- 212 pages

- English

- ePUB (mobile friendly)

- Available on iOS & Android

eBook - ePub

Improving Food and Beverage Performance

About this book

The food and beverage aspect of hotel operations is often the most difficult area to control effectively, but it plays a crucial role in customer satisfaction. Improving Food and Beverage Performance is able to show how successful catering operations can increase profitability whilst providing continuing improvements in quality, value and service.

Keith Waller looks at the practical issues of improving performance combining the key themes of quality customer service and efficient management. This text will enable managers and students alike to recognise all the contributing factors to a successful food and beverage operation.

Keith Waller is Senior Lecturer for the Faculty of Business and Management at Blackpool and the Fylde College. He has extensive experience in the hospitality industry and is a member of the Hotel and Catering International Management Association. He is the co-author, with Professor John Fuller, of The Menu, Food and Profit.

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Study more efficiently using our study tools.

1

Customer-Centred Performance Improvement

Aims and Objectives

This chapter aims to show how improving products and services for the customer can reap benefits for the caterer. Cutting cost is not and should not be the only way to increase profit.

As has already been noted, there are many ways in which a catering operation may develop (strategy/tactics), all of which may offer positive potential. If an operation is to be successful then any strategy development must involve reference to the customer. Even where the main objective is to improve profit performance this cannot be achieved without knowledge of the market conditions, including customer analysis. Further, it may be argued that the only way to improve profit performance is by meeting customer needs more effectively.

The effective food and beverage manager needs to clearly understand the operating environment: the market, customer needs, wants and expectations. Thorough knowledge of resource availability will enable effective and economic plans to be produced.

What is Customer-Centred Performance Improvement?

The Hospitality Environment Defined

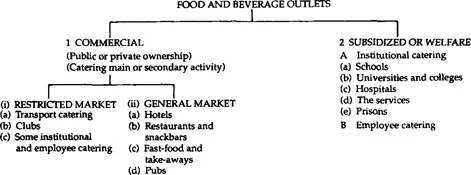

The Significance of Sectors

While Figure 1.1 may help to describe the industry it does not assist in the development of business opportunities within it. It could be argued that many of the more recent success stories in our industry result from the fact that they did not conform to the accepted industry norms. It is true that such classification is used for the presentation of statistics from which we can compare our own performance against competitors. But such a narrow measure may be what is actually holding us back.

Figure 1.1 The main sectors of the hospitality industry.

Source: Davis and Stone, 1991.

Keeping pace with the immediate competition leads to complacency. Recent data (published in Croner’s Catering) suggest the industry standards of performance given in Table 1.1. If I manage a public house with a 60 per cent GP on food, then I am doing well because that is the industry standard. But restaurants and hotels are managing 65 per cent. How and why shouldn’t I be able to achieve the same, or better? Operations should try to review operational performance on its own merits without reference to sector norms. How well are we meeting our own targets, how innovative are we, can we attract business from other sectors?

Table 1.1 Gross profit guidelines

Type of business | Gross profit | |

Liquor (%) | Food (%) | |

Public houses | 40–55 | 40–60 |

Restaurants/hotels | 45–65 | 50–65 |

Banqueting | 55–70 | 55–70 |

Wine bars | 45–55 | 40–50 |

Self service | 45–55 | 60–70 |

School meals | N/A | 30–50 |

Member’s clubs | 25–45 | 30–60 |

Outdoor catering | 50–60 | 50–70 |

Fast food | N/A | 55–70 |

Kiosks | N/A | 30 |

Compiled by Michael J. Boella for Croner’s Catering (May 1995) © Croner Publications Ltd, 1995.

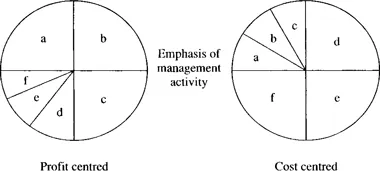

Categorizing catering operations as private (commercial) or public (welfare) is no longer relevant in terms of performance improvement. The benefits of moving away from the old welfare concept of annual budgeting has been welcomed by most managers. Although threatened by privatization and market testing (competitive tendering) welfare manages now have greater control over their operations and are using commercial techniques to good effect. What little remains of the private/public divide may be found in the tendency for operations to be either profit or cost centred, measuring their performance primarily against profit or cost targets. Because a high street restaurant will have relatively high fixed costs, rent and rates, it is likely to be profit centred. Rent and rates attributable to a caterer operating within a hospital may be more difficult to attribute (identify and allocate a cost for) consequently hospital catering managers will tend to concentrate on variable costs. To suggest that all private operations are profit centred and all welfare operations are cost centred is an over-generalization. It is important that each and every operation examines its financial structure in order to more carefully consider its cost/profit strategy.

Figure 1.2 Profit versus cost orientation. One operation is concerned with revenue and the other is concerned with cost. a, high fixed costs (rent, rates, etc.); b, emphasis on increasing revenue; c, flexible pricing policies to respond quickly to changing situations, unstable activity, emphasis on marketing/merchandising to maintain volume; d, high variable costs; e, emphasis on cost controls; f, stable activity, use of merchandising to improve performance (customer satisfaction), fixed pricing policy.

Consider two operations which are both currently operating at the same break even point. They both want to improve their performance, become more profitable. Both would benefit from increased volume and reduced costs, but where should management effort be concentrated?

Figure 1.3 Comparison of profit-centred and cost-centred operations. (a) High fixed costs – profit centred. Little to be gained from management of variable costs. (b) High variable costs – cost centred. Little to be gained from increasing volume, variable costs will continue increasing at the same rate. FC, fixed cost; VC, variable cost; TC, total cost (VC + FC).

Both operations may currently be in the same position, have the same total revenue and the same volume of sales. However, future strategy (potential for performance improvement) is quite differen...

Table of contents

- Cover

- Half Title

- Dedication

- Title Page

- Copyright

- Contents

- Preface

- Introduction

- 1. Customer-centred performance improvement

- 2. Developing operational policy

- 3. Marketing

- 4. Merchandising

- 5. Quality

- 6. Product and service development

- 7. Systems management

- 8. Efficient staffing

- 9. Summary

- Bibliography

- Index

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go.

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Improving Food and Beverage Performance by Keith Waller in PDF and/or ePUB format, as well as other popular books in Business & Hospitality, Travel & Tourism Industry. We have over 1.5 million books available in our catalogue for you to explore.