- English

- ePUB (mobile friendly)

- Available on iOS & Android

eBook - ePub

About this book

Doing well with money isn't necessarily about what you know. It's about how you behave. And behavior is hard to teach, even to really smart people.

Money—investing, personal finance, and business decisions—is typically taught as a math-based field, where data and formulas tell us exactly what to do. But in the real world people don't make financial decisions on a spreadsheet. They make them at the dinner table, or in a meeting room, where personal history, your own unique view of the world, ego, pride, marketing, and odd incentives are scrambled together.

In The Psychology of Money, award-winning author Morgan Housel shares 19 short stories exploring the strange ways people think about money and teaches you how to make better sense of one of life's most important topics.

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Study more efficiently using our study tools.

Key takeaways

AI-Generated Insights

Insight 1

Analyze how psychological biases and personal experiences influence financial decision-making, distinguishing between traditional economic models and real-world human behavior.

Insight 2

Evaluate fundamental financial concepts such as compounding, risk, and wealth accumulation, considering their long-term implications and the behavioral challenges in their application.

Insight 3

Develop strategies for navigating financial uncertainty and managing personal expectations by recognizing the impact of historical context and individual perspectives on wealth management.

Information

Let me tell you about a problem. It might make you feel better about what you do with your money, and less judgmental about what other people do with theirs.

People do some crazy things with money. But no one is crazy.

Here’s the thing: People from different generations, raised by different parents who earned different incomes and held different values, in different parts of the world, born into different economies, experiencing different job markets with different incentives and different degrees of luck, learn very different lessons.

Everyone has their own unique experience with how the world works. And what you’ve experienced is more compelling than what you learn second-hand. So all of us—you, me, everyone—go through life anchored to a set of views about how money works that vary wildly from person to person. What seems crazy to you might make sense to me.

The person who grew up in poverty thinks about risk and reward in ways the child of a wealthy banker cannot fathom if he tried.

The person who grew up when inflation was high experienced something the person who grew up with stable prices never had to.

The stock broker who lost everything during the Great Depression experienced something the tech worker basking in the glory of the late 1990s can’t imagine.

The Australian who hasn’t seen a recession in 30 years has experienced something no American ever has.

On and on. The list of experiences is endless.

You know stuff about money that I don’t, and vice versa. You go through life with different beliefs, goals, and forecasts, than I do. That’s not because one of us is smarter than the other, or has better information. It’s because we’ve had different lives shaped by different and equally persuasive experiences.

Your personal experiences with money make up maybe 0.00000001% of what’s happened in the world, but maybe 80% of how you think the world works. So equally smart people can disagree about how and why recessions happen, how you should invest your money, what you should prioritize, how much risk you should take, and so on.

In his book on 1930s America, Frederick Lewis Allen wrote that the Great Depression “marked millions of Americans—inwardly—for the rest of their lives.” But there was a range of experiences. Twenty-five years later, as he was running for president, John F. Kennedy was asked by a reporter what he remembered from the Depression. He remarked:

I have no first-hand knowledge of the Depression. My family had one of the great fortunes of the world and it was worth more than ever then. We had bigger houses, more servants, we traveled more. About the only thing that I saw directly was when my father hired some extra gardeners just to give them a job so they could eat. I really did not learn about the Depression until I read about it at Harvard.

This was a major point in the 1960 election. How, people thought, could someone with no understanding of the biggest economic story of the last generation be put in charge of the economy? It was, in many ways, overcome only by JFK’s experience in World War II. That was the other most widespread emotional experience of the previous generation, and something his primary opponent, Hubert Humphrey, didn’t have.

The challenge for us is that no amount of studying or open-mindedness can genuinely recreate the power of fear and uncertainty.

I can read about what it was like to lose everything during the Great Depression. But I don’t have the emotional scars of those who actually experienced it. And the person who lived through it can’t fathom why someone like me could come across as complacent about things like owning stocks. We see the world through a different lens.

Spreadsheets can model the historic frequency of big stock market declines. But they can’t model the feeling of coming home, looking at your kids, and wondering if you’ve made a mistake that will impact their lives. Studying history makes you feel like you understand something. But until you’ve lived through it and personally felt its consequences, you may not understand it enough to change your behavior.

We all think we know how the world works. But we’ve all only experienced a tiny sliver of it.

As investor Michael Batnick says, “some lessons have to be experienced before they can be understood.” We are all victims, in different ways, to that truth.

In 2006 economists Ulrike Malmendier and Stefan Nagel from the National Bureau of Economic Research dug through 50 years of the Survey of Consumer Finances—a detailed look at what Americans do with their money.4

In theory people should make investment decisions based on their goals and the characteristics of the investment options available to them at the time.

But that’s not what people do.

The economists found that people’s lifetime investment decisions are heavily anchored to the experiences those investors had in their own generation—especially experiences early in their adult life.

If you grew up when inflation was high, you invested less of your money in bonds later in life compared to those who grew up when inflation was low. If you happened to grow up when the stock market was strong, you invested more of your money in stocks later in life compared to those who grew up when stocks were weak.

The economists wrote: “Our findings suggest that individual investors’ willingness to bear risk depends on personal history.”

Not intelligence, or education, or sophistication. Just the dumb luck of when and where you were born.

The Financial Times interviewed Bill Gross, the famed bond manager, in 2019. “Gross admits that he would probably not be where he is today if he had been born a decade earlier or later,” the piece said. Gross’s career coincided almost perfectly with a generational collapse in interest rates that gave bond prices a tailwind. That kind of thing doesn’t just affect the opportunities you come across; it affects what you think about those opportunities when they’re presented to you. To Gross, bonds were wealth-generating machines. To his father’s generation, who grew up with and endured higher inflation, they might be seen as wealth incinerators.

The differences in how people have experienced money are not small, even among those you might think are pretty similar.

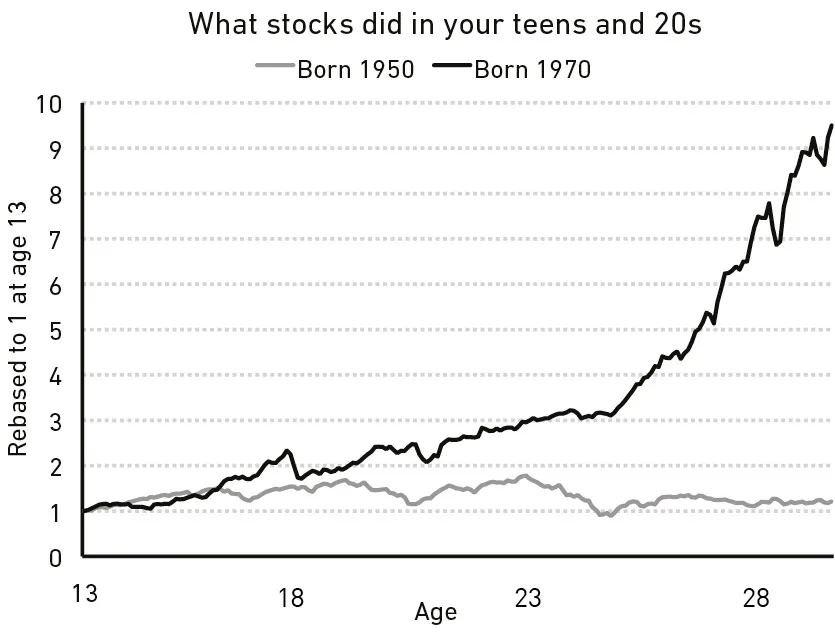

Take stocks. If you were born in 1970, the S&P 500 increased almost 10-fold, adjusted for inflation, during your teens and 20s. That’s an amazing return. If you were born in 1950, the market went literally nowhere in your teens and 20s adjusted for inflation. Two groups of people, separated by chance of their birth year, go through life with a completely different view on how the stock market works:

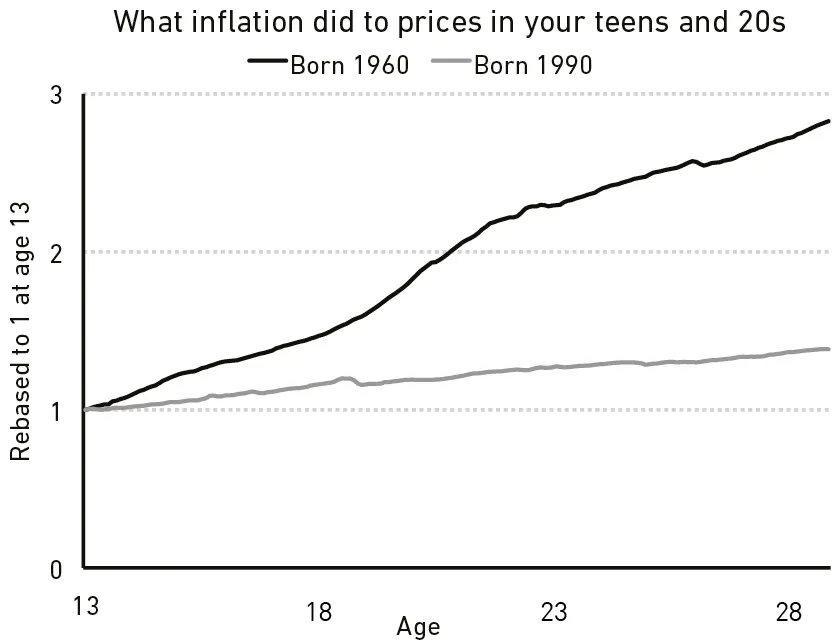

Or inflation. If you were born in 1960s America, inflation during your teens and 20s—your young, impressionable years when you’re developing a base of knowledge about how the economy works—sent prices up more than threefold. That’s a lot. You remember gas lines and getting paychecks that stretched noticeably less far than the ones before them. But if you were born in 1990, inflation has been so low for your whole life that it’s probably never crossed your mind.

America’s nationwide unemployment in November 2009 was around 10%. But the unemployment rate for African American males age 16 to 19 without a high school diploma was 49%. For Caucasian females over age 45 with a college degree, it was 4%.

Local stock markets in Germany and Japan were wiped out during World War II. Entire regions were bombed out. At the end of the war German farms only produced enough food to provide the country’s citizens with 1,000 calories a day. Compare that to the U.S., where the stock market more than doubled from 1941 through the end of 1945, and the economy was the strongest it had been in almost two decades.

No one should expect members of these groups to go through the rest of their lives thinking the same thing about inflation. Or the stock market. Or unemployment. Or money in general.

No one should expect them to respond to financial information the same way. No one should assume they are influenced by the same incentives.

No one should expect them to trust the same sources of advice.

No one should expect them to agree on what matters, what’s worth it, what’s likely to happen next, and what the best path forward is.

Their view of money was formed in different worlds. And when that’s the case, a view about money that one group of people thinks is outrageous can make perfect sense to another.

A few years ago, The New York Times did a story on the working conditions of Foxconn, the massive Taiwanese electronics manufacturer. The conditions are often atrocious. Readers were rightly upset. But a fascinating response to the story came from the nephew of a Chinese worker, who wrote in the comment section:

My aunt worked several years in what Americans call “sweat shops.” It was hard work. Long hours, “small” wage, “poor” working conditions. Do you know what my aunt did before she worked in one of these factories? She was a prostitute.

The idea of working in a “sweat shop” compared to that old lifestyle is an improvement, in my opinion. I know that my aunt would rather be “exploited” by an evil capitalist boss for a couple of dollars than have her body be exploited by several men for pennies.

That is why I am upset by many Americans’ thinking. We do not have the same opportunities as the West. Our governmental infrastructure is different. The country is different. Yes, factory is hard labor. Could it be better? Yes, but only when you compare such to American jobs.

I don’t know what to make of this. Part of me wants to argue, fiercely. Part of me wants to understand. But mostly it’s an example of how different experiences can lead to vastly different views within topics that one side intuitively thinks should be black and white.

Every decision people make with money is justified by taking the information they have at the moment and plugging it into their unique mental model of how the world works.

Those people can be misinformed. They can have incomplete information. They can be bad at math. They can be persuaded by rotten marketing. They can have no idea what they’re doing. They can misjudge the consequences of their actions. Oh, can they ever.

But every financial decision a person makes, makes sense to them in that moment and checks the boxes they need to check. They tell themselves a story about what they’re doing and wh...

Table of contents

- Introduction: The Greatest Show On Earth

- 1. No One’s Crazy

- 2. Luck & Risk

- 3. Never Enough

- 4. Confounding Compounding

- 5. Getting Wealthy vs. Staying Wealthy

- 6. Tails, You Win

- 7. Freedom

- 8. Man in the Car Paradox

- 9. Wealth is What You Don’t See

- 10. Save Money

- 11. Reasonable > Rational

- 12. Surprise!

- 13. Room for Error

- 14. You’ll Change

- 15. Nothing’s Free

- 16. You & Me

- 17. The Seduction of Pessimism

- 18. When You’ll Believe Anything

- 19. All Together Now

- 20. Confessions

- Postscript: A Brief History of Why the U.S. Consumer Thinks the Way They Do

- Endnotes

- Acknowledgements

- Publishing details

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go.

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access The Psychology of Money by Morgan Housel in PDF and/or ePUB format, as well as other popular books in Business & Wealth Management. We have over 1.5 million books available in our catalogue for you to explore.