Navigate M&A accounting arbitrations with insider perspective

M&A Disputes takes you inside the dispute resolution process to help you put together the many "moving parts" necessary to obtain a successful outcome. With deep insight from experts in the field—including valuable advice from the arbitrator's perspective—this book guides you through the entire process to explore the variables at work. The high volume of M&A transactions makes post-closing price adjustment provisions and accounting arbitrations a critical part of doing business. Yet, the field is opaque to non-practitioners and important issues can be easily misunderstood without specific knowledge and experience. A resulting award can make or break a transaction; an intimate understanding of the process's inner working can help you plan your position to the greatest advantage. This book explores the many factors that that contribute to a successful resolution across the entire transaction life cycle from contract negotiation through the dispute phase including due diligence, determination of the target net working capital, conception and closing of the purchase agreement, post-closing negotiation and dispute resolution, the impact of accounting practices, guidance, and documentation as well as relevant auditing concepts, and various facts and circumstances surrounding the target business and the transaction that need to be considered.

M&A volume remains high and continues to result in large numbers of current and future post-closing M&A disputes. Clients rely on their attorneys and advisers to guide them through the process and counsel them toward a positive outcome. Those professionals will find that M&A accounting arbitrations carry a range of distinctions that require a specialized knowledge base to navigate correctly. This book provides real-world guidance from experts in the field, with invaluable insight for every stage of the process.

Walk through the entire dispute resolution process from arbitrator selection through final award

Understand how M&A agreement provisions impact the awarded amount as well as the options available to limit the scope of potential disputes and the "gaming" of the post-closing process by the counterparty

Understand the nature of accounting estimates and guidance, their interaction with accounting arbitrations, and how to synthesize facts, circumstances, and GAAP into a persuasive argument to present to the accounting arbitrator

Get situation-specific advice for different types of transactions

Learn practitioner "dos" and "don'ts" from the arbitrator's perspective

M&A Disputes provides transaction parties and their representatives an inside view at the transaction and commonly disputed items through the eyes of the arbitrator to provide them with uniquely valuable insight.

In addition to being an invaluable tool for practitioners appearing before an accounting arbitrator, M&A Disputes also provides advice to would-be and experienced arbitrators alike to successfully resolve disputes that can be significant and complex.

Foire aux questions

Comment puis-je résilier mon abonnement ?

Il vous suffit de vous rendre dans la section compte dans paramètres et de cliquer sur « Résilier l’abonnement ». C’est aussi simple que cela ! Une fois que vous aurez résilié votre abonnement, il restera actif pour le reste de la période pour laquelle vous avez payé. Découvrez-en plus ici.

Puis-je / comment puis-je télécharger des livres ?

Pour le moment, tous nos livres en format ePub adaptés aux mobiles peuvent être téléchargés via l’application. La plupart de nos PDF sont également disponibles en téléchargement et les autres seront téléchargeables très prochainement. Découvrez-en plus ici.

Quelle est la différence entre les formules tarifaires ?

Les deux abonnements vous donnent un accès complet à la bibliothèque et à toutes les fonctionnalités de Perlego. Les seules différences sont les tarifs ainsi que la période d’abonnement : avec l’abonnement annuel, vous économiserez environ 30 % par rapport à 12 mois d’abonnement mensuel.

Qu’est-ce que Perlego ?

Nous sommes un service d’abonnement à des ouvrages universitaires en ligne, où vous pouvez accéder à toute une bibliothèque pour un prix inférieur à celui d’un seul livre par mois. Avec plus d’un million de livres sur plus de 1 000 sujets, nous avons ce qu’il vous faut ! Découvrez-en plus ici.

Prenez-vous en charge la synthèse vocale ?

Recherchez le symbole Écouter sur votre prochain livre pour voir si vous pouvez l’écouter. L’outil Écouter lit le texte à haute voix pour vous, en surlignant le passage qui est en cours de lecture. Vous pouvez le mettre sur pause, l’accélérer ou le ralentir. Découvrez-en plus ici.

Est-ce que M&A Disputes est un PDF/ePUB en ligne ?

Oui, vous pouvez accéder à M&A Disputes par A. Vincent Biemans, Gerald M. Hansen en format PDF et/ou ePUB ainsi qu’à d’autres livres populaires dans Business et Fusioni e acquisizioni. Nous disposons de plus d’un million d’ouvrages à découvrir dans notre catalogue.

The purchase and sale of a business is typically an extensive process involving the identification of potential counterparties, due diligence, negotiation of a price and the purchase agreement, and finally the closing of the transaction. The closing represents the culmination of months of hard work often involving the assistance of a variety of advisors, including investment bankers, transaction counsel, and accountants.

The closing, however, does not necessarily mean that the transaction is fully completed and the purchase price is set. Many contracts governing the acquisition of a company or a business contain one or more mechanisms that allow for post‐closing adjustments to the purchase price based on a predetermined metric such as net working capital; earnings before interest, taxes, depreciation, and amortization (EBITDA); or some other metric. Such mechanisms and any resulting proposed purchase price adjustments may be resolved amicably between the parties. On the other hand, the adjustment process may lead to post‐closing disputes between the parties regarding the appropriate amount of the purchase price adjustment.

THE TRANSACTION LIFECYCLE

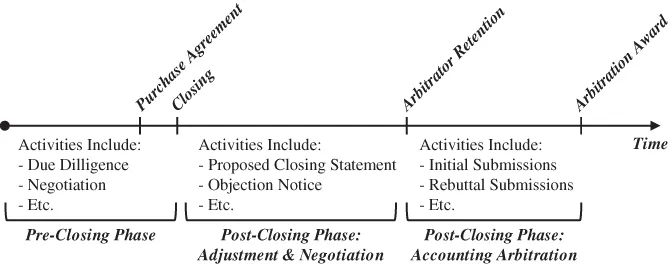

Purchase price adjustments are generally implemented after the closing of the transaction. The underlying mechanisms, however, are agreed upon prior to the closing. Moreover, the actual post‐closing adjustments may well find their genesis in pre‐closing events. Shown here is a sample representation of the lifecycle of a typical merger and acquisition transaction.

Sample Transaction Lifecycle with NWC Adjustment

M&A transactions can take a variety of forms and can follow varying timelines. Notwithstanding, the transaction lifecycle can generally be broken down into two major time periods—pre‐closing and post‐closing—with a variety of activities occurring in each period. For example, if the seller initiates the sales process, it may perform a variety of activities early on in the process to identify potential buyers and to get the company ready for sale. Once the field of potential buyers has narrowed, the parties can engage in further information exchanges, the buyer can perform its due diligence, and the parties can negotiate the purchase agreement.

The purchase agreement can incorporate both a negotiated purchase price amount (e.g., $1 billion) as well as a variety of adjustments that need to be made to arrive at the amount that is to ultimately be paid by the buyer. By means of example, the purchase price may be set on a debt free/cash free basis, that is, the agreed upon purchase price of $1 billion assumes the company has no debt and no cash. To arrive at the amount ultimately owed by the buyer, the company's debt and cash at closing have to be, respectively, deducted from and added to the negotiated purchase price amount (of $1 billion).

Transactions routinely provide for purchase price adjustments to be implemented post‐closing. For example, many purchase agreements contain a net working capital adjustment mechanism in order to have the final purchase price—i.e., after any post‐closing adjustments—reflect the actual amount of net working capital that was transferred with the business as of the closing date. Such adjustments are made post‐closing because, among other things, it is typically not possible to correctly quantify the net working capital on the closing date itself because of the time necessary to perform a typical “closing of the books.”

In such situations, the purchase agreement can provide for a preliminary closing statement based on which the preliminary purchase price is calculated and paid at closing. Subsequent to closing, the buyer is commonly contractually required to submit a proposed closing statement with updated net working capital amounts and any resulting purchase price adjustment. The seller may disagree with the buyer's calculations and send a—contractually provided for—objection notice. In the case of disagreement regarding any proposed adjustments, the purchase agreement commonly provides for negotiations between the parties, which are typically aided by the exchange of information between them.

In the event the parties cannot resolve the implementation of the purchase price adjustment between them, the purchase agreement may provide for the disputed items to be submitted to an accounting arbitrator for resolution. The dispute phase will typically at least involve the parties tendering initial and rebuttal submissions (with supporting documentation) to the accounting arbitrator for consideration and resolution of the dispute.

The focus of this book is on disputes arising after the closing of an M&A transaction and their resolution through accounting arbitration. Of course, the parties' pre‐closing activities can have an impact on the post‐closing purchase price adjustment process. For example, the level of sell‐side and buy‐side due diligence performed prior to closing can result in the preemptive identification and resolution of potential problem areas and, generally, increase the parties' knowledge of the accounting of the company being sold/acquired. Moreover, the negotiation of the purchase agreement and the precise language of its provisions can have a significant impact on the implementation of any purchase price adjustment mechanisms and the ultimate purchase price paid and received.

CATEGORIES OF PURCHASE PRICE ADJUSTMENT PROVISIONS

Contractual post‐closing purchase price adjustment mechanisms are found in purchase agreements that are structured as stock purchases as well as in those that are structured as asset purchases. Post‐closing purchase price adjustments can range from immaterial in the context of the transaction to large amounts that significantly impact the economics for the buyer and seller. There are three broad categories of potential contractual post‐closing adjustments to the purchase price:

Adjustments to the purchase price based on the financial position or performance of the target company as of or through the closing date

Adjustments to the purchase price based on the financial performance of the target company subsequent to the closing date

Adjustments to the purchase price based on the allocation of financial responsibility through representations, warranties, and indemnifications in the purchase agreement

Each of those categories of post‐closing adjustments can lead to disputes between the parties to the transaction. In addition to contractual purchase price adjustment disputes, there are also disputes related to the transaction and/or the purchase price that are based directly on the legal framework governing the transaction as opposed to the underlying contract. An example of a possible legal challenge that can lead to an adjustment to a share purchase price is a Delaware appraisal action. Another example of a legal challenge related to alleged under‐ or overpayment can be an action based on allegations of transaction fraud. Parties can also end up in dispute regarding a transaction that was never consummated based on, for example, allegations that one of the parties wrongfully failed to close. As this book focuses on accounting arbitrations, which generally find their basis in being preemptively agreed upon as a form of alternative dispute resolution, non‐contractual purchase price adjustment disputes are outside the scope of this book (although we discuss transaction fraud briefly in Chapter 22).

As it relates to contractual purchase price adjustments, agreements governing larger transactions generally contain at least a choice of law and forum selection clause. Many agreements, however, go much further and contain arbitration and/or expert determination clauses complete with prescribed procedures and an agreed‐upon timeline for dispute resolution. The agreed‐upon choices for alternative dispute resolution and the associated procedures can differ dependent on the nature of the potential dispute. In other words, one purchase agreement can contain multiple avenues for dispute resolution. For example, an agreement can simultaneously contain (i) an overall clause that prescribes New York law as the governing law and the federal court for the Southern District of New York as the venue of choice, (ii) an arbitration clause that arranges for an American Arbitration Association appointed arbitrator to decide any indemnification‐related disputes, and (iii) a clause that provides for an independent accountant to resolve any post‐closing net working capital disputes.

In general, the perceived benefits of alternative dispute resolution include the relative efficiency of the process, as it is often both faster and cheaper than traditional litigation, as well as the ability to tailor procedures and discovery. The limitations on discovery tend to be especially attractive to foreign transaction parties, for which the U.S. discovery process is often significantly more extensive than the obligations that are imposed by their home jurisdictions. In addition, especially in the event of a would‐be venue that is smaller and less used to foreign litigants, some foreign parties may fear that they would be at a disadvantage due to local biases. Of course, alternative dispute resolution also has downsides, including a commonly perceived tendency of arbitrators to arrive at split or compromise decisions as well as significant limitations on the ability to appeal an arbitration ruling. In the case of purchase price adjustment clauses, the efficiency benefits of alternative dispute resolution can be further increased by having, what are essentially, accounting disputes analyzed and decided by accountants.

The first category of purchase price adjustment disputes—adjustments based on the target company's financial position or performance as of or through the closing date—is as close as it gets to contract‐based pure accounting disputes. The underlying adjustment mechanisms include those based on the amounts of net working capital, debt (or net debt), and/or cash and cash equivalents that are transferred with the company at closing. The adjustment mechanisms can also incorporate performance measures...