Deploying Computer Algorithms to Conquer the Markets

Ernest P. Chan

This is a test

This is a test

Compartir libro

English

ePUB (apto para móviles)

Disponible en iOS y Android

eBook - ePub

Machine Trading

Deploying Computer Algorithms to Conquer the Markets

Ernest P. Chan

Detalles del libro

Vista previa del libro

Índice

Citas

Información del libro

Dive into algo trading with step-by-step tutorials and expert insight

Machine Trading is a practical guide to building your algorithmic trading business. Written by a recognized trader with major institution expertise, this book provides step-by-step instruction on quantitative trading and the latest technologies available even outside the Wall Street sphere. You'll discover the latest platforms that are becoming increasingly easy to use, gain access to new markets, and learn new quantitative strategies that are applicable to stocks, options, futures, currencies, and even bitcoins. The companion website provides downloadable software codes, and you'll learn to design your own proprietary tools using MATLAB. The author's experiences provide deep insight into both the business and human side of systematic trading and money management, and his evolution from proprietary trader to fund manager contains valuable lessons for investors at any level.

Algorithmic trading is booming, and the theories, tools, technologies, and the markets themselves are evolving at a rapid pace. This book gets you up to speed, and walks you through the process of developing your own proprietary trading operation using the latest tools.

Utilize the newer, easier algorithmic trading platforms

Access markets previously unavailable to systematic traders

Adopt new strategies for a variety of instruments

Gain expert perspective into the human side of trading

The strength of algorithmic trading is its versatility. It can be used in any strategy, including market-making, inter-market spreading, arbitrage, or pure speculation; decision-making and implementation can be augmented at any stage, or may operate completely automatically. Traders looking to step up their strategy need look no further than Machine Trading for clear instruction and expert solutions.

Preguntas frecuentes

¿Cómo cancelo mi suscripción?

Simplemente, dirígete a la sección ajustes de la cuenta y haz clic en «Cancelar suscripción». Así de sencillo. Después de cancelar tu suscripción, esta permanecerá activa el tiempo restante que hayas pagado. Obtén más información aquí.

¿Cómo descargo los libros?

Por el momento, todos nuestros libros ePub adaptables a dispositivos móviles se pueden descargar a través de la aplicación. La mayor parte de nuestros PDF también se puede descargar y ya estamos trabajando para que el resto también sea descargable. Obtén más información aquí.

¿En qué se diferencian los planes de precios?

Ambos planes te permiten acceder por completo a la biblioteca y a todas las funciones de Perlego. Las únicas diferencias son el precio y el período de suscripción: con el plan anual ahorrarás en torno a un 30 % en comparación con 12 meses de un plan mensual.

¿Qué es Perlego?

Somos un servicio de suscripción de libros de texto en línea que te permite acceder a toda una biblioteca en línea por menos de lo que cuesta un libro al mes. Con más de un millón de libros sobre más de 1000 categorías, ¡tenemos todo lo que necesitas! Obtén más información aquí.

¿Perlego ofrece la función de texto a voz?

Busca el símbolo de lectura en voz alta en tu próximo libro para ver si puedes escucharlo. La herramienta de lectura en voz alta lee el texto en voz alta por ti, resaltando el texto a medida que se lee. Puedes pausarla, acelerarla y ralentizarla. Obtén más información aquí.

¿Es Machine Trading un PDF/ePUB en línea?

Sí, puedes acceder a Machine Trading de Ernest P. Chan en formato PDF o ePUB, así como a otros libros populares de Business y Finance. Tenemos más de un millón de libros disponibles en nuestro catálogo para que explores.

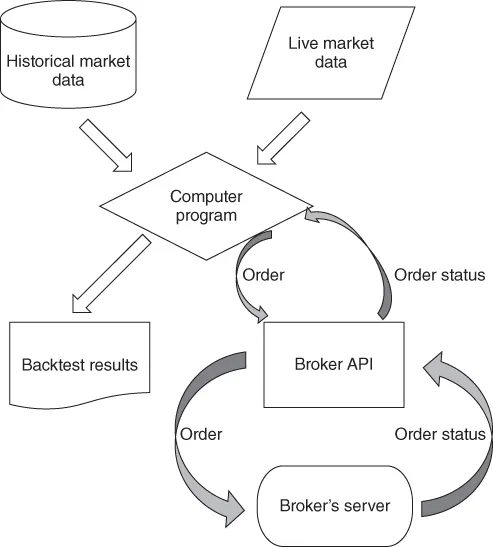

An algorithmic trading strategy feeds market data (historical or live) into a computer (backtest or automated execution) program. The program then submits orders to the broker through an API, and receives order status notifications back from the broker. The flowchart in Figure 1.1 illustrates this process.

Figure 1.1 Algorithmic trading at a glance

Notice that I deliberately use the same box to indicate the computer program that generates backtest results and live orders: This is the best way to ensure we are trading the exact same model that we have backtested.

In this chapter, I will discuss the latest services, products, and their vendors applicable to each of the blocks in Figure 1.1. In addition, I will describe my favorite performance metrics, the way to determine the optimal leverage, and the simplest asset allocation method. Though I have touched on many (but not all) of these issues in my previous books, I have updated them here based on the state of the art. The FinTech industry has not been standing still, nor has my understanding of issues ranging from brokers' safety to subtleties of portfolio optimization.

Historical Market Data

For daily historical data in stocks and futures, I have been using CSI (csidata.com) for a long time. CSI has a very flexible, and robust, desktop application. The beauty of this application is that we can set a time in the evening when the data are automatically updated through an Internet connection with CSI's server. Also, the data can be stored in various convenient formats such as .txt, .csv, or .xlsx. We can ask it to automatically adjust historical stock (and ETF) prices for splits and dividends. For a little extra, CSI can also provide delisted stocks' historical data, so that you can have a survivorship‐bias‐free data set.1 (By the way, CSI data powers Yahoo! Finance's historical stock data.) For futures, we can choose different rollover methods to create continuous contracts. Or not, since the original contract prices are also available, and many professional traders prefer to backtest futures using original contract prices instead of back‐adjusted continuous contract prices. This is because the latter depends on a particular roll method, and may have look‐ahead bias embedded (see Chan, 2013, for a detailed exploration of this issue). Finally, CSI has excellent customer support through email and phone.

An alternative to CSI is Quandl.com, which is a consolidator of many kinds of data from many different vendors. It also provides an API in different languages (including MATLAB, which I use in this book, or Python, which many other traders use) that we can use for data selection and download. Some of Quandl's data are free (daily data for stocks is one example), and others require payment. I have purchased, for example, fundamental stock data from them (see Chapter 2, Factor Models), and they are much more economical than established vendors such as Compustat.

Serious traders or academic finance researchers may prefer stock, ETF, and mutual fund data from CRSP (www.crsp.com). Their historical data are carefully compiled to be survivorship‐bias‐free, and dividends and splits are provided separately so you can decide how to utilize them in a backtest. But most importantly, they provide the best bid and offer (BBO) prices at the close. These are important because, as is explained in Box 6.4 in Chapter 6, using the usual consolidated closing prices from CSI or Quandl can inflate backtest performances for certain strategies. A similar issue arises from using the consolidated opening prices. The best open and close prices to use are the auction prices from the primary exchange. (See also Box 6.4 for an explanation of how we can extract such auction prices from tick data.) The second best open and close prices to use are the BBO prices that can be used to compute the midprices at the open and close. Unfortunately CRSP does not provide the BBO prices at the open, so one must use intraday data for that purpose. For academic researchers, CRSP data can be obtained at a lower cost through WRDS (wrds‐web.wharton.upenn.edu), which is a consolidator of many high quality historical databases for scholarly research.

Of course, those serious traders who can afford to buy data from CRSP may also be able to afford a Bloomberg terminal subscription. One advantage of a Bloomberg terminal is that we can download the “primary exchange” close price for US stocks. Of course, a Bloomberg subscription also includes access to many historical and live data spanning a wide variety of instruments and, importantly, breaking news on every stock. I have found Bloomberg's news service to be superior to many other vendors'. Often, we will see a stock moves suddenly, and are not able to find the reason anywhere else but on Bloomberg's news feed. They do capture the most obscure news on the most obscure stocks in the shortest time frame, which is important when you have an event‐driven strategy. Bloomberg's historical US stock data are also survivorship‐bias‐free. (To be fair ...