rate of interest. With a given nominal rate r, compounded m times per year, we define the corresponding effective rate of interest to be the rate that would apply if compounding occurred on an annual basis only. One can demonstrate this point by supposing for the example given in §1-2 above that the investment rate is 4.04 per cent compounded annually. We would then have that the present value of £100 receivable in three years’ time, compounded at an annual rate of 4.04 per cent, would be

Likewise, the present value of the interest payments compounded at an annual rate of 4.04 per cent will be

Hence, the value of the bond is again (£88.80 + £16.80) = £105.60, i.e. the same value as calculated in §1-2 above. This implies that an interest rate of 4 per cent (per annum) compounded semi-annually is equivalent to an interest rate of 4.04 per cent compounded annually. In other words, an effective rate of interest of 4.04 per cent corresponds to a nominal rate of interest of 4 per cent (per annum) compounded semi-annually. The effective rate of interest is often called the Annual Percentage Rate or APR for short. We develop the relationship between the nominal rate of interest and the effective rate of interest (or APR) in further detail in §1-7 below.

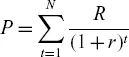

§1-4. Suppose I have to repay a loan and I want to confirm the integrity or otherwise of the figures that have been given to me by the lending institution. The principles just enunciated for bond valuation may also be applied here. The present value of the repayments on the loan must be equal to the amount borrowed, or

where P is the principal (or the amount) borrowed, N is the number of repayments that will be made on the loan, R is the periodic repayment and r is the investment rate on the loan. One can demonstrate the application of this formula by considering a person who takes out a loan of £2,000 that is to be repaid in 12 equal monthly instalments. The borrowing (investment) rate is 18 per cent (per annum). It thus follows that P = £2,000, r = 0.18/12 = 0.015 or 1