The Business of Venture Capital

The Art of Raising a Fund, Structuring Investments, Portfolio Management, and Exits

Mahendra Ramsinghani

- English

- ePUB (disponibile sull'app)

- Disponibile solo in versione web

The Business of Venture Capital

The Art of Raising a Fund, Structuring Investments, Portfolio Management, and Exits

Mahendra Ramsinghani

Informazioni sul libro

The new edition of the definitive guide for venture capital practitioners—covers the entire process of venture firm formation & management, fund-raising, portfolio construction, value creation, and exit strategies

Since its initial publication, The Business of Venture Capital has been hailed as the definitive, most comprehensive book on the subject. Now in its third edition, this market-leading text explains the multiple facets of the business of venture capital, from raising venture funds, to structuring investments, to generating consistent returns, to evaluating exit strategies. Author and VC Mahendra Ramsinghani who has invested in startups and venture funds for over a decade, offers best practices from experts on the front lines of this business.

This fully-updated edition includes fresh perspectives on the Softbank effect, career paths for young professionals, case studies and cultural disasters, investment models, epic failures, and more. Readers are guided through each stage of the VC process, supported by a companion website containing tools such as the LP-GP Fund Due Diligence Checklist, the Investment Due Diligence Checklist, an Investment Summary format, and links to white papers and other industry guidelines. Designed for experienced practitioners, angels, devils, and novices alike, this valuable resource:

- Identifies the key attributes of a VC professional and the arc of an investor's career

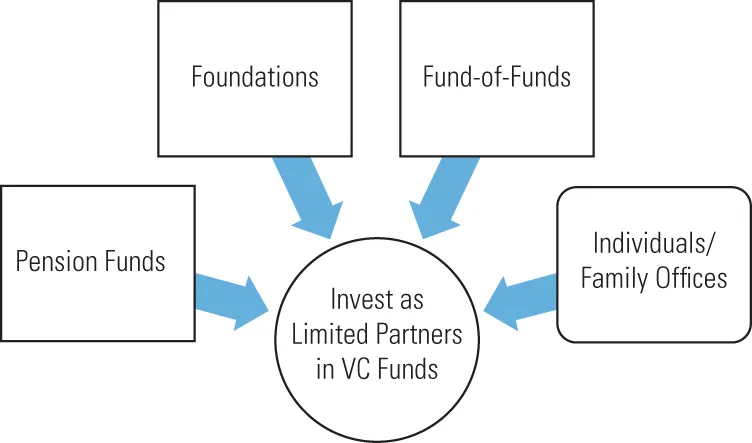

- Covers the art of raising a venture fund, identifying anchor investors, fund due diligence, negotiating fund investment terms with limited partners, and more

- Examines the distinct aspects of portfolio construction and value creation

- Balances technical analyses and real-world insights

- Features interviews, personal stories, anecdotes, and wisdom from leading venture capitalists

The Business of Venture Capital, Third Edition is a must-read book for anyone seeking to raise a venture fund or pursue a career in venture capital, as well as practicing venture capitalists, angel investors or devils alike, limited partners, attorneys, start-up entrepreneurs, and MBA students.

Domande frequenti

Informazioni

Part One

The Making of a VC

1

The Business of Cash and Carry

INTRODUCTION: AN OPERATIONAL PRIMER