The rise of hard discounters like Aldi and Lidl has been monumental. Explore the very real threat they pose to traditional retailers and brand manufacturers and what you can learn from their growth.

Hard discounters are stores that sell a limited selection of consumer-packaged goods and perishables - typically fewer than 2,000 Stock Keeping Units - for prices that are usually 50-60% lower than national brands. The best-known hard discounters are Aldi and Lidl, but global brands include Trader Joe's, EuroSpin, Biedronka, Netto and Leader Price. Their rise has been monumental; they have irrevocably changed the face of retail in Europe and Australia and are making steady inroads into the US.

Retail Disruptors is the first book that explores this upheaval, providing expert insight into the business models of the leading hard discounters, and what mainstream retailers and brand manufacturers can do to remain competitive in the face of disruption. Meticulously researched by two of the leading authorities in retail strategy, private labels, branding, and hard discounting, Retail Disruptors is essential reading for all brand manufacturers and retailers who want to retain the competitive edge.

eBook - ePub

Retail Disruptors

The Spectacular Rise and Impact of the Hard Discounters

- English

- ePUB (mobile friendly)

- Available on iOS & Android

eBook - ePub

Retail Disruptors

The Spectacular Rise and Impact of the Hard Discounters

About this book

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Study more efficiently using our study tools.

PART ONE

Hard discounter strategies

02

Understanding the hard discounter business model

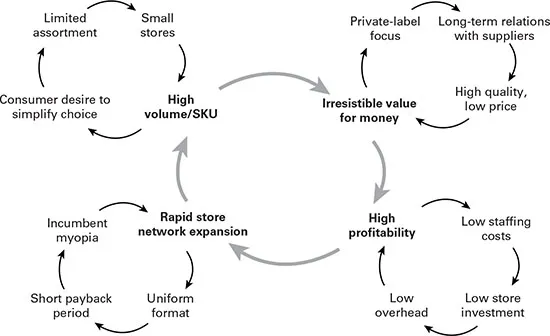

How are hard discounters able to grow so fast? How are they able to make money at such low price points? Why has it proven so difficult for conventional retailers to copy elements of their model to fight them off? To answer these questions, we must take a close look at the business model that powers the hard discounter format. While different hard discounters, of course, do not follow the exact same model, there are many similarities that are brought together in Figure 2.1. The core of the business model is the virtuous cycle, in which a high volume per stock keeping unit (SKU) leads to irresistible value for money for consumers. This contributes to high profitability that funds expansion of the store network, which further increases the volume per SKU, and so on. We take up each of these in turn.

Figure 2.1 Hard discounter business model

We need to point out, though, that each of these four key success factors can only be in place because of specific and crucial enabling processes, which are also outlined in Figure 2.1. In our discussion of the key success factors, we will take a look at these enabling processes as well.

High volume per SKU

High volume per SKU is not feasible in a mainstream supermarket which carries 25,000–40,000 items. There is simply not enough consumer demand to achieve high sales volume for so many SKUs. The hard discounter solves this problem by limiting the number of SKUs offered to around 1,000–2,500 items. In each category, it carefully selects only the most popular flavours, package sizes, or other types of variety. This strategy leads to high volumes per item. We illustrate this for the Netherlands, where we compare Aldi with market leader Albert Heijn (Table 2.1).1 Aldi carries about 1,250 different items versus 27,500 items offered by Albert Heijn. Aldi generates revenues of €2.5 billion per year with 500 stores, while Albert Heijn generates €13 billion per year with 950 stores.

Table 2.1 Comparison of sales per SKU between Aldi and Albert Heijn in the Netherlands in 2016

| Aldi | Albert Heijn | |

Total revenues | €2.5 bn | €13 bn |

Market share | 7.0% | 35.2% |

Number of stores | 500 | 950 |

Number of SKUs | 1,250 | 27,500 |

Revenues per store | €5.0 mn | €13.7 mn |

Revenues per SKU | €2.0 mn | €0.5 mn |

Revenues per SKU per store | €4,000 | €500 |

SOURCE Based on 2017 research from EFMI Business School

At first sight, Albert Heijn outperforms Aldi almost by a factor of three when sales per store are compared: €13.7 million versus €5.0 million. But when we compare the sales per item, a totally different picture arises: Aldi sells €2 million per SKU per year versus €0.5 million for Albert Heijn. So, even with only one-fifth of the market share, Aldi’s revenue per SKU is four times that of Albert Heijn. And Albert Heijn is the market leader! The situation for other chains is even bleaker. If we further take into account that many Aldi items are sold in other countries, the factor of four can easily become a factor of 10 or more. That is one of the amazing effects of item rationalization.

But why would consumers patronize a store that limits their freedom of choice by more than 95 per cent? Because more choice is not always preferred by shoppers.

Consumer desire for choice simplicity

It is a common supposition in Western society that choice is good, and the more choice, the better. Economic theory dictates that the greater the number of options in a product category, the higher the likelihood that consumers can find a close match to their needs. This attracts a broader, more diverse set of people to the store, as they can be more confident that they can find a suitable item in that store, facilitating one-stop shopping. Economic theory further postulates that consumers derive utility from freedom of choice and enjoyment of exploration in the store. As it turns out, this is not necessarily the case.

In one famous study conducted in an upscale grocery store in Menlo Park, California, researchers showed that consumers were more likely to make a purchase when presented with an assortment comprising of six flavours of jam than with an assortment comprising of 24 flavours (all flavours were of the same brand).2 The difference was substantial: only 2 per cent of the consumers in the extensive-choice context made a purchase versus 12 per cent of the consumers in the limited-choice condition. This study is not an isolated instance. A stream of subsequent work has documented that consumers regularly experience choice overload, leading to less satisfaction, more post...

Table of contents

- Cover

- Title Page

- Copyright

- Contents

- List of figures

- List of tables

- List of abbreviations

- About the authors

- Preface

- Acknowledgements

- 01 How hard discounters are disrupting the traditional retail model

- PART ONE Hard discounter strategies

- PART TWO Competitive counterstrategies for conventional retailers

- PART THREE Brand manufacturer strategies versus hard discounters

- Index

- Backcover

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

- Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

- Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go.

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Retail Disruptors by Jan-Benedict Steenkamp,Laurens Sloot in PDF and/or ePUB format, as well as other popular books in Commerce & Marketing. We have over 1.5 million books available in our catalogue for you to explore.