Financial services are an ever increasing part of the infrastructure of everyday life. From banking to credit, insurance to investment and mortgages to advice, we all consume financial services, and many millions globally work in the sector. Moreover, the way we consume them is changing with the growing dominance of fintech and Big Data. Yet, the part of financial services that we engage with as consumers is just the tip of a vast network of markets, institutions and regulators – and fraudsters too.

Many books about financial services are designed to serve corporate finance education, focusing on capital structures, maximising shareholder value, regulatory compliance and other business-oriented topics. A Practical Guide to Financial Services: Knowledge, Opportunities and Inclusion is different: it swings the perspective towards the end-user, the customer, the essential but often overlooked participant without whom retail financial services markets would not exist. While still introducing all the key areas of financial services, it explores how the sector serves or sometimes fails to serve consumers, why consumers need protection in some areas and what form that protection takes, and how consumers can best navigate the risks and uncertainties that are inherent in financial products and services.

For consumers, a greater understanding of how the financial system works is a prerequisite of ensuring that the system works for their benefit. For students of financial services – those aspiring to or those already working in the sector – understanding the consumer perspective is an essential part of becoming an effective, holistically informed and ethical member of the financial services community. A Practical Guide to Financial Services: Knowledge, Opportunities and Inclusion will equip you for both these roles.

The editors and authors of A Practical Guide to Financial Services: Knowledge, Opportunities and Inclusion combine a wealth of financial services, educational and consumer-oriented practitioner experience.

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

‘Financial services’ is an umbrella term for a wide range of different products and services, including day-to-day money management, saving and borrowing, insurance and investing for the future.

Globally financial services have been growing and are concentrated in geographical centres, including, for example, New York, London and several Asian cities.

This development of financial services markets may contribute to economic growth and shapes the way that individuals and households manage their financial affairs.

The nature and level of household engagement with financial services is also shaped by major contextual factors, such as income growth and distribution, migration, ageing populations and climate change.

Most student texts about financial services use a corporate finance lens, while most books about personal finance focus on financial planning and products. There are very few books that aim to help both students and consumers understand from a personal finance perspective the implications of how the financial services sector works. This book aims to fill that gap. It unfolds the workings of financial services to illuminate how consumers can navigate the system better and turn it to their best advantage.

Learning outcomes

The learning outcomes for this chapter are to:

Appreciate the scale of financial services both globally and in the UK.

Understand key events that have shaped the current financial services system.

Begin to see the implications of the financial system for the well-being of individuals and households and how they manage their financial affairs.

1.1 The financial services sector

Historically, many financial services were seen as facilitating productive economic activity rather than directly creating value themselves – a debate that continues today (see, for example, Mazzucato, 2019). However, the international system, which countries use to measure the size of their gross domestic product (GDP), started to more comprehensively identify the financial sector contribution from 1993 onwards (Harrison, 2005). As the statisticians wrangled back then, before the scale of financial services sector can be measured, it is necessary first to define what it includes.

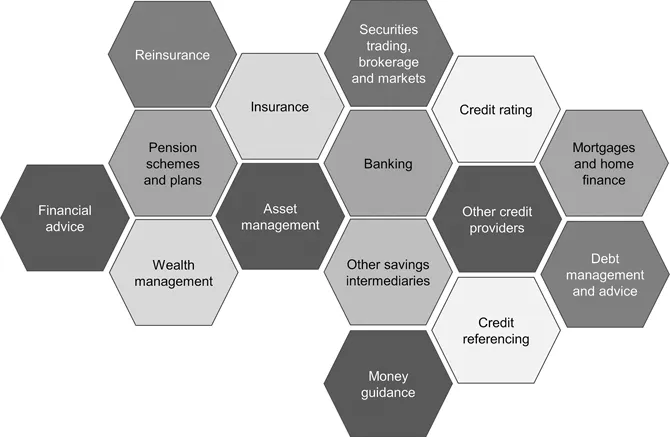

Figure 1.1 shows the main categories of financial services today, including, for example, banking, insurance, securities markets, asset management and mortgages. From a corporate perspective, these are large global markets that generate billions in profit, and the central importance of financial markets will be discussed in Chapter 2. From a consumer perspective, the categories in Figure 1.1 are the source of essential products and services needed to manage everyday living and planning for the future.

FIGURE1.1 Key financial services.

Source: author’s diagram.

1.1.1 The size of the financial sector

While individuals and households deal mainly with financial services firms located in their own country, the products they buy or invest in are the tip of a vast global network of markets.

The overall size of the global financial services market is estimated to be around $22.5 trillion (The Business Research Company, 2021). Putting the scale into context, that’s slightly larger than the whole US economy or nearly ten times the size of the UK economy, at $21.4 trillion and $2.8 trillion, respectively (World Bank, 2021a).

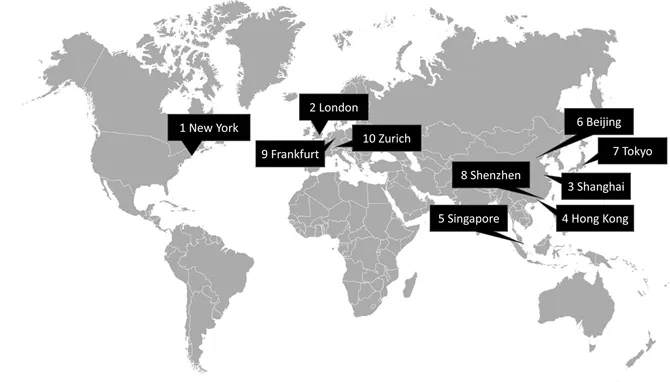

Financial markets function best when expertise and liquidity come together and so activity tends to concentrate in specific financial centres. Z/Yen, a commercial think tank, publishes twice a year a ranking of financial centres based on five ‘areas of competitiveness’: business environment, human capital, infrastructure, financial sector development and reputation. Figure 1.2 shows the ten most highly ranked financial centres from their spring 2021 survey. New York and London, which may be considered the historical cradles of financial services, retain their top spots, but there is an increasing growth of financial centres in Asia, particularly in China. While the traditional financial centres in the US and Europe have an advantage in terms of well-established regulatory regimes, Asian centres are already becoming dominant in some areas such as insurance and fintech (Z/Yen and CDI, 2021, Table 5).

FIGURE1.2 The world’s top 10 financial centres, 2021.

Source: author’s diagram based on data from Z/Yen and CDI (2021).

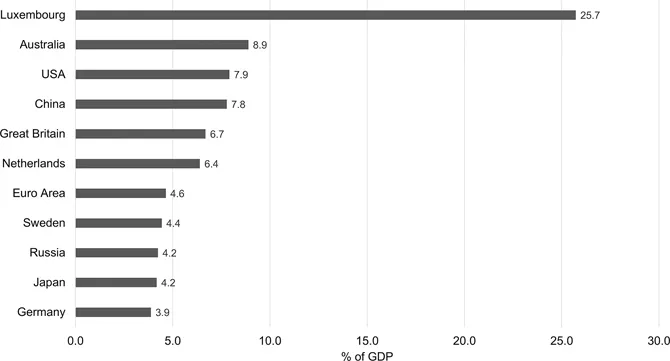

However, the importance of financial services to individual countries varies, as shown in Figure 1.3. While New York and London are globally important financial centres, financial services account for only 8% and 7% of the US and UK economies, respectively, because other sectors, such as agriculture and industry, are larger (OECD Data, 2021). On the other hand, the tiny state of Luxembourg (population 0.6 million, GDP $0.07 trillion) specialises in investment fund services, with the result that financial services account for over a quarter of its GDP (OECD 2019; OECD Data, 2021).

FIGURE1.3 Financial services sector as a percentage of GDP, selected countries, most recent data (2018 to 2020).

Source: author’s chart based on OECD Data (2021).

Yet, even at 7% of GDP, UK financial services are sizeable – it is the eighth largest sector of the economy, contributes around £130 billion a year and employs over 1.1 million people, albeit with a hefty skew towards London (Hutton and Shalchi, 2021). However, in 2021, London has given ground to some European Union (EU) financial centres ‒ for example, Amsterdam (ranked 28th in the Z/Yen survey) ‒ following the end of the ‘Brexit’ (Britain leaving the EU) transition period (Stafford, 2021). It is possible that more financial firms and jobs will relocate from the UK to the EU over time.

1.1.2 Why financial services matter to consumers

Thinking about economies as a whole, while the evidence is not conclusive, it suggests that well-developed financial systems contribute to the growth of a country’s GDP, particularly by enabling more efficient and cheaper access to finance for firms which ultimately are the engines of growth (Levine, 2004). However, access to the financial system is not necessarily equal and, especially in developing countries, may be skewed towards a privileged minority rather than benefitting the population as a whole (Claessens and Perotti, 2007). This can leave poorer segments of the population without access to the most basic financial products and services that are taken for granted in higher-income countries, where financial services are for most people part of the warp and weft of modern life. One of the most essential is banking, described in Chapter 3. It provides the means for individuals to receive income and pay their expenses, and it is the major provider of saving and borrowing products. In addition, in more developed countries having a bank account is the gateway to other financial services, acting as a first line of information about a person’s identity, creditworthiness and financial stability.

Living is an uncertain venture, and, beyond savings, insurance (Chapter 4) offers another way for households to increase their resilience against possible future adverse events, such as redundancy, illness or death. Other financial events, for example, the costs associated with bringing up children and eventual retirement, can be anticipated and planned for. The cornerstone of long-term planning is investment (the topic of Chapter 5).

In all areas of personal financial management and planning, consumers may seek financial advice, which is described in Chapter 6.

1.2 Growth and deregulation

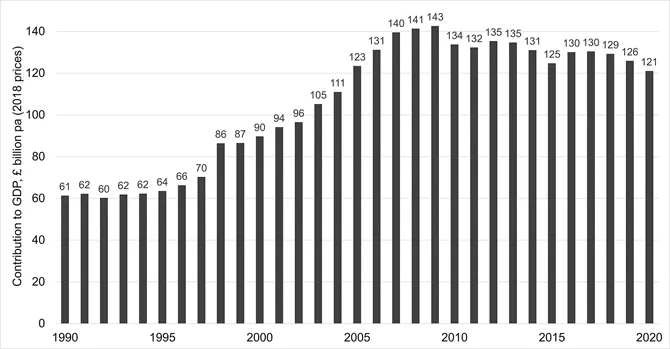

The scale of the financial services industry has increased enormously in recent decades – in the UK alone doubling in real terms (see Figure 1.4). This section explores the drivers of growth and the implications for how the sector has developed in the UK.

FIGURE1.4 Growth in the contribution of financial services to UK GDP, 1990–2020.

Source: author’s chart based on data from ONS (2021).

1.2.1 The drivers of growth

A key stimulus to this growth was financial deregulation during the 1980s. However, the factors that brought about deregulation go back much further.

After the 1939–1945 World War, economies across Europe were ravaged and trade between them was severely constrained. Initially, many countries accepted only US dollars as a trusted form of p...

Table of contents

Cover

Half Title

Title Page

Copyright Page

Table of Contents

About the authors

Acknowledgements

1 Overview of financial services

2 Financial markets

3 Banking

4 Insurance

5 Investments

6 Financial advice

7 Financial technology (fintech)

8 Financial inclusion

9 Financial services and the role of government

10 Financial crimes

11 Regulation of financial services

12 Risk and financial services

Conclusion: themes and trends in financial services

Glossary

Index

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

Both plans are available with monthly, semester, or annual billing cycles.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go. Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access A Practical Guide to Financial Services by Lien Luu, Jonquil Lowe, Patrick Ring, Amandeep Sahota, Lien Luu,Jonquil Lowe,Patrick Ring,Amandeep Sahota in PDF and/or ePUB format, as well as other popular books in Business & Finance. We have over 1.5 million books available in our catalogue for you to explore.