This policy note assesses tax administration measures and tax rate adjustments, two options for the Philippines' fiscal consolidation in terms of their efficiency for revenue mobilization and impacts on tax equity. Its key findings are: 1) a policy mix of a higher value-added tax and a lower corporate income tax will make the overall tax system more regressive, even if its impact on tax revenue is neutral; 2) the country's tax productivity is much lower than those of its peers in the region, which signals the presence of significant tax loopholes and weak tax administration; and, 3) there is ample room to increase excise taxes on tobacco, alcoholic products, and gasoline, without ruining the equity of the tax system. These suggest that tax administration remains a key focus of efforts for the new administration.

eBook - ePub

Tax Reforms toward Fiscal Consolidation

Policy Options for the Government of the Philippines

- 20 pages

- English

- ePUB (mobile friendly)

- Available on iOS & Android

eBook - ePub

Tax Reforms toward Fiscal Consolidation

Policy Options for the Government of the Philippines

About this book

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Study more efficiently using our study tools.

The Current Tax System and Its Problems

In the Philippines, VAT, CIT, and personal income tax (PIT), make up over two thirds of total tax revenues. Although the statutory tax rates applied in the country are higher than those of its neighboring countries, the revenues generated as a share of GDP are not proportionally higher compared to those of its neighboring countries. Although the share of indirect taxes (VAT, excise taxes, customs duties, etc.) has been decreasing, indirect taxes still account for 58% of total tax revenues in 2009. This suggests that the country’s overall tax system is relatively regressive compared to that in the other countries in the Asia and Pacific region. In theory, fairness of a tax system must be checked in the context of the progressivity of public spending. Even if revenues are raised in a regressive manner, the overall impacts of the tax system can be progressive if the authorities spend its resources more for the poor. However, given the limited spending on education and health and weak targeting of poverty programs4 in the Philippines, the country’s tax system cannot be progressive even after taking into account the expenditure pattern. The fiscal system has not helped distribute income more equitably.5

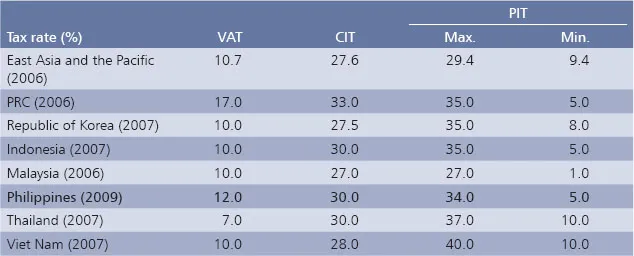

Several business surveys show that a high tax rate is one of the barriers to doing business in the country. However, the current CIT rate of 30%, having dropped from the previous 35% in 2009, is comparable with the rate of the neighboring countries (Table 1).6 PIT rates, both the maximum (34%) and the minimum (5%), are also comparable with those of the other countries. In the Philippines, the VAT was introduced in 1998 with a single rate (10%) and a reasonable exemption threshold. The VAT base was then broadened to cover services in 2004 and petroleum products and electricity in 2005. With the VAT reform in 2005 (RA 9337,7 known as the reformed VAT law), the VAT rate was increased to 12%, the highest in the Asia and Pacific region. With the rate increase, the VAT-to-GDP ratio rose from 1.65% in 2004 to 2.18% in 2007.

Table 1 Tax Rates in Selected Countries

CIT = corporate income tax, PIT = personal income tax, PRC = People’s Republic of China, VAT = value-added tax.

Source: World Bank, World Development Indicators.

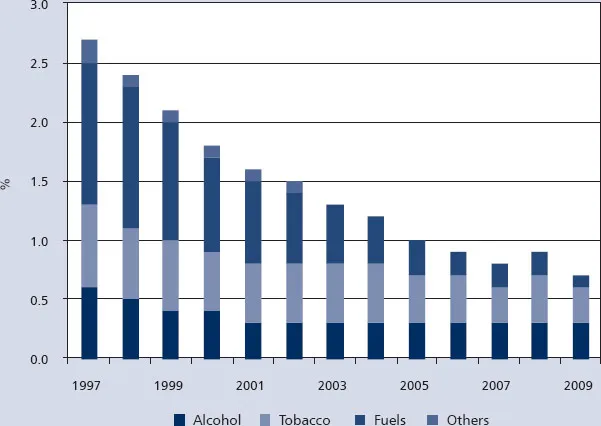

Excise taxes are levied on tobacco, alcoholic products, and petroleum products. Currently, a grave concern is the dramatic decline of the excise taxes. From 1997 to 2009, excise taxes as a share of GDP decreased by 1.8 percentage points (Figure 5). In 1996, the authorities shifted the excise tax from an ad-valorem to a complicated multitiered unit tax rate, and did not allow for inflation adjustment. The authorities, with the RA 9334 approved in 2004, planned discrete increases in the tax rate on tobacco and alcoholic products beginning 2005 and every other year until 2011.8 The reformed VAT law in 2005 incorporated a number of mitigating measures, including reducing the selected petroleum excises (Table 2) and import tariff of petroleum products from 5% to 3%.

Figure 5 Philippines: Excise Tax Revenues (% of GDP)

Source: International Monetary Fund, Article IV consultation reports.

Table 2 Philippines: Excise Taxes on Petroleum Products (Peso/liter)

| Item | Before the 2005 reform | After the 2005 reform |

| Gasoline (regular) | 4.80 | 4.35 |

| Kerosene | 0.60 | 0.00 |

| Diesel | 1.63 | 0.00 |

| Bunker fuel | 0.30 | 0.00 |

Source: The Philipp...

Table of contents

- Front Cover

- Title Page

- Copyright Page

- Contents

- List of Tables and Figures

- Abbreviations

- Summary

- Where Are We?

- Two Policy Options

- The Current Tax System and Its Problems

- Assessment of the Two Options

- Tax Administration Reforms

- Back Cover

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

- Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

- Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go.

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Tax Reforms toward Fiscal Consolidation by Norio Usui in PDF and/or ePUB format, as well as other popular books in Law & Tax Law. We have over 1.5 million books available in our catalogue for you to explore.