The legal, financial, and business primer to the M&A process

Mergers and Acquisitions offers accessible step-by-step guidance through the M&A process to provide the legal and financial background required to navigate these deals successfully. From the initial engagement letter to the final acquisition agreement, this book delves into the mechanics of the process from beginning to end, favoring practical advice and actionable steps over theoretical concepts. Coverage includes deal structure, corporate structuring considerations, tax issues, public companies, leveraged buyouts, troubled businesses and more, with a uniquely solution-oriented approach to the M&A process. This updated second edition features new discussion on cross-border transactions and "pseudo" M&A deals, and the companion websites provides checklists and sample forms to facilitate organization and follow-through.

Mergers and acquisitions are complex, and problems can present themselves at each stage of the process; even if the deal doesn't fall through, you may still come out with less than you bargained for. This book is a multi-disciplinary primer for anyone navigating an M&A, providing the legal, financial, and business advice that helps you swing the deal your way.

Understand the legal mechanics of an M&A deal

Navigate the process with step-by-step guidance

Compare M&A structures, and the rationale behind each

Solve common issues and avoid transactional missteps

Do you know what action to take when you receive an engagement letter, confidentiality agreement, or letter of intent? Do you know when to get the banker involved, and how? Simply assuming the everything will work out well guarantees that it will—for the other side. Don't leave your M&A to chance; get the information and tools you need to get it done right. Mergers and Acquisitions guides you through the process step-by-step with expert insight and real-world advice.

Foire aux questions

Comment puis-je résilier mon abonnement ?

Il vous suffit de vous rendre dans la section compte dans paramètres et de cliquer sur « Résilier l’abonnement ». C’est aussi simple que cela ! Une fois que vous aurez résilié votre abonnement, il restera actif pour le reste de la période pour laquelle vous avez payé. Découvrez-en plus ici.

Puis-je / comment puis-je télécharger des livres ?

Pour le moment, tous nos livres en format ePub adaptés aux mobiles peuvent être téléchargés via l’application. La plupart de nos PDF sont également disponibles en téléchargement et les autres seront téléchargeables très prochainement. Découvrez-en plus ici.

Quelle est la différence entre les formules tarifaires ?

Les deux abonnements vous donnent un accès complet à la bibliothèque et à toutes les fonctionnalités de Perlego. Les seules différences sont les tarifs ainsi que la période d’abonnement : avec l’abonnement annuel, vous économiserez environ 30 % par rapport à 12 mois d’abonnement mensuel.

Qu’est-ce que Perlego ?

Nous sommes un service d’abonnement à des ouvrages universitaires en ligne, où vous pouvez accéder à toute une bibliothèque pour un prix inférieur à celui d’un seul livre par mois. Avec plus d’un million de livres sur plus de 1 000 sujets, nous avons ce qu’il vous faut ! Découvrez-en plus ici.

Prenez-vous en charge la synthèse vocale ?

Recherchez le symbole Écouter sur votre prochain livre pour voir si vous pouvez l’écouter. L’outil Écouter lit le texte à haute voix pour vous, en surlignant le passage qui est en cours de lecture. Vous pouvez le mettre sur pause, l’accélérer ou le ralentir. Découvrez-en plus ici.

Est-ce que Mergers and Acquisitions est un PDF/ePUB en ligne ?

Oui, vous pouvez accéder à Mergers and Acquisitions par Edwin L. Miller, Lewis N. Segall en format PDF et/ou ePUB ainsi qu’à d’autres livres populaires dans Law et Financial Law. Nous disposons de plus d’un million d’ouvrages à découvrir dans notre catalogue.

We will violate our initial promise of practicality by starting with a few pages on the corporate finance concepts underlying acquisitions and then a short section on the reasons for acquisitions.

Valuation Theory

At its simplest, there is really only one reason for a Buyer to do an acquisition: to make more money for its shareholders. A fancier way of expressing this is to create shareholder value, but that is not very precise or helpful. Creating shareholder value simply means making the acquirer's business more valuable. In an academic sense, how is the value of a business or asset theoretically determined?

At the most theoretical level, the value of a business (or an asset) is the economic present value of the future net cash generated by that business. Inflows are roughly equivalent to the operating cash flow component of the company's net income. Net income means the revenues of the business minus the expenses to run it determined on the accrual basis as described in the paragraphs that follow. There are other cash inflows and outflows that are not components of net income (e.g., cash investments in the business that are used to finance it). Also, a business's valuation is partially dependent on its balance sheet, which lists the company's assets and liabilities as of a point in time. In a purely theoretical sense, however, the balance sheet is relevant only for the net cash inflows and outflows that ultimately will result from the assets and liabilities shown. In other words, a balance sheet is a component of future net cash flow in the sense that the assets ultimately will be sold or otherwise realized, and the liabilities will take cash out of the business when they are paid.

An income statement looks pretty simple: Money in, money out over a period of time, not as of a particular point in time. But in order to truly understand an income statement, one must understand accrual basis accounting.

Cash flows are uneven and do not necessarily reflect the health of the business on a period‐to‐period basis. Accounting attempts to rectify this problem by employing the accrual method that puts cash flows in the period when the actual service or transaction occurs, not when cash is exchanged. A simple example is where you buy a widget‐making machine for $100 in year one and that machine generates $20 in cash each year for 10 years, at which point it can no longer be used. In evaluating the health of the business in year one, you would not look at it as the business losing $80 in that year ($20 minus the $100 cost of the machine) because you will not have to spend money to buy a new machine for another 9 years. So accrual accounting depreciates the machine by $10 per year for 10 years. Thus, the real income of the business is $10 in each year in our example ($20 of generated cash minus the $10 depreciation on the machine).

Ultimately, the intrinsic value of the business is, as already stated, the present value of all future net cash flows generated by the business. Because stock market analysts and others in part try to evaluate the ultimate value of the business, they would like to know what cash the business is generating in each accounting period. The reconciliation of the income statement to cash flow is contained in the statement of cash flows, which is one of the financial statements that are required to be presented to comply with generally accepted accounting principles (GAAP).

In valuing a business, you also have to consider the element of risk that is involved in generating the future cash flows that are to be discounted to present value. More precisely, the value of the business is the sum of each of the possible outcomes of net cash generated to infinity multiplied by the probability of achieving each one, then discounted to present value.

Take the example of a ski resort. The cash flows from the business looking out indefinitely are dependent on whether or not there is global warming. If there is no global warming, cash flows will be one thing; if there is, cash flows will be less. So, in valuing that business, we need to take an educated guess as to the likelihood of there being global warming. More generally, in valuing a business, you have to estimate the range of possible outcomes and their probabilities. This is what stock market analysts do for a living. Because it is not practical to value cash flows to infinity, analysts typically will look at projected cash flows over a period of five years, for example, and then add to that value the expected terminal value of the business at the end of the five years using another valuation method.

Comparing Investments

Another problem faced by an investor or an acquisitive Buyer is to analyze the desirability of one acquisition versus another by using common measures of return on investment. In reality, investments will be made, to the extent of available funds, in the opportunities that are better than the others, provided that the rate of return on those investments meets minimum standards.

So take our widget‐making machine example. The so‐called internal rate of return or yield on that investment of $100 in year one is computed algebraically by solving the following equation:

where r is the rate that discounts the stream of future cash flows to equal the initial outlay of 100 at time 0.

Another method is the net present value method where the cash inflows and outflows are discounted to present value. If you use a risk‐free interest rate as the discount rate, that tells you how much more your dollar of investment is worth, ignoring risk, than putting it in a government bond for the same period of time.

Element of Risk

Adding in the concept of risk makes things even more complicated. The term risk as used by financial analysts is a different concept from the probabilities that are used to produce the expected present value of the business. Risk is essentially the separate set of probabilities that the actual return will deviate from the expected return (i.e., the variability of the investment return).

In the economic sense, being risk averse does not mean that an investor is not willing to take risks. Whether the investor wants to or not, there are risks in everything. The first cut at an investment analysis is to take all of the possible negative and positive outcomes and then sum them, weighting each outcome by its probability. For most investors, that is not sufficient, however. The reason is that investors are loss averse, meaning that the value of a negative outcome of x multiplied by its probability of y is not the exact opposite of a positive outcome of x multiplied by its probability of y. As an example, if you were offered the opportunity to toss a coin—tails you lose your house and heads you are paid the value of your house—you would probably not take this bet because your fear of losing your house would outweigh the possible dollar payout—you would be loss averse.

Risk and Portfolio Theory

These risk concepts are applied to the construction of a portfolio of securities. The concept of diversification is commonly misunderstood. Using the term with reference to the foregoing discussion, you attempt to reduce the risk of a severely negative outcome by placing more bets that have independent outcomes, or diversifying. You equally reduce the chance of spectacular gains. Taking the example of the coin toss/bet the value of your house, if you were to agree to do 10 bets in a row, betting 10 percent of the value of your house each time, the odds of your losing the entire value of your house are infinitesimal since you would have to lose ten 50/50 bets in a row. On the other hand, the odds of your doubling the value of your house are infinitesimal as well.

In the case of the stock market, you can never reduce your risk to zero because the market itself has a base level of risk that results from risks that affect all stocks. If you want an essentially risk‐free investment, you have to invest only in U.S. Treasuries.

The term beta is simply a measure of the extent to which a particular stock's risk profile differs from the market generally. In theory, if you held all available stocks, you would have diversified away all of the risks of each of the stocks in your portfolio other than those that affect all stocks. You cannot completely eliminate them, but in economic terms, the stock‐specific risks with any particular stock should, if the worst happens, have a minuscule effect on the overall portfolio. Put another way, if one of your stocks experiences a loss or gain from its specific risk, it changes the risk profile and return of your portfolio close to nothing because you hold thousands of stocks. The implicit assumption here is that it is unlikely that your portfolio would experience many bad outcomes from individual stock‐specific risks.

Portfolio Theory as Applied to Acquisitions

What do these risk concepts and portfolio theory have to do with acquisitions? Simply, an acquisition is an investment by the Buyer. What a Buyer will rationally pay for a business or asset in an efficient market is a combination of the expected return from that asset, the riskiness of the investment, and the Buyer's appetite for risk.

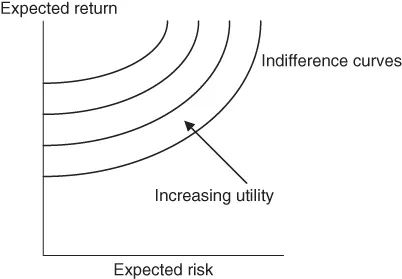

An interesting way to look at portfolio construction is by using what are known as indifference curves. The curves in Exhibit 1.1 show that for a hypothetical investor (and everyone is different), if that investor were happy with the risk/reward profile for an investment represented by a particular point on the grid (risk on one axis, return on the other), then you could construct a curve of the points on the grid where the investor would be equally happy (i.e., the investor presumably would be happy with an investment that offered greater returns as risk increased). Everyone's curves would be different, but it is thought that the curves would look something like those in Exhibit 1.1. The other thing depicted here is that each higher curve (in the direction of the arrow) represents a better set of investments for the particular individual investor than any curve in the opposite direction, because for any given amount of risk, the higher curve offers more return. That is what the words increasing utility mean in this diagram.

EXHIBIT 1.1 Indifference Curves

So far, we are dealing with theoretical sets of risks and returns that may have no relation to what is actually available in the market.

So, for an exclusively stock portfolio, one can plot sets of actual stock portfolios. Each actual stock portfolio has a different risk/reward combination. In Exhibit 1.2, the shaded area represents all of the possible com...