Why Moats Matter is a comprehensive guide to finding great companies with economic moats, or competitive advantages. This book explains the investment approach used by Morningstar, Inc., and includes a free trial to Morningstar's Research.

Economic moats—or sustainable competitive advantages—protect companies from competitors. Legendary investor Warren Buffett devised the economic moat concept. Morningstar has made it the foundation of a successful stock-investing philosophy.

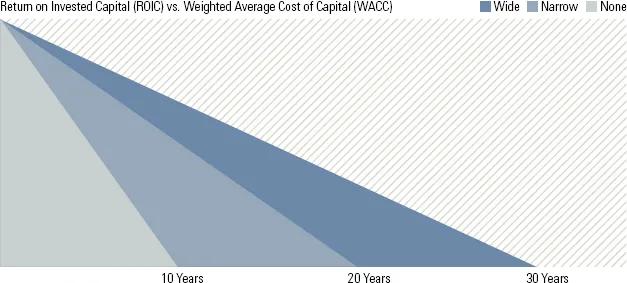

Morningstar views investing in the most fundamental sense: For Morningstar, investing is about holding shares in great businesses for long periods of time. How can investors tell a great business from a poor one? A great business can fend off competition and earn high returns on capital for many years to come. The key to finding these great companies is identifying economic moats that stem from at least one of five sources of competitive advantage—cost advantage, intangible assets, switching costs, efficient scale, and network effect. Each source is explored in depth throughout this book.

Even better than finding a great business is finding one at a great price. The stock market affords virtually unlimited opportunities to track prices and buy or sell securities at any hour of the day or night. But looking past that noise and understanding the value of a business's underlying cash flows is the key to successful long-term investing. When investors focus on a company's fundamental value relative to its stock price, and not where the stock price sits today versus a month ago, a day ago, or five minutes ago, investors start to think like owners, not traders. And thinking like an owner will makes readers better investors.

The book provides a fundamental framework for successful long-term investing. The book helps investors answer two key questions: How can investors identify a great business, and when should investors buy that business to maximize return?

Using fundamental moat and valuation analysis has led to superior risk-adjusted returns and made Morningstar analysts some of the industry's top stock-pickers. In this book, Morningstar shares the ins and outs of its moat-driven investment philosophy, which readers can use to identify great stock picks for their own portfolios.