The book provides a rigorous introduction to corporate finance and the valuation of equity. The first half of the book covers much of the received theory in these areas such as the relationship between the risk of an equity security and the return one can expect from it, the effects of leverage (that is, the borrowing policies of the firm) on the return one can expect from the firm's shares and the role that dividends, operating cash flows and accounting earnings play in the valuation of equity. The second half of the book is more advanced and deals with the important role that "real options" (that is, as yet unexploited investment opportunities) play in the valuation of equity.

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

1 The measurement of returns on bonds, equities and other financial instruments

§1-1. The calculation and indeed, the manipulation of returns pervades our everyday lives. When one opens a bank account or line of credit with a financial institution, the rate of interest on surplus funds and/or the rate of interest on the overdraft facilities we expect to use figure highly in the decisions we make about which bank/and or financial institution we will lend our custom to. When it comes to risky assets such as the shares and bonds of publicly listed companies, we make investment decisions by weighing the returns we expect to get from our proposed investments against the risks that are likely to arise from them. Our retirement plans also hinge crucially on the returns earned by the superannuation funds with which we deposit our retirement funds and on the prospective benefits these returns will enable us to enjoy after we retire. All of this presupposes of course that we have a clear understanding of how the returns on a given portfolio or financial instrument ought to be calculated. Hence, the principal brief of this chapter is to identify the pitfalls that may arise from the incorrect calculation and averaging of the returns that accrue on shares, bonds, portfolios and other financial instruments. We begin our analysis with a consideration of the procedures that can be used to compute the returns on bonds.

§1-2. A bond is a written contract by a debtor to pay a creditor a redemption payment V on an indicated date and to pay a pre-specified amount K (normally termed interest) on a periodic basis. The typical bond mentions a borrowed principal H, called the face value or par value of the bond. Bonds typically make interest payments on a semi-annual basis and are redeemable at par – in which case V = H. Consider, then, the purchaser of a bond who demands that his money be invested at a pre-specified rate r. We call this the investment rate. The price the investor will pay for the bond is given by

the present value of the final redemption payment (V) plus the present value of the remaining interest payments (K)

One can demonstrate how this valuation formula is implemented using the following simple example.

An H = £100 par 6 per cent bond pays interest on a semi-annual basis. This means that interest of K = (0.06/2) × H = 0.03 × £100 = £3 is paid at the mid-point of the year and also at the end of year until such time as the bond is redeemed. The bond is to be redeemed on 30 June 2012. Determine the price to be paid for the bond if (a) the bond is purchased on 1 July 2009, (b) the investment rate is 2 per cent (per half year); that is, r = 4 per cent (per annum) compounded semi-annually and (c) the bond is redeemable at par; that is V = £100 = H. Now the present value of £100 receivable in three years’ time, compounded at 4 per cent (per annum) compounded semi-annually, is

Likewise, the present value of the interest payments compounded at 4 per cent (per annum) compounded semi-annually is

Hence, the investor would be prepared to pay no more than (£88.80+£16.80) = £105.60 for the bond.

§1-3. The rate of interest quoted on a bond is normally what is known as the nominal rate of interest. With a given nominal rate r, compounded m times per year, we define the corresponding effective rate of interest to be the rate that would apply if compounding occurred on an annual basis only. One can demonstrate this point by supposing for the example given in §1-2 above that the investment rate is 4.04 per cent compounded annually. We would then have that the present value of £100 receivable in three years’ time, compounded at an annual rate of 4.04 per cent, would be

Likewise, the present value of the interest payments compounded at an annual rate of 4.04 per cent will be

Hence, the value of the bond is again (£88.80 + £16.80) = £105.60, i.e. the same value as calculated in §1-2 above. This implies that an interest rate of 4 per cent (per annum) compounded semi-annually is equivalent to an interest rate of 4.04 per cent compounded annually. In other words, an effective rate of interest of 4.04 per cent corresponds to a nominal rate of interest of 4 per cent (per annum) compounded semi-annually. The effective rate of interest is often called the Annual Percentage Rate or APR for short. We develop the relationship between the nominal rate of interest and the effective rate of interest (or APR) in further detail in §1-7 below.

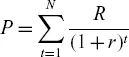

§1-4. Suppose I have to repay a loan and I want to confirm the integrity or otherwise of the figures that have been given to me by the lending institution. The principles just enunciated for bond valuation may also be applied here. The present value of the repayments on the loan must be equal to the amount borrowed, or

where P is the principal (or the amount) borrowed, N is the number of repayments that will be made on the loan, R is the periodic repayment and r is the investment rate on the loan. One can demonstrate the application of this formula by considering a person who takes out a loan of £2,000 that is to be repaid in 12 equal monthly instalments. The borrowing (investment) rate is 18 per cent (per annum). It thus follows that P = £2,000, r = 0.18/12 = 0.015 or 1

per cent (per month), and N = 12. Sub...

Table of contents

Cover

Half title

Title

Copyright

Dedication

Contents

List of Figures

List of Tables

Preface

Acknowledgements

Introduction

1. The measurement of returns on bonds, equities and other financial instruments

2. The relationship between return and risk

3. Alternative approaches to the relationship between return and risk

4. Returns and the capital structure of the firm

5. The relationship between equity value, dividends and other cash flow streams

6. The relationship between book (accounting) rates of return and the cost of capital for firms and capital projects

12. Equity valuation: higher-order investment opportunity sets, momentum and acceleration

Index

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go. Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Principles of Equity Valuation by Ian Davidson,Mark Tippett in PDF and/or ePUB format, as well as other popular books in Business & Business General. We have over 1.5 million books available in our catalogue for you to explore.