The new edition of the definitive guide for venture capital practitioners—covers the entire process of venture firm formation & management, fund-raising, portfolio construction, value creation, and exit strategies

Since its initial publication, The Business of Venture Capital has been hailed as the definitive, most comprehensive book on the subject. Now in its third edition, this market-leading text explains the multiple facets of the business of venture capital, from raising venture funds, to structuring investments, to generating consistent returns, to evaluating exit strategies. Author and VC Mahendra Ramsinghani who has invested in startups and venture funds for over a decade, offers best practices from experts on the front lines of this business.

This fully-updated edition includes fresh perspectives on the Softbank effect, career paths for young professionals, case studies and cultural disasters, investment models, epic failures, and more. Readers are guided through each stage of the VC process, supported by a companion website containing tools such as the LP-GP Fund Due Diligence Checklist, the Investment Due Diligence Checklist, an Investment Summary format, and links to white papers and other industry guidelines. Designed for experienced practitioners, angels, devils, and novices alike, this valuable resource:

Identifies the key attributes of a VC professional and the arc of an investor's career

Covers the art of raising a venture fund, identifying anchor investors, fund due diligence, negotiating fund investment terms with limited partners, and more

Examines the distinct aspects of portfolio construction and value creation

Balances technical analyses and real-world insights

Features interviews, personal stories, anecdotes, and wisdom from leading venture capitalists

The Business of Venture Capital, Third Edition is a must-read book for anyone seeking to raise a venture fund or pursue a career in venture capital, as well as practicing venture capitalists, angel investors or devils alike, limited partners, attorneys, start-up entrepreneurs, and MBA students.

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Most good beginnings in this land of venture capital careers involve some planning, some luck, and not taking yourself too seriously. How does this business work — what does an average day look like — how do you get in and how do you grow — and what are the pitfalls? Is it just about making money — multiplying green pieces of paper and filthy lucre?

Should you try to keep improving every day? “If you are under the impression you have already perfected yourself, you will never rise to the heights you are no doubt capable of,” Kazuo Ishiguro, wrote in his book, The Remains of the Day. It is no wonder that Jeff Bezos, founder and CEO of Amazon, refers to this book as one of his favorites.

What makes a good VC? Is it skill, tenacity, or that mysterious stroke of luck? Is it a network of relationships, or is it market timing? And who decides what is good? If you follow the industry standards, then it's largely returns — cash-on-cash multiples you can generate as fast as you can. That will get you a place on the vanity charts of Forbes Midas List of Venture Capitalists, which can elevate your brand and career prospectus. How do you grow as a person? Should VCs think about their role in society — to support and enhance systems of governance, better education, role of arts, and a healthier environment? Or should we pretend that those problems do not belong to us nor affect us?

As my mama said, never trust anyone who tells you how to get in but does not show you how to get out — be it a swimming pool, a dark cave with supposedly hidden treasures, or the business of venture capital. Hanging out with cool founders every day, discussing the latest bleeding-edge trends, can be fun, even addictive. You need to know how to get out of this business. Alcoholics Anonymous has a 12-step program to recovery — but for investors addicted to the adrenalin rush of cool-tech and exit-highs, there are no support groups. On that note, I have added a chapter on your own exit strategies — just as you get in, you should know how to graciously find your way out of the maze.

1 The Business of Cash and Carry

INTRODUCTION: AN OPERATIONAL PRIMER

For Masayoshi Son, raising a $100 billion Softbank Vision fund was easy. As he quips, it was “$45 billion in 45 minutes” — his 45-minute meeting with Saudi Arabia's crown prince kicked off the fund raise. To the prince, Masa offered a gift. “I want to give you a Masa gift, the Tokyo gift, a $1 trillion gift. Here's how I can give you a $1 trillion gift: You invest $100 billion in my fund, I give you a trillion.” Son left the meeting with a commitment of $45 billion, and other investors followed soon thereafter. The world's largest venture fund was off to the races.

But if raising $100 billion was that easy, the doyens of Sand Hill Road venture firms would have done it long ago. For Softbank, the journey started in the year 2000, with a $20 million investment in Alibaba, a startup that would eventually grow into a Chinese e-commerce giant. Alibaba went public in 2014, and at that time, Softbank's 28 percent stake in the company was valued at $58 billion. Son had also invested in Yahoo! in 1996 and reaped its rewards, following the company's IPO four years later. Son's fascination with the world of technology started with the microprocessor. “When I was 17 years old, the very first time I saw a photo of a microprocessor, it made me cry. I was overwhelmed,” he would say. As the waves of innovation rose and fell, the teeny microprocessor spawned into the World Wide Web in the 1990s, followed by the cloud and mobility a decade later. Son kept surfing along and is poised to ride the next trend — be it technological changes like robotics, automation, and artificial intelligence (AI) or societal changes such as ridesharing, vertical farming, and food delivery.

Those who have analyzed his historic investment track record point to the fact that even if you slice off the biggest win — his Alibaba investment — the rest of his portfolio shows above 40 percent internal rate of return (IRR). When the industry average performance is in the mid-teens, having such a significant edge in investment performance helps. Combine that with a boldness of vision and the ability to execute on a global investment strategy and voilà — you have $45 billion in 45 minutes.

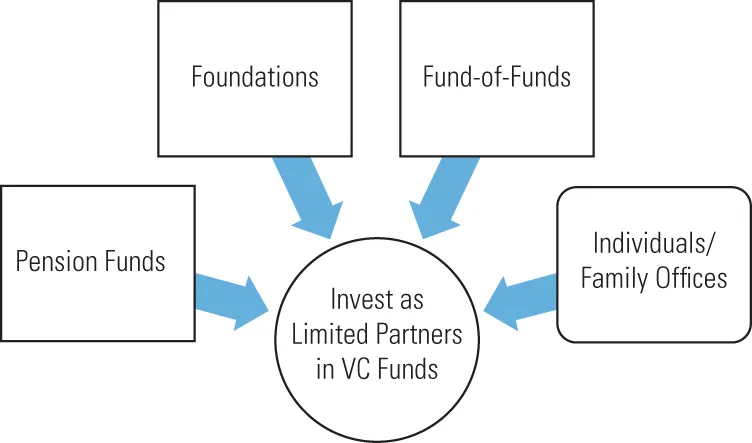

The venture capitalist's journey often begins with the ability to raise a venture fund (Exhibit 1.1). The universe of investors in any venture fund includes two broad categories: (a) institutional investors such as pension funds, foundations, university endowments, sovereign wealth funds, business corporations, and (b) high-net-worth individuals (HNWIs) and their family offices (see Exhibit 1.2). Institutional investors primarily view venture funds as an asset class, a money-making machine that promises to deliver an annualized “risk-adjusted” IRR.

Exhibit 1.1Venture capital business model.

Exhibit 1.2Limited partners.

The VC business model is simple: a venture capitalist, or general partner (GP), knocks on the door of various investors, known as limited partners (LP), to raise a fund. LPs agree to invest in venture funds based on the venture capitalist's background, investment expertise and past performance, a compelling investment strategy, and, to some extent, that mystical X factor — an amalgamation of ability, skills, and luck that defies any logical construct and makes one practitioner more successful than the others.

The two groups — the GP as the investment manager and the LP as the provider of capital — form a 10-year partnership. The LP agrees to pay the GP a management fee each year and a share in a percentage of the profits. In turn, the GP agrees to work night and day to find hot, blazing startups, to invest the capital, turn them into unicorns (billion-dollar valued companies), and harvest the money back in large multiples. The end game for the LP is to make a superior risk-adjusted financial return. The primary measure of success for the venture firm is the IRR and cash-on-cash (C-on-C) return, a multiple of the original investment amount or multiple of invested capital (MOIC). Venture firms and GPs live, and are slaughtered by, these two metrics.

To better understand the economics, take the example of a $100 million fund. The GPs of the fund would invest this capital in, say, about a dozen companies and after building value aspire to “exit” the investments, meaning to sell the ownership. Should these investments generate profits, the investors (or LPs) keep 80 percent of the profits, and the GPs take home 20 percent. The profit, called carried interest or carry, where one-fifth profits were shared, has evolved from the time of Phoenicians, who in the year 1200 CE commanded 20 percent of profits earned from trade and shipping merchandise. In addition to the carry, the LPs also pay the GPs an annual management fee, typically 2 to 2.5 percent of the committed capital per year. Thus, for a $100 million fund with a predetermined life of 10 years, annual fees of 2 percent yield $2 million for the firm. The fees provide for the day-to-day operations of the firm and are used to pay for salaries, travel, operational, and legal expenses. The responsibilities and compensation packages are determined by the professional's responsibilities and experience.

A venture fund is defined as a fixed pool of capital raise...

Table of contents

Cover

Table of Contents

Title Page

Copyright

Dedication

Foreword

Preface

Acknowledgments

Part One: The Making of a VC

Part Two: Raising Your Venture Fund

Part Three: Building Your Portfolio

Part Four: The Art of Value Creation

Part Five: Exits: Liquidity Events and Champagne

Index

End User License Agreement

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

Both plans are available with monthly, semester, or annual billing cycles.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go. Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access The Business of Venture Capital by Mahendra Ramsinghani in PDF and/or ePUB format, as well as other popular books in Business & Corporate Finance. We have over 1.5 million books available in our catalogue for you to explore.