Incorporate economic moat analysis for profitable investing

Why Moats Matter is a comprehensive guide to finding great companies with economic moats, or competitive advantages. This book explains the investment approach used by Morningstar, Inc., and includes a free trial to Morningstar's Research.

Economic moats—or sustainable competitive advantages—protect companies from competitors. Legendary investor Warren Buffett devised the economic moat concept. Morningstar has made it the foundation of a successful stock-investing philosophy.

Morningstar views investing in the most fundamental sense: For Morningstar, investing is about holding shares in great businesses for long periods of time. How can investors tell a great business from a poor one? A great business can fend off competition and earn high returns on capital for many years to come. The key to finding these great companies is identifying economic moats that stem from at least one of five sources of competitive advantage—cost advantage, intangible assets, switching costs, efficient scale, and network effect. Each source is explored in depth throughout this book.

Even better than finding a great business is finding one at a great price. The stock market affords virtually unlimited opportunities to track prices and buy or sell securities at any hour of the day or night. But looking past that noise and understanding the value of a business's underlying cash flows is the key to successful long-term investing. When investors focus on a company's fundamental value relative to its stock price, and not where the stock price sits today versus a month ago, a day ago, or five minutes ago, investors start to think like owners, not traders. And thinking like an owner will makes readers better investors.

The book provides a fundamental framework for successful long-term investing. The book helps investors answer two key questions: How can investors identify a great business, and when should investors buy that business to maximize return?

Using fundamental moat and valuation analysis has led to superior risk-adjusted returns and made Morningstar analysts some of the industry's top stock-pickers. In this book, Morningstar shares the ins and outs of its moat-driven investment philosophy, which readers can use to identify great stock picks for their own portfolios.

Domande frequenti

Come faccio ad annullare l'abbonamento?

È semplicissimo: basta accedere alla sezione Account nelle Impostazioni e cliccare su "Annulla abbonamento". Dopo la cancellazione, l'abbonamento rimarrà attivo per il periodo rimanente già pagato. Per maggiori informazioni, clicca qui

È possibile scaricare libri? Se sì, come?

Al momento è possibile scaricare tramite l'app tutti i nostri libri ePub mobile-friendly. Anche la maggior parte dei nostri PDF è scaricabile e stiamo lavorando per rendere disponibile quanto prima il download di tutti gli altri file. Per maggiori informazioni, clicca qui

Che differenza c'è tra i piani?

Entrambi i piani ti danno accesso illimitato alla libreria e a tutte le funzionalità di Perlego. Le uniche differenze sono il prezzo e il periodo di abbonamento: con il piano annuale risparmierai circa il 30% rispetto a 12 rate con quello mensile.

Cos'è Perlego?

Perlego è un servizio di abbonamento a testi accademici, che ti permette di accedere a un'intera libreria online a un prezzo inferiore rispetto a quello che pagheresti per acquistare un singolo libro al mese. Con oltre 1 milione di testi suddivisi in più di 1.000 categorie, troverai sicuramente ciò che fa per te! Per maggiori informazioni, clicca qui.

Perlego supporta la sintesi vocale?

Cerca l'icona Sintesi vocale nel prossimo libro che leggerai per verificare se è possibile riprodurre l'audio. Questo strumento permette di leggere il testo a voce alta, evidenziandolo man mano che la lettura procede. Puoi aumentare o diminuire la velocità della sintesi vocale, oppure sospendere la riproduzione. Per maggiori informazioni, clicca qui.

Why Moats Matter è disponibile online in formato PDF/ePub?

Sì, puoi accedere a Why Moats Matter di Heather Brilliant, Elizabeth Collins in formato PDF e/o ePub, così come ad altri libri molto apprezzati nelle sezioni relative a Business e Azioni. Scopri oltre 1 milione di libri disponibili nel nostro catalogo.

Chapter 1 Guiding Principles of Morningstar’s Equity Research

What is a moat? For most people, images of water-filled trenches protecting castles from invaders immediately come to mind. We have taken that concept and applied it to investing, where an economic moat is a structural barrier protecting companies from competition.

Here at Morningstar, we’ve always viewed investing in the most fundamental sense of the word: We want to hold shares in great businesses for long periods of time. So what’s a great business? Essentially, we believe it’s one that can fend off competition and earn high returns on capital for many years into the future—increasing earnings, returning cash to shareholders, and compounding intrinsic value. Identifying companies like this is the goal of our economic moat analysis and our Morningstar Economic Moat Rating, which we explore in great detail in the coming chapters.

Even better than finding a great business is finding one at a great price. The stock market affords virtually unlimited opportunities to track prices and buy or sell securities at any hour of the day or night, but we think the key to successful long-term investing is concentrating not on the daily price movements of a stock but on the value of the cash flows generated by the underlying business. When you focus on a company’s underlying fundamental value relative to its stock price, and not where the stock price is today relative to a month ago or a day ago or five minutes ago, you start to think like an owner, rather than a trader.

If you’re looking for a book on how to get rich quick by trading in the stock market, you’ve come to the wrong place. Our goal is to give you a fundamental framework for successful long-term investing, which, we admit, is all we really know how to do. Our book aims to answer two primary questions: How can we identify which businesses are great? And when is the best time to buy these businesses, in order to maximize potential returns? If you can get just these two things right more often than not, you’ll be well on your way to becoming a successful long-term investor.

When Morningstar first started analyzing stocks more than a decade ago, we began with some core principles that guide our research to this day. Then and now, our analytic work has centered on three main elements: sustainable competitive advantages, valuation, and margin of safety, which we believe are the keys to outperforming the stock market over time. How exactly do we define these terms and why do they matter? That’s the purpose of this book. Throughout the coming chapters, we give you an overview of each of these principles, with the primary focus on how to identify companies with sustainable competitive advantages, or economic moats.

Question 1: How Can We Identify Which Businesses Are Great?

The answer to this question lies in finding companies with sustainable competitive advantages, or economic moats. Just as moats were dug around medieval castles to keep enemies at bay, economic moats protect the high returns on capital enjoyed by the world’s best companies.

Moats

In a famous 1999 Fortune article, legendary investor Warren Buffett wrote, “The key to investing is . . . determining the competitive advantage of any given company and, above all, the durability of that advantage. The products or services that have wide, sustainable moats around them are the ones that deliver rewards to investors.” With gratitude to Mr. Buffett, Morningstar has taken the economic moat concept a step further and developed a comprehensive moat-based analytic framework that can be applied consistently across a broad, global list of companies.

Whenever a company develops a profitable product or service, it isn’t long before other firms try to capitalize on that opportunity by producing a similar version, or even improving on the original version. We know from microeconomics that in a perfectly competitive market, rivals will eventually compete away any excess profits earned by a successful business. Nokia boasted the majority share of the mobile phone market for several years, but the introduction of Apple’s iPhone in 2007 and the subsequent evolution of the smartphone market left the flat-footed Nokia behind. A similar shift has occurred in the gaming industry, where longtime powerhouse Nintendo is seeing its iconic, family-friendly franchises left behind by powerful new consoles boasting high-end third-party software, such as Microsoft’s Xbox and Sony’s PlayStation. Meanwhile, mobile devices have begun to erode Nintendo’s dominant position in the handheld gaming market. In other words, profits attract competitors, and competition makes it difficult for firms to generate strong growth and margins over the long term.

But there are definitely some companies that manage to earn high returns on capital for extended periods of time. These companies are able to withstand the relentless onslaught of competition for long stretches, and these are the wealth-compounding machines that we want to find and own.

It’s important to note that an economic moat must be a structural element of the business itself. We’re not looking for companies with better short-term execution than competitors, or cyclical improvements that make returns on capital look good. We’re looking for companies where the business and industry structure protect profits. Along these lines, while great management can certainly enhance a company’s moat, just as poor management can detract from it, management itself cannot form the basis of an economic moat (more on that in Chapter 4).

Moats and Value Creation

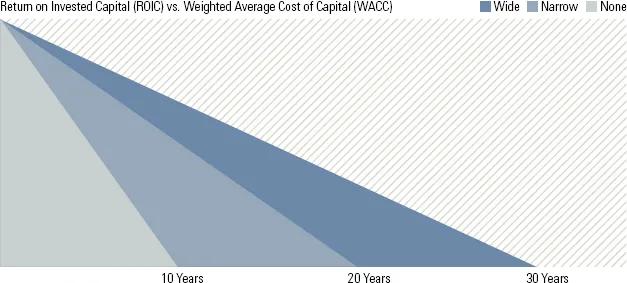

How much value a company will create for itself and its shareholders depends on two things: the amount of value currently being created and the business’ ability to continue to create value well into the future. The first factor is widely known by the market because it’s easy to calculate using basic financial statements. It’s the second factor, the magnitude and duration of future excess returns, that is harder to determine but is ultimately more important for successful long-term investing.

Here’s another way to illustrate this idea: Take three companies, each with a similar value-creating return on invested capital, or ROIC, today. The company that is able to sustain those excess returns the longest is going to be able to add the most value for itself over the coming years. In Figure 1.1, the company with the widest moat and the longest advantage period has the greatest value creation (area under the curve).

Figure 1.1 Measuring a Moat by the Duration of Excess Returns

Source: Morningstar.

Moats in Action

What does an economic moat look like for a real live company? Take electric utility ITC Holdings as an example. Electricity transmission isn’t exactly a sexy business, but investors in this pure-play transmission company have enjoyed double-digit earnings growth and healthy returns on capital thanks to its dominant market position and favorable long-term regulatory framework. We believe this “boring” utility has a wide economic moat that should protect those high returns for years to come. Its competitors have little incentive to build competing transmission lines if one that ITC owns is already serving a market’s full capacity; capital costs are too high and incremental benefits too low to offer sufficient returns for two competing transmission owners. In addition, ITC benefits from regulatory protection. The Federal Energy Regulatory Commission approves new transmission lines only if there is a demonstrated need for new capacity. In exchange for regulatory protection, ITC must charge rates based on a formula that allows ITC to recover its expenses and earn a reasonable return on investment. We believe that because of its transparency and predictability, a forward-looking formula rate—which is more investor-friendly than typical backward-looking rates given to most utilities—results in a below-average cost of capital for ITC and supports stable cash returns that we expect to last years into the future.

Contrast this with no-moat ethanol firms like Pacific Ethanol, VeraSun Energy, and Aventine Renewable Energy that boomed and then quickly busted in the past decade. The ethanol frenzy rose to a fever pitch in mid-2006, fueled by waves of government support and hotly anticipated IPOs. Two years later, investors in the corn-based fuel product were left with billions of dollars in losses as lofty expectations of this “wonder product” failed to pan out. This disappointment exemplifies an industry where it’s virtually impossible for a company to earn a moat, while it’s easy for new ethanol firms to enter, and hard for any single firm to establish a cost advantage, causing eventual oversupply and weak or nonexistent profits for all players.

Moat Sources

Over years of studying companies, we have identified five major sources of competitive advantage, or economic moat. We discuss each source in depth in the next chapter, but here’s a quick rundown of the five:

Intangible assets

Intangible assets include brands, patents, or government licenses that explicitly keep competitors at bay.

Cost advantage

Firms that have the ability to provide goods or services at lower cost have an advantage because they can undercut their rivals on price. Alternatively, they may sell their products or services at the same prices as rivals, but achieve fatter profit margins. We consider economies of scale to be a type of cost advantage, an idea we discuss in more detail in the next chapter.

Switching costs

Switching costs are those one-time inconveniences or expenses a customer incurs to change from one product to another. Customers facing high switching costs often won’t change providers unless they are offered a large improvement in either price or performance, and even then, the risk associated with making a change may still prevent switching in some industries.

Network effect

The network effect occurs when the value of a particular good or service increases for both new and existing users as more people use that good or service, often creating a viscious circle that allows strong companies to become even stronger.

Efficient scale

Efficient scale describes a dynamic in which a market of limited size is effectively served by one or just a few companies. The companies involved generate economic profits, but potential competitors are discouraged from entering because doing so would result in insufficient returns for all players.

Assigning Moat Ratings

When assigning moat ratings, we first consider the five qualitative factors outlined earlier. But we also look for quantitative evidence of a moat, namely, a company’s ability to earn excess returns on invested capital. The size of the spread between ROIC and cost of capital is actually far less important than the expected duration of the excess profits. When we believe that a company will more likely than not benefit from a competitive advantage and earn excess returns for a period of at least 10 years, we assign it a narrow moat rating. When we’re near-certain that a firm will earn excess returns for the next 10 years, and likely for the next 20 years, we assign the firm a wide moat rating. Clearly, the hurdle is high for earning a wide moat rating, and despite scouring the universe of listed companies, we have assigned wide moat ratings to fewer than 200 companies globally.

Question 2: When Is the Best Time to Invest in Great Businesses?

It’s tempting to conclude that wide-moat businesses are so rare and so great th...